Topic Background

Bit forward

Crypto Newbie

2h ago

Eight Pieces of Advice from Justin Sun to Young People Eight Years Ago:

(Don't buy Justin's cryptocurrency, but listen to his advice!)

1. Before 30, don't buy a house, a car, or get married. Invest all your cash flow in self-improvement.

2. Marriage is the most tightly bound yet most dangerous partnership in human history. Most people aren't capable of being a good partner before 30.

3. Investing in yourself isn't about taking a bunch of courses, but about spending 20% of your time trying and failing, and 80% of your time reflecting on your mistakes.

4. Spend your money on information density in first-tier cities, not on mortgage payments in county towns.

5. Treat your social media accounts like equity with unlimited leverage; your followers are your future cash flow.

6. Financial freedom isn't about how much money you have in your account, but about no longer having to sacrifice your emotions, dignity, and attention for money.

7. The sooner you acknowledge your limitations, the faster you'll embark on the road to wealth. Acknowledging your limitations is the first step to change. 8. Compound interest isn't just for money; health, knowledge, and brand also have compounding curves, provided you live long enough.

Each point deserves careful consideration, especially looking back now, as many have already been taught a lesson by reality…

How many of these did you heed back then? Do you still agree with them all now? 👇

#JustinSun #FinancialFreedom #LifeAdvice

29

458

33

crypto九笙

Crypto Newbie

3h ago

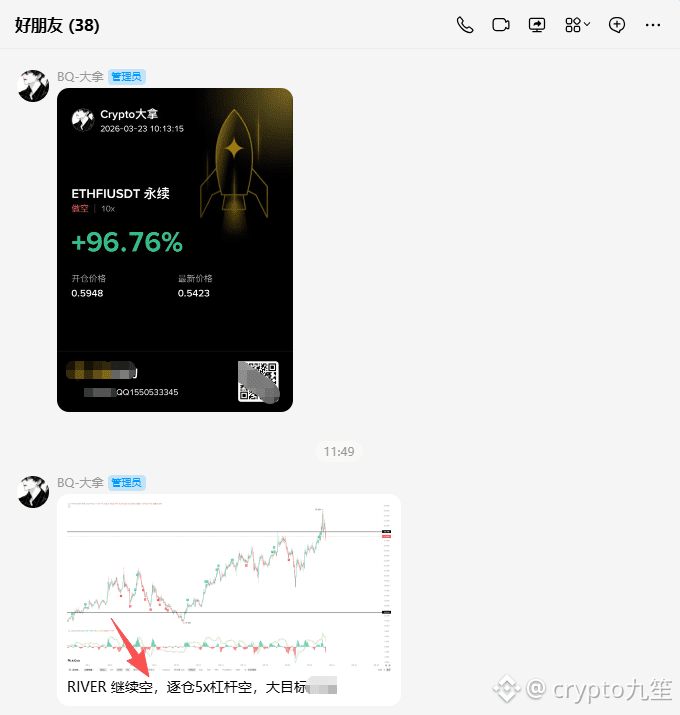

Shorting is definitely the fastest way to make money in this market!

$RIVER

{future}(RIVERUSDT) I went short with my brothers this morning, and it's already up eight points. I'm using 5x leverage, so the profit might not be very noticeable, but with 20x leverage, it would be more than double the return!

Don't panic when the market moves. Even if you don't have innate talent, you need to know how to follow the trend!

My trading record is briefly described on my homepage.

20

438

27

Jamie Coutts CMT

Crypto Newbie

4h ago

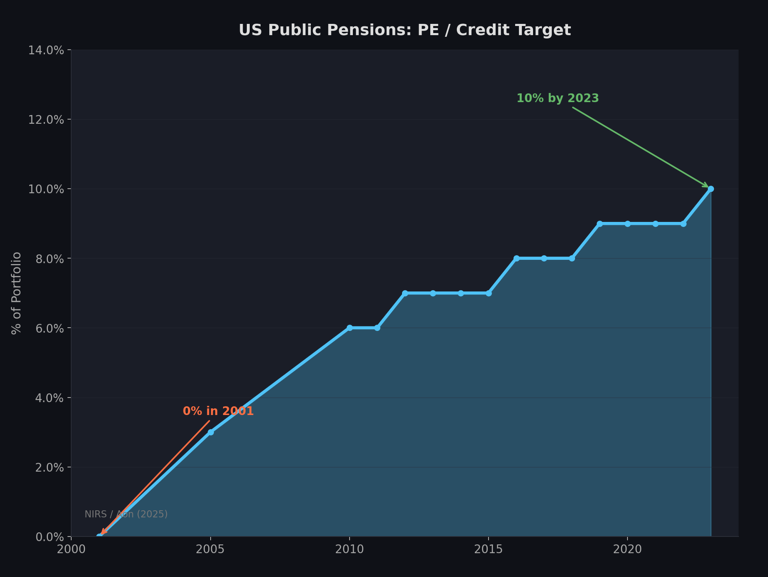

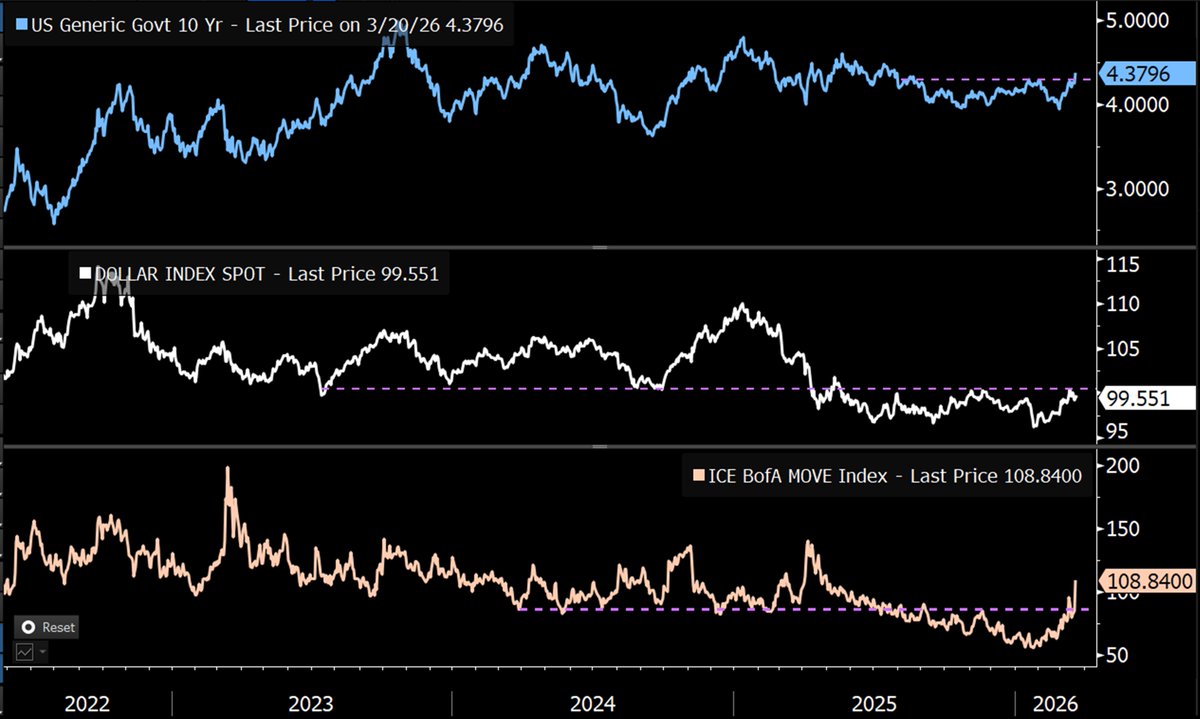

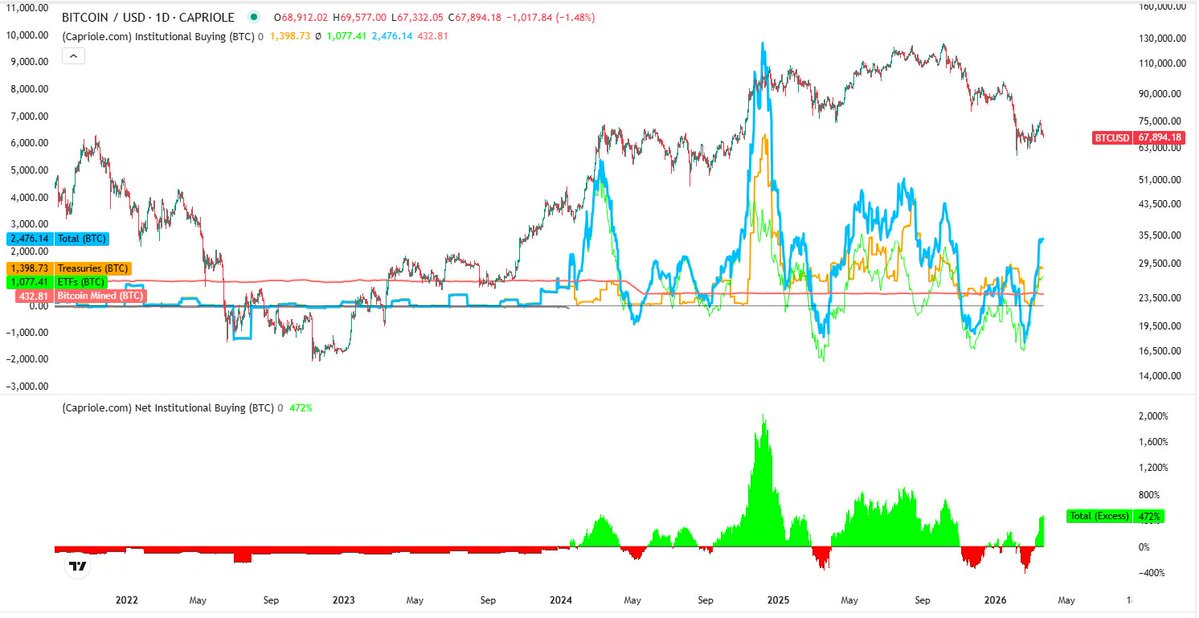

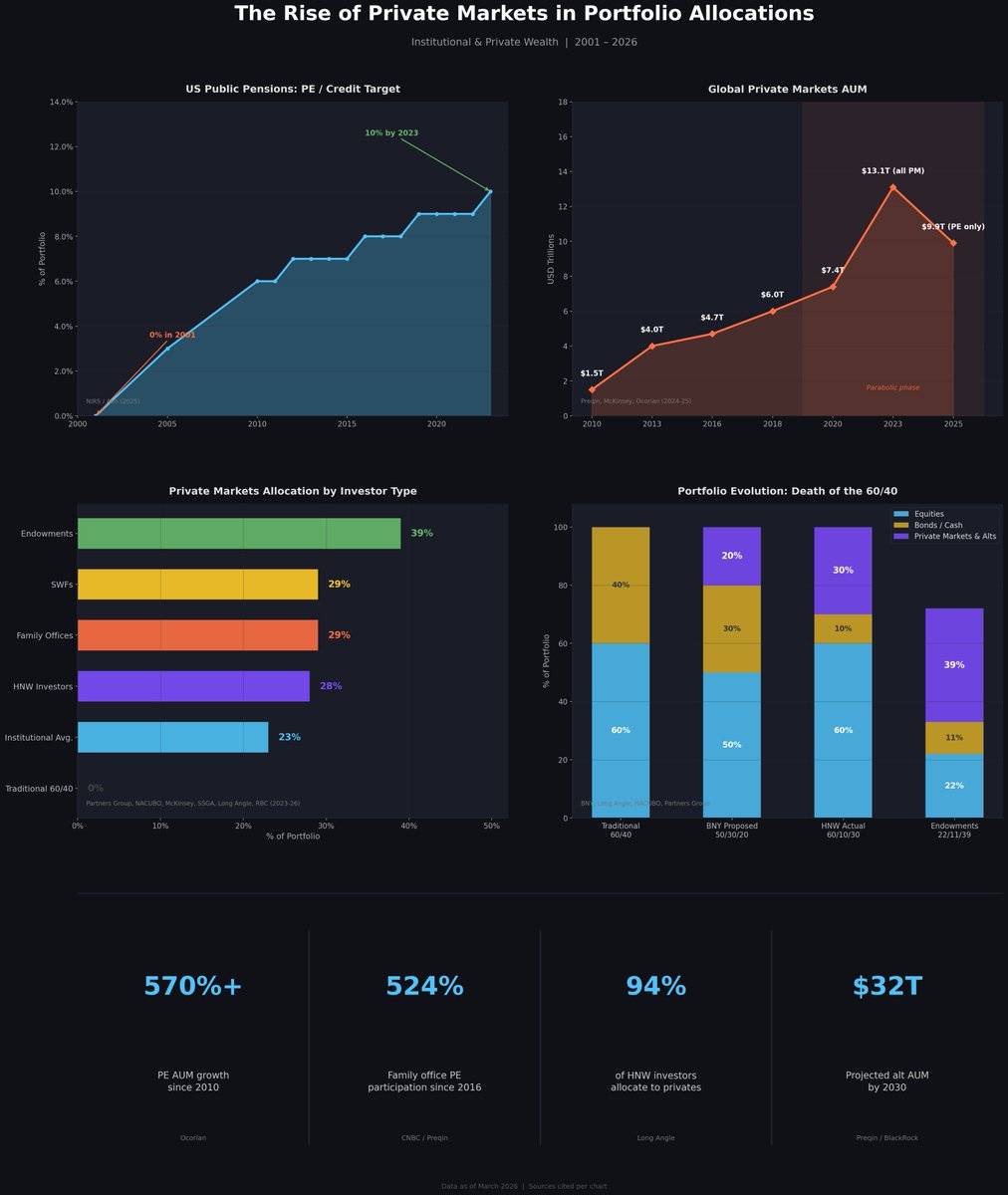

For a decade, private equity firms have been touting low volatility and portfolio diversification. This is essentially volatility whitewashing. Not pricing in market capitalization doesn't mean there are no losses. It means problems won't be discovered until it's too late. And now, it's too late.

Bitcoin's position is rising as the illusion of a fractional-reserve credit system for fiat currencies stumbles from one crisis to another. 🧵

Liquidity is under pressure. The MOVE index is soaring. The US Dollar Index (DXY) is nearing the warning line of 100.50. Credit conditions are tightening in private equity and AI-related sectors. Inflation expectations are currently rising significantly. The macroeconomic outlook is not optimistic.

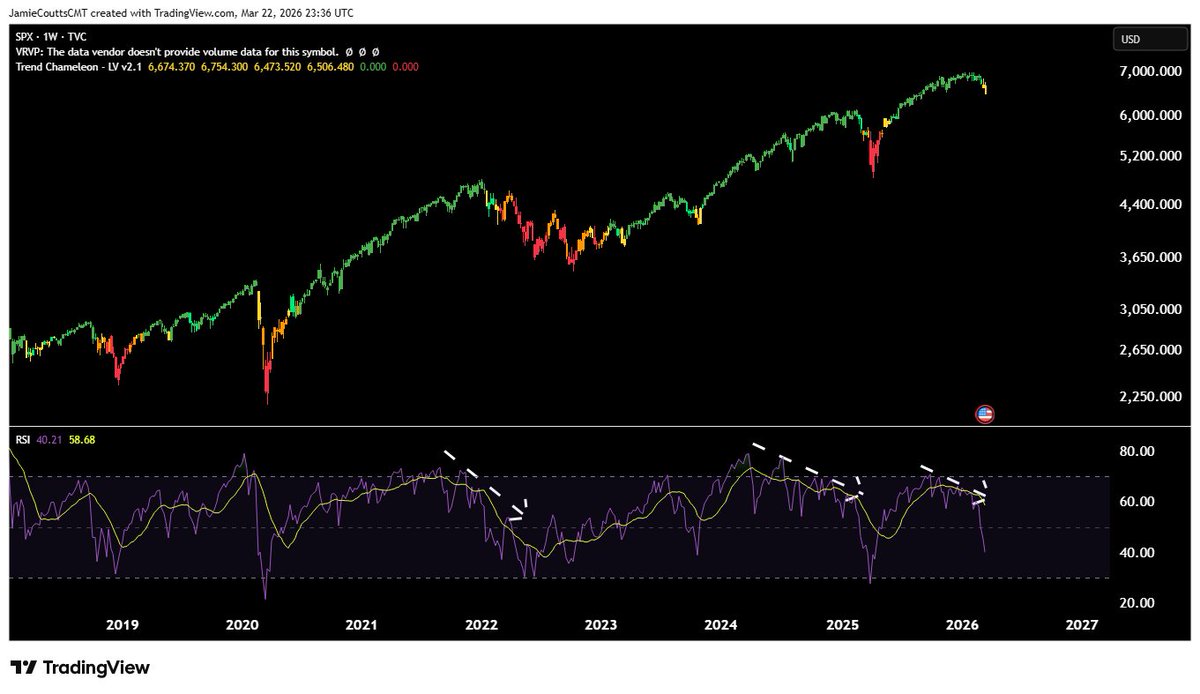

Stock markets are reacting sluggishly. However, this year, the Relative Strength Index (RSI) for major stock indices is diverging—prices are hitting new highs while momentum is waning. This is a typical late-cycle top pattern. The market expects a soft landing for the economy. But the credit market is not.

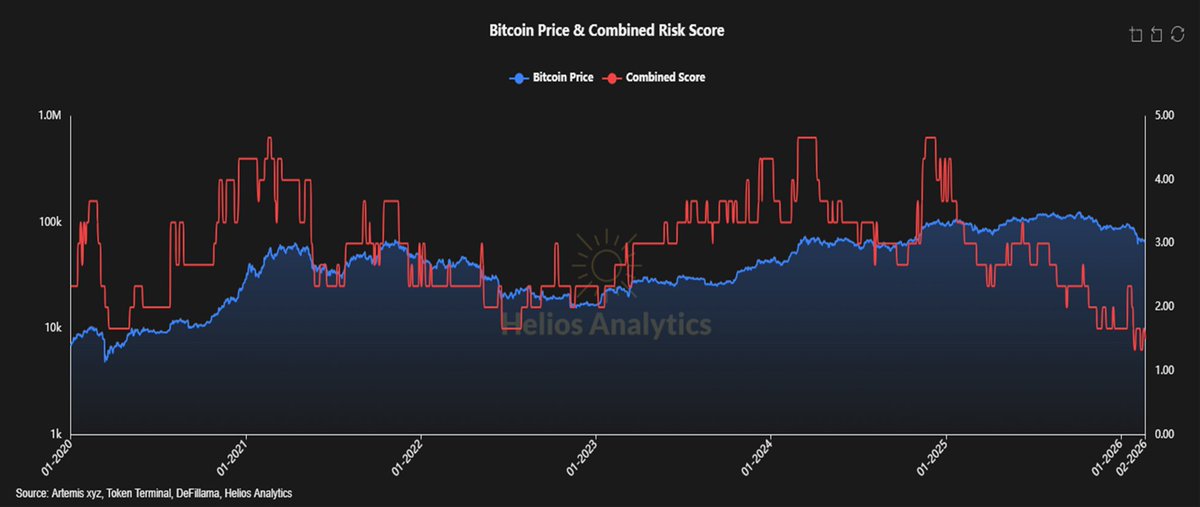

Bitcoin's resilience last month stemmed from two factors. The capitulation sell-off triggered by the February lows cleared out previously accumulated leverage—the excessive leverage built up before 2025. Derivatives further compressed volatility before 2025. But this was merely structural support, not genuine strength. Given that all risk assets face typical 10-15% drops, this buffer no longer exists. The February lows have resurfaced.

Inflows into Bitcoin ETFs surged again in March, but may have peaked and begun to decline.

Short-term bearish, long-term bullish. Here's why. This is the range of risk traditional investors face. Since 2010, private equity fund assets under management have grown by over 570% and are projected to reach $32 trillion by 2030. Institutional investors' share of the private market has risen from 17% to 27% in a decade. 94% of high-net-worth investors now hold alternative investments. Its selling points are: low volatility, diversification, and uncorrelated returns. The reality, however, is: volatility for money laundering. Opaqueness does not equal stability. Asset prices are constantly adjusting. You simply cannot predict when this will happen.

Now imagine what will happen to Bitcoin when all this happens. All risks will be repriced. But Bitcoin's volatility relative to traditional assets has been declining for years. Transparent ledger, real-time settlement. No valuation methods based on fantasy. The recommended weighting is for reference only. Actual allocation will increase, and the recommended weighting may increase accordingly.

When the bailout plan arrives—and it will eventually—this asset will be the first to smell its scent.

Despite the government/Federal Reserve's vehement denial of ample liquidity.

47

494

31

Chaos Technology

Crypto Newbie

4h ago

The top gainers list for $SIREN is dominated by newly listed coins, and some more are expected to catch up. The 'Siren' coin doubled in a single day, which is truly astonishing. I'm going long on $TRUTH at 0.01, and there's a high probability it will follow suit. My initial target is 0.0122-0.0135, which is frankly quite low. With reduced leverage, I'm waiting for a surge in volume and a takeoff!

{future}(TRUTHUSDT)

{future}(SIRENUSDT)

48

364

39

GiGi Lucky Pig

Crypto Newbie

8h ago

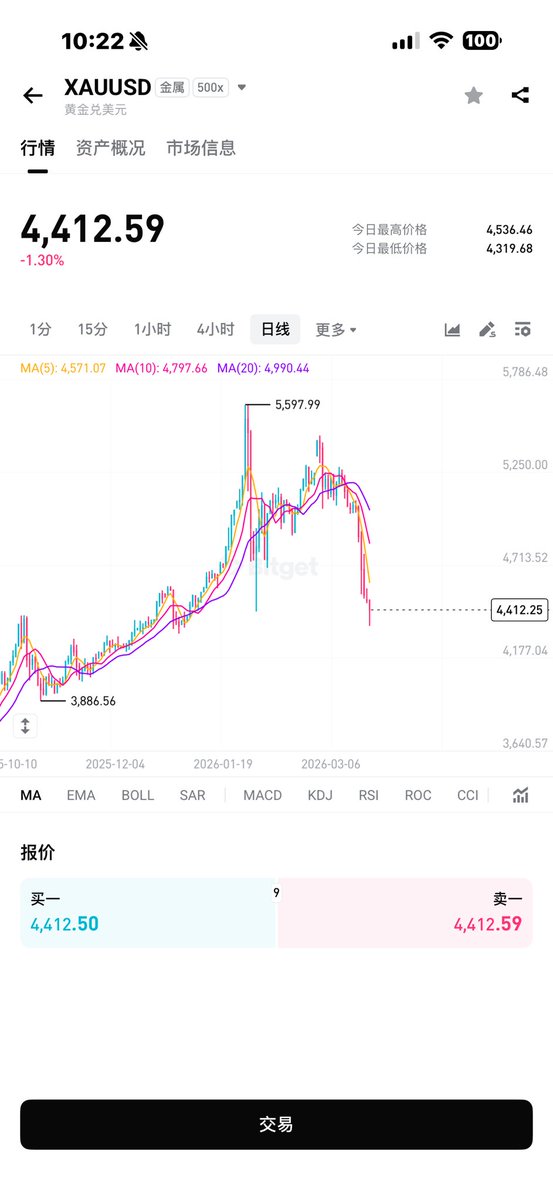

When Safe Haven Becomes a Slaughterhouse: The Collapse of the Gold Faith

These past few days, watching gold's price movements, a picture keeps popping into my head: a flock of sheep panicking in a blizzard, thinking they've stumbled into a warm shelter, only to find it teeming with drooling, hungry wolves.

This isn't just a horror story; it's a true reflection of the current gold market.

Gold has changed; it's no longer the docile safe-haven asset it once was.

We used to say, "Antiques in prosperous times, gold in chaotic times"—that was an ironclad rule.

But now, gold's persona has completely collapsed.

It's become desensitized to real interest rates, showing a negative correlation with inflation. Ironically, it's now in sync with the US stock market, exhibiting a very strong positive correlation.

What does this mean? It means that after massive bubbles were injected, gold has been completely transformed into a risky asset.

Those of us in the cryptocurrency world should feel this most acutely. Like Bitcoin, which we placed high hopes on, thinking it was digital gold to hedge against inflation, but when extreme market conditions hit, it fell more closely with the US stock market than anything else. The so-called safe-haven properties are incredibly fragile in the face of liquidity and leverage.

Gold is currently experiencing the most devastating bullish stampede.

When a real risk event strikes, funds instinctively rush into gold as a safe haven. But once the market realizes its current risky nature, panic instantly reverses. People who initially came to seek shelter from the rain, only to find the shelter leaking or even containing landmines, begin to flee.

This isn't safe-haven; it's a stampede of bulls. The price avalanche is like sheep rushing into an igloo, fighting for survival, only to find themselves the prey.

This teaches us a lesson: in this bubble-filled market, there is no absolute safe haven. When an asset is excessively inflated, its so-called safety may just be bait to lure you in. Don't be misled by labels; only clear-headed awareness and a constantly vigilant mind can save you.

#Gold $BTC #XAU

#TradeFi #Bitget

25

320

23

TheKingfisher

Infra

17h ago

Most Bitcoin price fluctuations are fake.

Not manipulated. Not a scam.

Fake. Designed by humans. A performance manipulated by algorithms.

Those crazy five-minute pump-and-dump schemes? 80% of them aren't natural buying. Nor are they panic selling.

It's liquidation hunting. It's that simple.

Two forces drive this market:

Market makers. They provide buffers. Liquidity. Stability.

The strong. The sharks. They don't trade—they're the hunters.

They hunt your stop-loss levels.

Your $50,000 stop-loss? To them, that's no risk. It's like a magnet.

When harmful order flows pile up—a wall of shorts here, a mountain of longs there—it's not unusual. It's a target drawn on the chart.

They saw it. Their algorithm saw it. They know exactly where the blood is.

And then, they trigger it.

TheKingfisher doesn't display moving averages; instead, it shows trading zones, liquidity cliffs, and massive liquidations preceding a crash.

The problem isn't whether the algorithm is trading;

the problem is whether you're focusing on the trading map or becoming prey for the trades.

This happens repeatedly, every single time. 👇

Have you noticed that the price always seems to "find" your stop-loss level?

This is no coincidence.

The algorithm maps out every trading cluster. $50,000? $48,500? They find trades piling up.

They wait for the most vulnerable moment—low volume, high leverage—and then trigger the trades.

The result? A series of liquidations that look like a "natural" sell-off.

But it's actually a trap, set and executed.

TheKingfisher highlights these liquidity cliffs in real time.

After the trades end, something strange happens.

The price doesn't continue to fall; instead, it quickly reverses.

Why did the algorithm just buy the cheap liquidity it created itself? They're not done yet. They're just preparing for the next move.

Retail investors see a "recovery," FOMO surges again—and they fall into the next trap.

This cycle repeats itself day after day, hour after hour.

The key isn't the price chart.

It's the liquidation heatmap.

Most traders ignore this level.

They only focus on RSI, MACD, and moving averages.

But these indicators are useless against an algorithm that pinpoints you precisely before you even set your stop-loss.

The Kingfisher Index doesn't predict prices.

It tells you where large sums of money are hidden.

Where liquidity is piling up.

Where the next buying frenzy will occur.

You can continue guessing.

Or, you can see the target directly.

33

311

39

Doctor Profit 🇨🇭

Crypto Newbie

17h ago

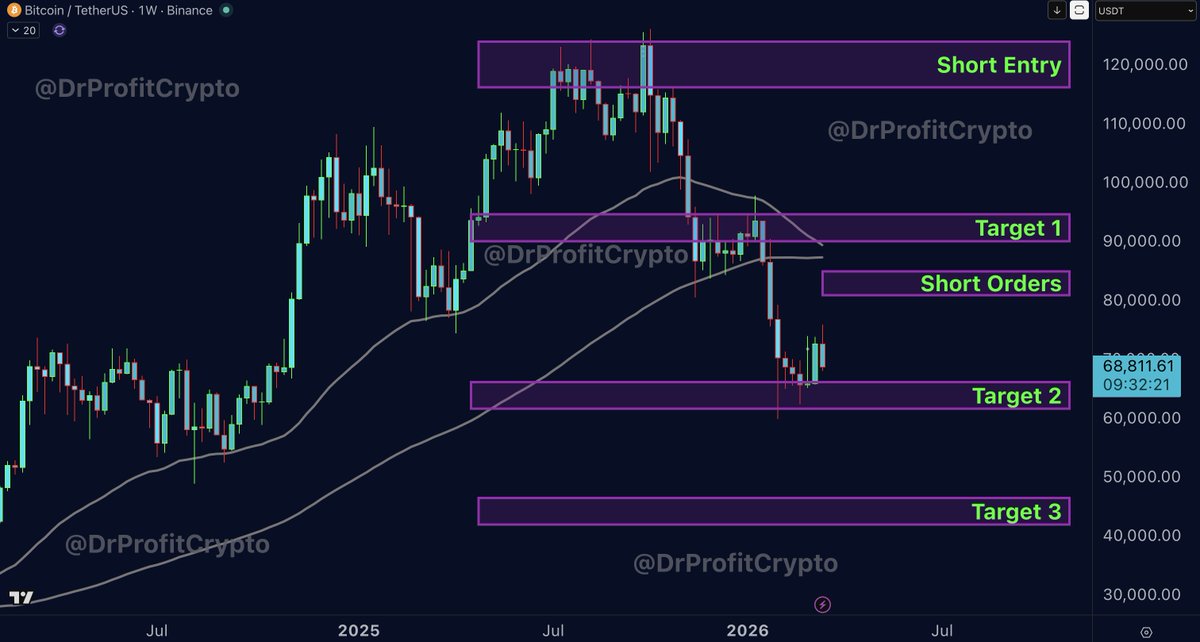

#Bitcoin – What's Next?

Sunday Breakout Report: Everything We Need to Know 🚩

Technical Analysis/Long-Term Analysis/Psychological Analysis: Since September 2025, I've been sharing my outlook and expectations for Bitcoin, as well as its movement over the next few months. At the short-term entry point of 115-125K, my initial target price was 100K, which was reached within weeks of my prediction. Afterward, I clearly pointed out that Bitcoin would experience a period of consolidation before dropping to 60K. At the time, this was hard to believe, but a few weeks later, everything unfolded as I predicted. At 60K, I predicted Bitcoin would enter a consolidation range between 57K and 87K. Bitcoin recently rose to 76K, but then fell sharply back to 68K just a few days later. Is this the bullish trap I've been referring to? Yes, this is one of the traps in this area before it continues to fall.

My strategy is very simple. I sold the Bitcoin I bought around $68,000 two weeks ago and now only hold a large short position between $115,000 and $125,000. I plan to add to this position with 5x leverage between $79,000 and $84,000, and these orders have already been placed. We are in a bear market, not only in the Bitcoin market but also in the entire stock market. Back in September, I pointed out the severe liquidity crunch in the repo market and the increasing risks of the Fed's standing repo facility. Furthermore, we are seeing continued manipulation in the silver and gold markets, with futures prices increasingly decoupled from physical supply, while physical supply continues to decline. Oil prices are rising, consistent with my analysis two months ago when I shorted Chevron, which is currently one of the biggest beneficiaries of these trends. Artificial intelligence and data-related stocks are severely overbought and over-invested. I shorted these sectors, and these positions were sold at a premium in November. Many stocks have fallen 30% to 40%, including PLTR, MSFT, and Coinbase. All my short positions are currently profitable. I am shorting Bitcoin. I am bullish on stocks (especially AI-related stocks) and stock indices in the UK, Germany, and Japan.

Which assets am I bullish on? Only a few: Chevron stock, physical metals, and oil. I also hold a long position in oil, which I bought two weeks ago at a premium of $84 and shared. This is my current portfolio allocation. I expect the bear market to dominate most assets, with only a select few remaining strong. Bitcoin is currently weak and lacks clear direction, which explains its continued sideways movement. However, the next major move could still be downward. Market makers are trying to push prices up to gain liquidity before pushing them down. Meanwhile, based on current data, they seem more cautious and hesitant to make any big moves due to the high risk associated with the macro and geopolitical environment.

Therefore, I have slightly adjusted my short entry range to 79-84K, and my orders are currently placed within that range. Prior to this, I will continue to hold a core short position of 115-125K. A few days ago, I mentioned XRP. Shortly after I entered the position, it rose 16%. However, I took profits and publicly stated that I ultimately closed the position with a gain of approximately 5%. The reason is simple: the risk-reward ratio was no longer as attractive as it was a few weeks ago, and considering the potential of Bitcoin's overall trend. This is also why I no longer hold Bitcoin spot. The next significant drop is only a matter of time. I don't rule out the possibility of a false drop before then, and if it does occur, I will use that opportunity to increase my short position, but overall, we are moving towards target 3 shown on the chart.

Last week's FOMC meeting gave us a clearer understanding of future trends. The next rate cut is expected in December 2026, much later than the market anticipated. I recall that the last time I announced a rate cut was in December 2025. People said we would see another rate cut at the next FOMC meeting. They were wrong. Now, watch the market panic spread. There's no sign of interest rate cuts, and according to the latest PPI and core PPI data, inflation is rising. Scary, isn't it? Did you know your left eye is connected to your right brain? The right brain is the center of emotions. Some people really need to be pirates to trade without being influenced by emotions. And now is the time to completely eliminate emotions. Market makers are manipulating emotions and psychology; prepare for massive manipulation before the next big drop. Liquidity pressures are intensifying; the 2008 crisis is repeating itself. I'm not predicting a September 2025 correction, but a major crash, and that's exactly where we're headed. I'm fully prepared; there are no buy orders between $57,000 and $60,000, only short orders between $79,000 and $84,000, just in case the market allows it.

I must emphasize that the Premium Membership offers the highest level of trading insight. All my steps, trades, and decisions are shared there in real time. Premium Membership not only always posts earlier than what's published on X, but also includes deeper analysis, clearer explanations, and most importantly, real-time execution. Position management, profit-taking levels, and detailed breakdown analysis are all included. At $59 per month, it's excellent value for money.

23

401

28

TheKingfisher

Infra

20h ago

Here's the disturbing truth most traders will never tell you:

Leverage isn't a tool; it's a time bomb you can't see.

You stare at those liquidation clusters on the chart, thinking it's just data. But it's not.

That's a trap being set.

The market actually works like this:

Large algorithmic traders don't care about your technical analysis; they only care about your stop-loss levels.

They scan the order book for liquidity, finding areas with the highest retail leverage.

Then, they precisely push the price up enough to trigger stop-loss levels.

Instantly, thousands of positions vanish, funds moving from your hands to theirs.

And what about the traders who aren't hit hard?

They spot the trap before it's triggered.

They know the hunt is coming because they see liquidity lining up like ducks.

TheKingfisher maps these areas in real time.

You can clearly see where the danger is concentrated and where algorithmic traders are searching.

It's not magic; it's simply seeing the strategies other players are using.

The key is not predicting price movements, but identifying structural weaknesses.

This is the advantage, and one that most traders overlook because they're busy drawing trend lines.

See the traps, avoid the traps.

This is the way to survive.

View the chart. 👇

36

473

37