区块链项目融资详情一网打尽,助力你发现更好的撸毛机会!

Topic Background

CryptoMubai

Crypto Newbie

56m ago

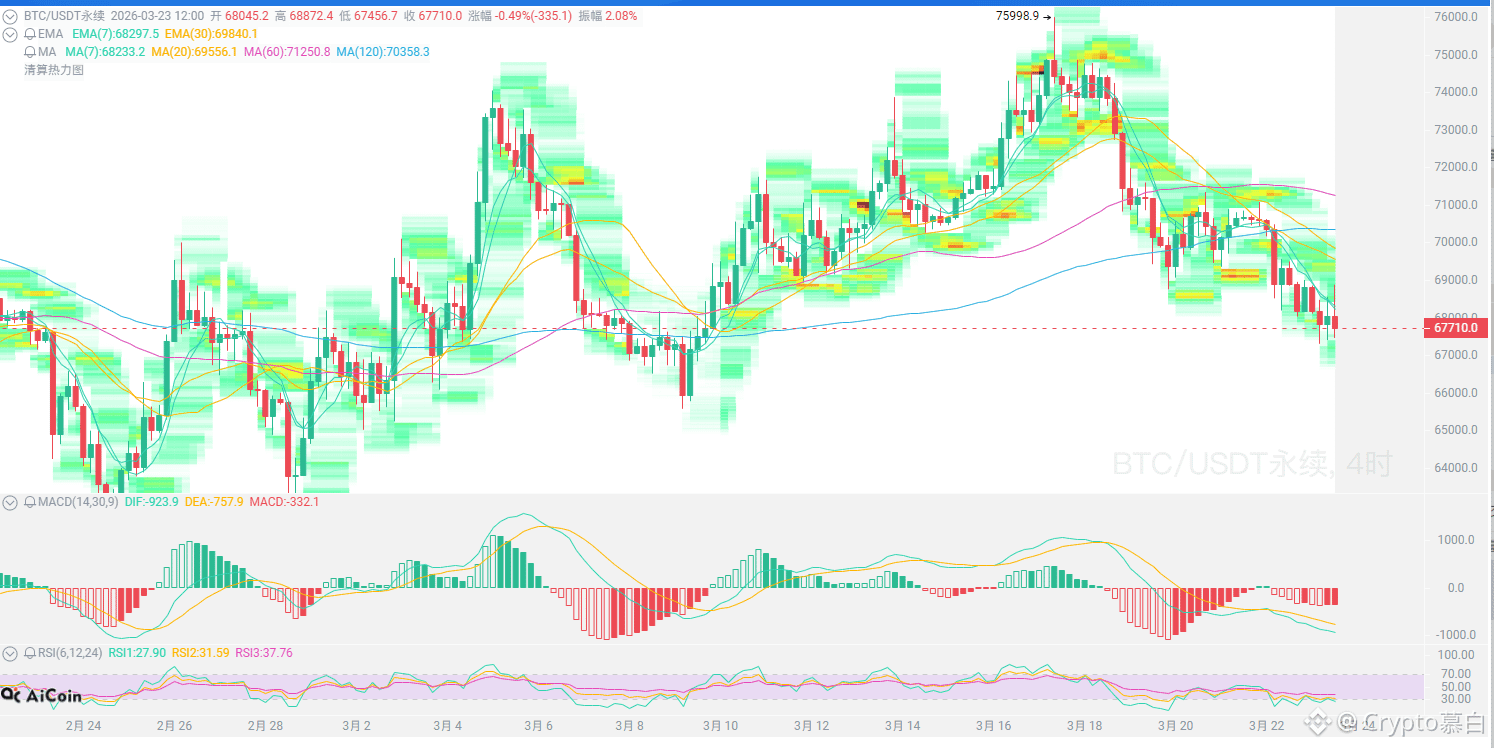

Let's analyze today's $BTC trend:

From a candlestick chart perspective, the price has been suppressed below the moving average for several days, breaking below the 20-day moving average and the Bollinger Band middle line, indicating a weak short-term trend.

The bears are still in control, but momentum is weakening. The MACD histogram shows that the downward momentum is weaker than in previous days, indicating that although the price is still falling, the selling pressure is not as strong as before.

The RSI is around 46, not yet in the oversold zone, suggesting there may be further downside potential.

On the hourly chart, the price is being suppressed by a descending trendline, with resistance around 69200. If it cannot break above this level, the rebound will be limited.

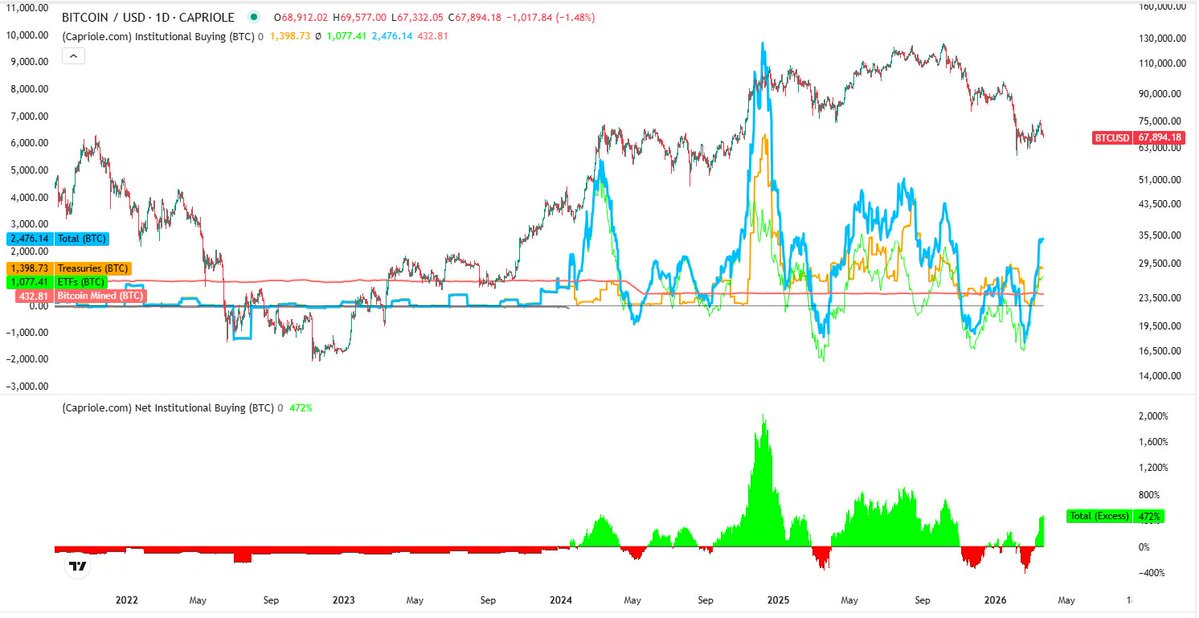

The Fear & Greed Index has fallen to around 10, indicating extreme fear, suggesting that retail investors are panicked. Interestingly, institutions seem to have stayed—data shows that Bitcoin ETFs saw a net inflow of $1.3 billion in March, and whales have cumulatively bought over 40,000 BT.

Retail investors are selling at a loss, while institutions are accumulating shares. This contrarian signal historically often indicates that the market is nearing its bottom.

Upside resistance: 69000-70000

Downside support: 67000-66000

Short-term trend is slightly weak and volatile, like being pulled back and forth within a "range," lacking a clear direction. The overall structure remains bearish. Institutions are quietly accumulating, but retail investor confidence is weak, making further declines possible! Be aware of the risks.

#CZ says Bitcoin is a hard asset #Trump's 48-hour ultimatum

{future}(BTCUSDT)

23

404

45

FinanceRun

Crypto Newbie

1h ago

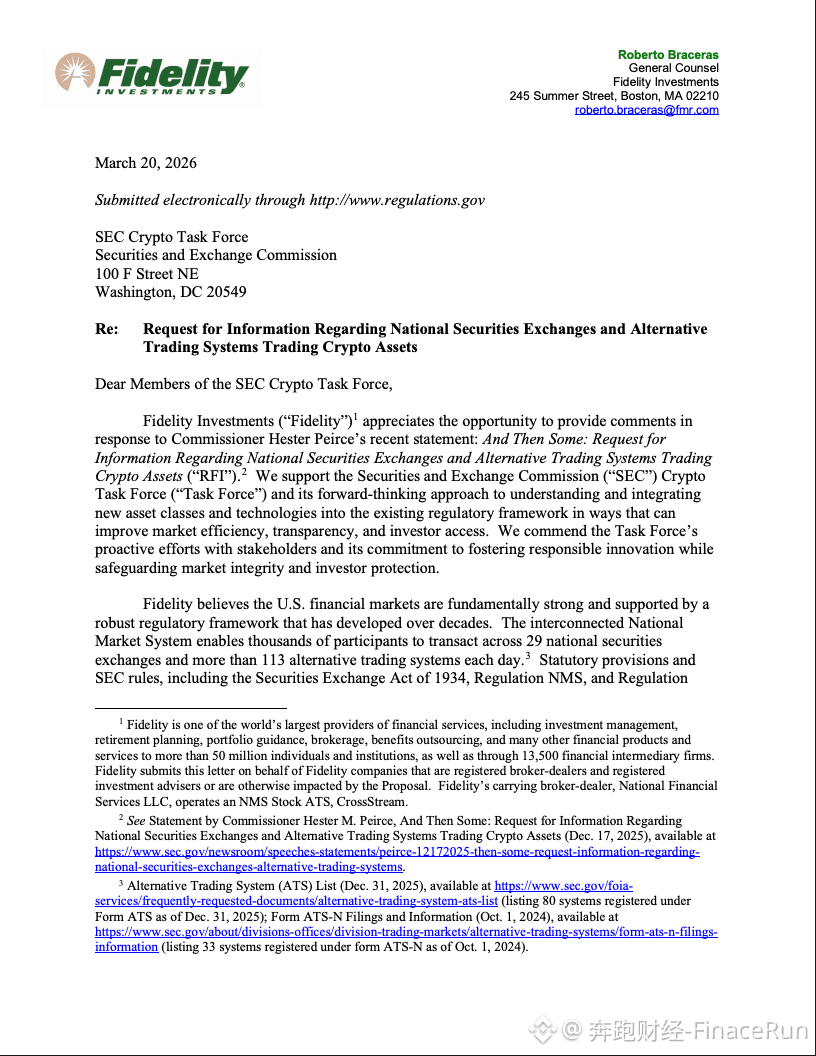

Fidelity Sends Letter to SEC: Tokenized Asset Regulation Should Not Be "One Token, One Rule," Differentiated Rules and Regulatory Models Needed

On March 22, Fidelity Investments, a US asset management company, sent a letter to the US Securities and Exchange Commission (SEC), responding to the SEC's earlier public comment period.

In the letter, Fidelity Investments called on the SEC to further refine its regulatory framework, primarily addressing matters related to brokers offering, custodian, and trading crypto assets on alternative trading systems (ATS).

The letter emphasized that developing a comprehensive regulatory framework and clear rules for trading tokenized securities is "crucial," including rules governing the trading of tokenized securities issued by third parties.

The letter pointed out that tokenized instruments have different issuance structures, legal attributes, and valuation models. For example, tokenized real-world assets (RWAs) encompass entirely different asset classes such as stocks, real estate, bonds, or private credit.

Fidelity further explains that tokenization models differ significantly in structure and the rights granted to holders. Some models allow indirect access to underlying securities through security interests, while others restrict participation to qualified contract investors based on security swaps.

This structural difference means the tokenization market is already "layered," requiring regulatory oversight that avoids a one-size-fits-all approach. Differentiated rules must be developed for different models; otherwise, compliance is impossible.

Furthermore, because DeFi financial trading platforms lack a central authority and cannot generate detailed financial reports as required by the SEC, Fidelity urges the SEC to bridge the regulatory gap between CeFi and DeFi trading systems and consider how they should evolve and coexist.

In response, Fidelity recommends that the SEC issue guidance allowing brokers to utilize distributed ledger technology for alternative trading systems and other record-keeping, aiming to alleviate unnecessary financial reporting burdens for decentralized systems by modifying reporting requirements.

In summary, Fidelity's letter reveals that some RWAs are merely digital shells of traditional securities, while others have become high-barrier contract derivatives, clearly inconsistent with a unified market regulatory logic.

Fidelity's demands are straightforward: either break down the rules into smaller, more manageable sections, or stifle innovation in the industry. The SEC's response will determine how fast CeFi can grow and how far the DeFi world can go.

#TokenizedSecurities

46

335

30

Jamie Coutts CMT

Crypto Newbie

1h ago

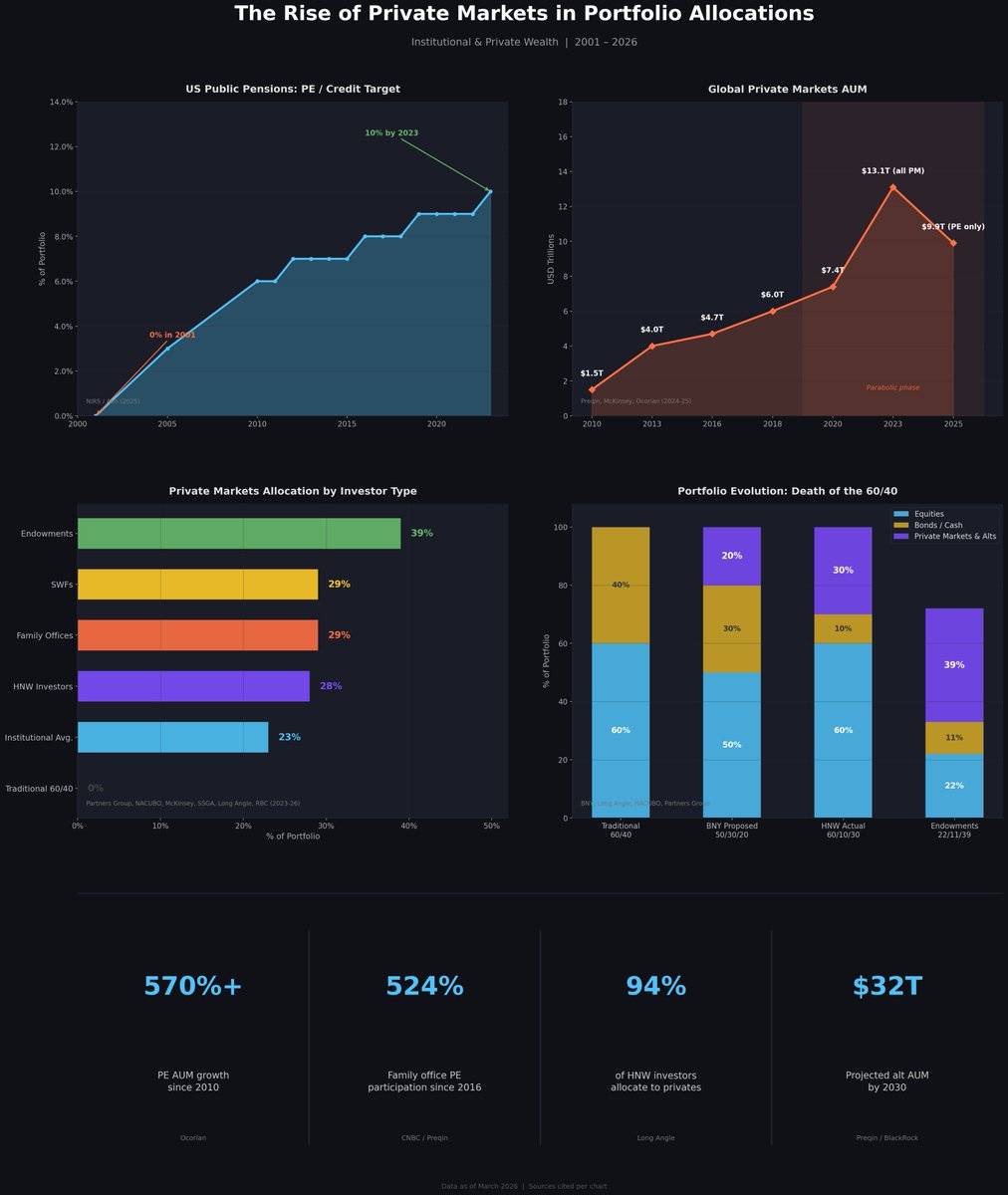

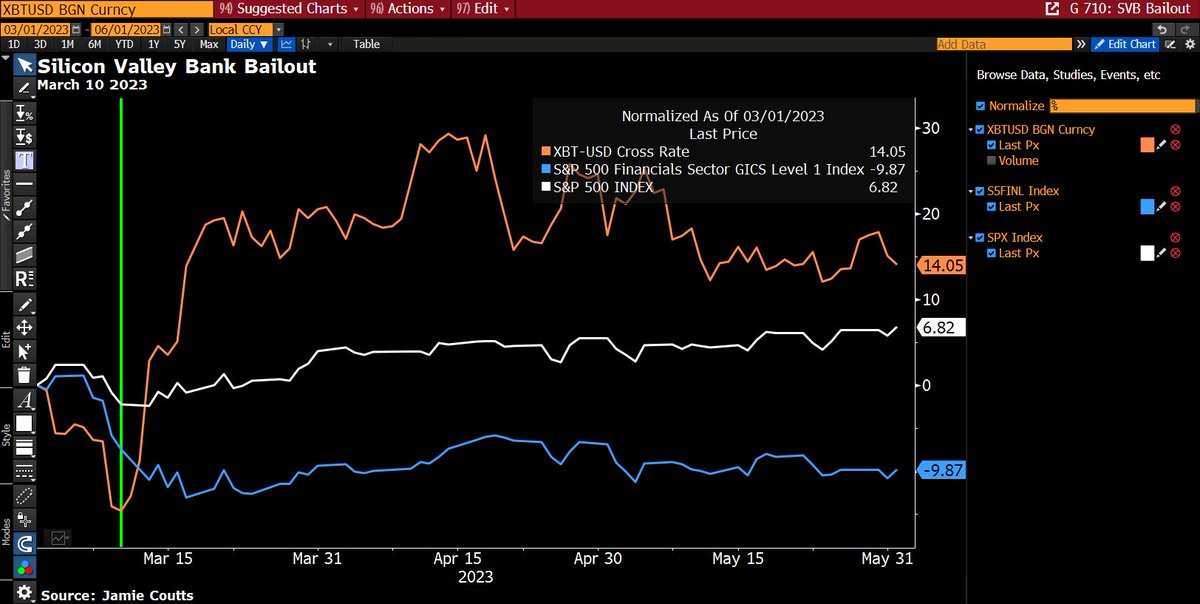

For a decade, private equity firms have been touting low volatility and portfolio diversification. This is essentially volatility whitewashing. Not pricing in market capitalization doesn't mean there are no losses. It means problems won't be discovered until it's too late. And now, it's too late.

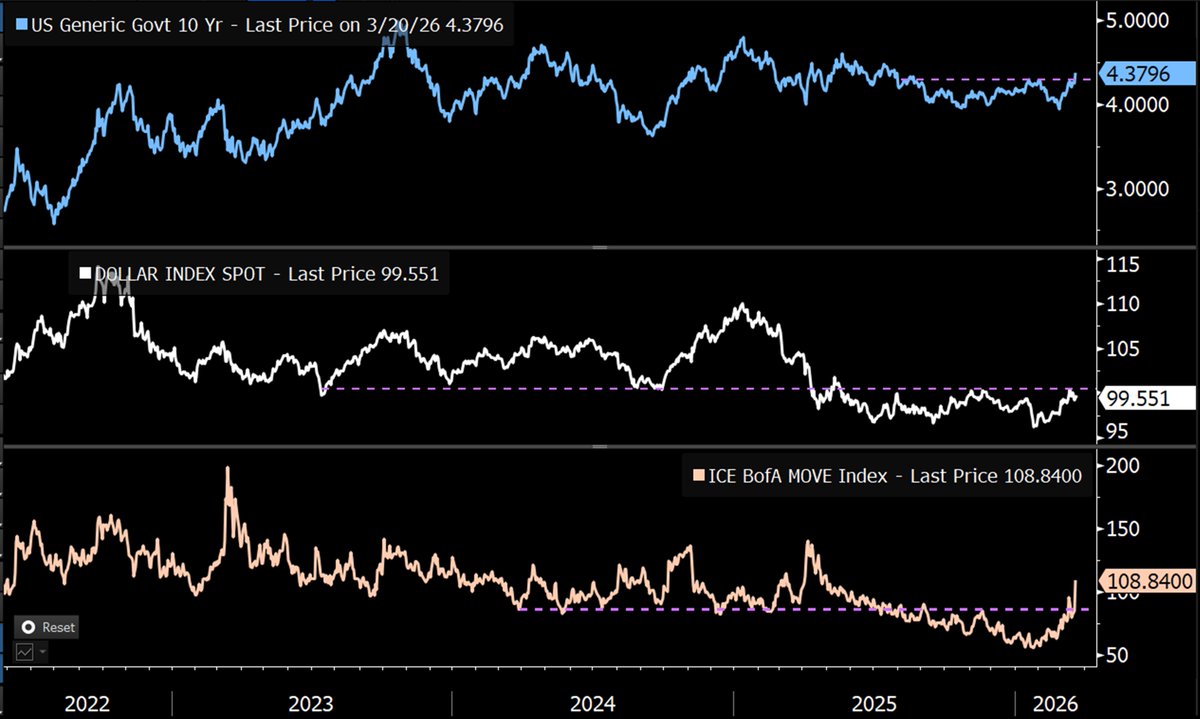

Bitcoin's position is rising as the illusion of a fractional-reserve credit system for fiat currencies stumbles from one crisis to another. 🧵

Liquidity is under pressure. The MOVE index is soaring. The US Dollar Index (DXY) is nearing the warning line of 100.50. Credit conditions are tightening in private equity and AI-related sectors. Inflation expectations are currently rising significantly. The macroeconomic outlook is not optimistic.

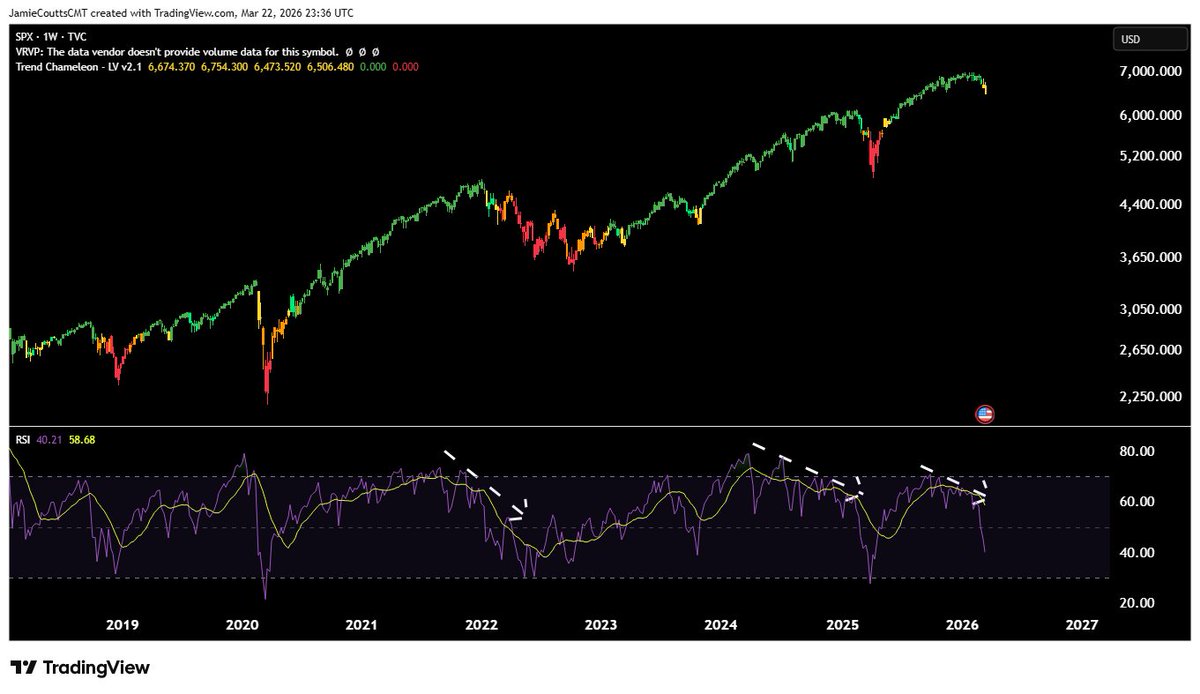

Stock markets are reacting sluggishly. However, this year, the Relative Strength Index (RSI) for major stock indices is diverging—prices are hitting new highs while momentum is waning. This is a typical late-cycle top pattern. The market expects a soft landing for the economy. But the credit market is not.

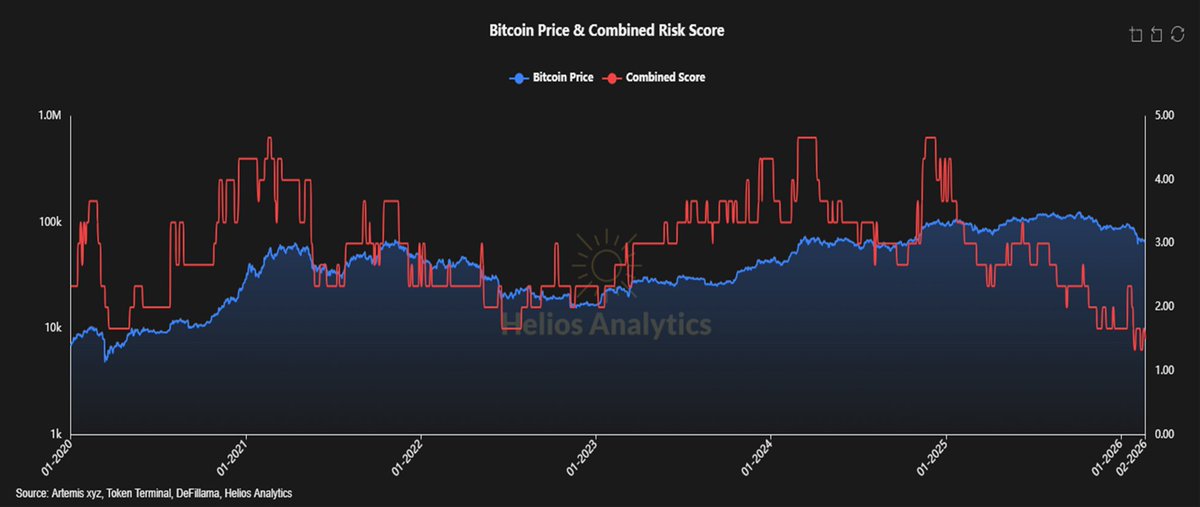

Bitcoin's resilience last month stemmed from two factors. The capitulation sell-off triggered by the February lows cleared out previously accumulated leverage—the excessive leverage built up before 2025. Derivatives further compressed volatility before 2025. But this was merely structural support, not genuine strength. Given that all risk assets face typical 10-15% drops, this buffer no longer exists. The February lows have resurfaced.

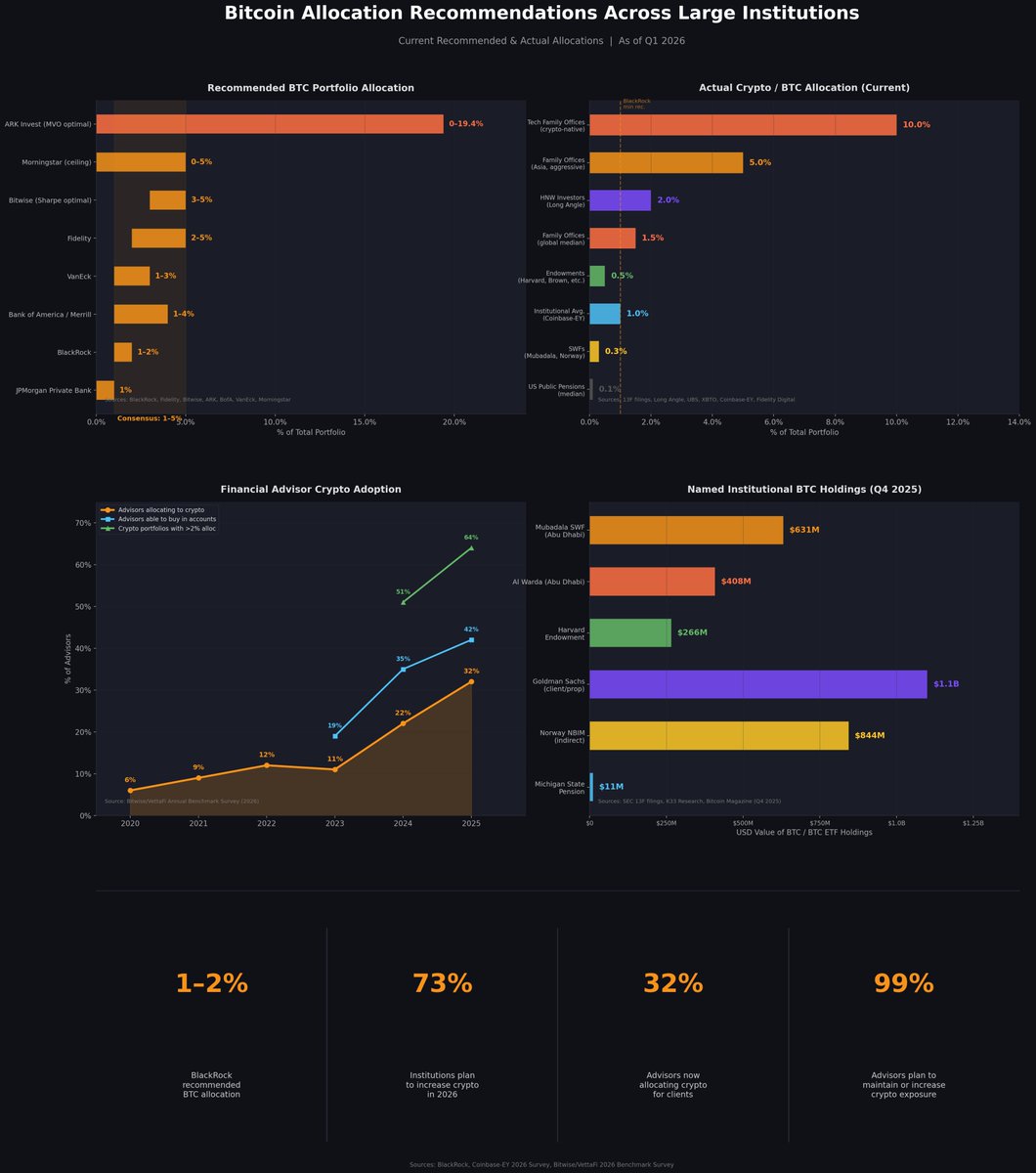

Inflows into Bitcoin ETFs surged again in March, but may have peaked and begun to decline.

Short-term bearish, long-term bullish. Here's why. This is the range of risk traditional investors face. Since 2010, private equity fund assets under management have grown by over 570% and are projected to reach $32 trillion by 2030. Institutional investors' share of the private market has risen from 17% to 27% in a decade. 94% of high-net-worth investors now hold alternative investments. Its selling points are: low volatility, diversification, and uncorrelated returns. The reality, however, is: volatility for money laundering. Opaqueness does not equal stability. Asset prices are constantly adjusting. You simply cannot predict when this will happen.

Now imagine what will happen to Bitcoin when all this happens. All risks will be repriced. But Bitcoin's volatility relative to traditional assets has been declining for years. Transparent ledger, real-time settlement. No valuation methods based on fantasy. The recommended weighting is for reference only. Actual allocation will increase, and the recommended weighting may increase accordingly.

When the bailout plan arrives—and it will eventually—this asset will be the first to smell its scent.

Despite the government/Federal Reserve's vehement denial of ample liquidity.

47

493

31

KK.aWSB

Crypto Newbie

4h ago

🚨Breaking News: A major anti-Semitic arson attack has occurred in Golds Green, London, destroying all of Hatzola Northwest's ambulances (at least four).

—Hatzola Northwest is a Jewish volunteer emergency service providing 24/7 medical assistance.

Source: @Breaking911

43

459

43

Wu Blockchain

Binance

6h ago

Wu learned that Fidelity Investments submitted comments to the U.S. Securities and Exchange Commission (SEC) Crypto Assets Working Group, recommending the integration of crypto asset trading within the existing regulatory framework, guided by the core principles of the Securities Exchange Act; proposing further improvements to the regulatory framework for broker-dealers providing, custodiing, and trading crypto assets;

issuing guidance to support alternative trading systems (ATS) in conducting tokenized securities trading and relying on the inherent properties of assets; assessing the evolution and coexistence of mediated and decentralized trading venues; and revising rules to promote the integration of on-chain systems into the securities market, including allowing the use of distributed ledger technology for record keeping and clarifying that on-chain settlement should not be considered a "clearinghouse."

30

370

49

Mars Finance

Crypto Newbie

7h ago

🔔Data: Erik Voorhees' linked address holds $249 million in ETH, rising to seventh place among institutional holders

According to Mars Finance, AI Aunt's monitoring shows that the linked address (0x3e68...Ef2f7) of Venice founder Erik Voorhees recently purchased another 1,624 ETH, worth $3.36 million.

This brings the total ETH held by this address to 121,929.46, with a total value of $249 million and an average cost of $2,158.51. According to strategicethreserve data, this holding has surpassed Mantle's 101,870 ETH, rising to seventh place among institutional ETH holders.

43

363

38

Mars Finance

Crypto Newbie

7h ago

🔔SkyBridge Founder: Bitcoin's Four-Year Cycle Continues, Price Expected to Rise in Q4

According to Mars Finance, SkyBridge founder Anthony Scaramucci stated that the current Bitcoin bear market can be explained by the four-year cycle theory and long-term holders selling at the psychological price level of $100,000. He pointed out that while inflows from institutional investors and Bitcoin ETFs have "mildened" the four-year cycle, they haven't completely eliminated this traditional cycle, and the shared beliefs of market participants create a self-fulfilling prophecy.

He predicts that Bitcoin will fluctuate for most of 2026, with a new bull market cycle starting in the fourth quarter. Scaramucci stated that market participants, including himself, generally expected Bitcoin to reach $150,000 by 2025, driven by the Trump administration's pro-crypto agenda and improved regulation, but the October market crash completely shattered this consensus.

He cited Bitcoin's price movement in early 2023 after the FTX crash in November 2022 as an example to illustrate that the market often moves in the opposite direction to mainstream sentiment. Bull markets usually begin in a period of "extreme indifference and lack of interest," and the current bear market is a "normal" correction consistent with previous pullbacks.

29

452

29

Mars Finance

Crypto Newbie

7h ago

🔔Fidelity Calls on SEC to Establish New Framework Allowing Brokerages to Trade Crypto Assets via ATS

According to Mars Finance, Fidelity, in a letter to the U.S. Securities and Exchange Commission (SEC), proposed establishing a regulatory framework that would allow broker-dealers to trade crypto assets through alternative trading systems (ATS). This proposal aims to integrate crypto asset trading into the existing financial system, enhancing market compliance and institutional participation.

35

435

36

BRICS News

Crypto Newbie

14h ago

Breaking news: The Speaker of the Iranian Parliament stated, "Financial institutions that fund the US military budget are legitimate targets."

"US Treasury bonds are soaked in the blood of Iranians. Buying them is tantamount to buying an attack on your headquarters and assets. We will be closely monitoring your investment portfolio. This is an ultimatum."

25

307

32