Topic Background

Bitcoin tycoon daheng.btc

Crypto Newbie

1h ago

Now all I can say is ten words: Contracts are risky, trade with caution.

This SIREN had a market capitalization of over 3 billion USD at its peak. Do you know what that means? It's just a small player in BSC.

Most of the chips are in the hands of the big players. Short sellers are in trouble; I was a victim of shorting yesterday.

The bears can't hold on any longer; it's almost over. The big players have taught us a lesson: making money doesn't depend on timing.

#SIREN

31

348

24

Sponge Evolution Theory

Crypto Newbie

1h ago

Compared to TRB:

TRB surged 60 times from its low, reaching a market capitalization of $2.5 billion.

SIREN almost replicated the same pattern, reaching a market capitalization of $3 billion, a nearly 70-fold increase.

I predict SIREN might eventually become like TRB, but be careful not to short it! You can see it rise 100-200% while falling!

Even market makers are trapped. Could it be the same manipulator using the same tactics to drive up the price?

Besides shorting leading to liquidation, isn't that how contracts work?

You can get rich quick, or you can lose everything.

If you ask me,

If hundreds or thousands of times a day

were happening every day,

wouldn't liquidity in the crypto market return?

Wouldn't the altcoin boom arrive?

That's how it should be done, a massive pump and dump.

#siren

37

465

26

Bitcoin Wukong (Bull)

Crypto Newbie

2h ago

This SIREN surge wasn't due to a sudden "fundamental explosion," but rather an accelerated market movement created by a combination of factors: a repricing of the AI Agent narrative, a return of funds to the BNB Chain, short squeezes in contracts, and a highly controlled supply structure.

My advice: don't go long or short; you'll never beat the market makers. The odds of winning are lower than in baccarat.

20

456

26

Cilantro Talks Crypto

Crypto Newbie

3h ago

No one dumped the shares after the lockout?

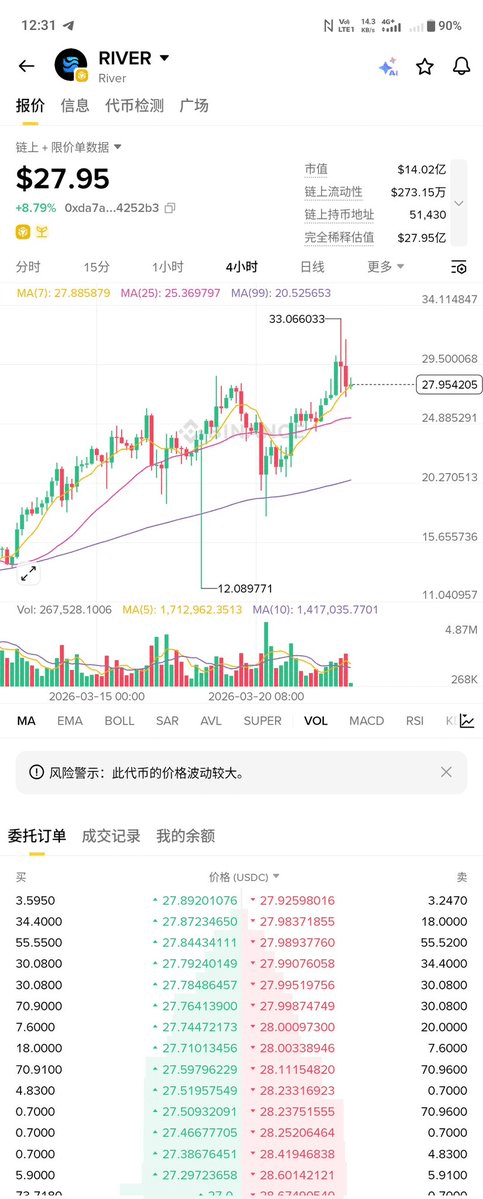

$River surged to $33 in the early morning, but has now fallen back to around $28! Another day of suffering for short positions~

As of approximately early morning on March 23, 2026, the River contract's trading volume over the past 24 hours is as follows:

Long position volume: Approximately $748 million

Short position volume: Approximately $695 million

Difference in trading volume between long and short positions: Long positions lead by approximately $53 million (longs account for approximately 51.8%, shorts approximately 48.2%)

It's advisable to observe more and act less, and avoid high leverage when trading contracts, as you risk being liquidated in both long and short positions!

41

313

39

Analyst Shu Qin

Crypto Newbie

3h ago

Gold has crashed! It plummeted from 5600 to 4200! Is now a good time to buy the dip? I'm thinking of trying a small position.

Currently, gold's support is around 4100-4200, roughly around 4120. You could consider buying some spot gold within this support range. This might be a temporary bottom, and there should be a significant rebound, possibly even reaching 4500+. As long as the 4000 support level holds, there's a good chance of a rebound.

Gold is listed on major exchanges as XAU, XAUT, and PAXG.

For contracts, it's called XAU/USDT or XAUT/USDT. The one with a price around 4000 is gold.

If you're holding spot gold around 4100-4200 and are currently holding at a loss, you can hold it. Getting out of the loss shouldn't be a problem. For contracts, you should cut your losses if it slightly falls below 4000.

I'm allocating about 10% of my capital to this; my main positions are in crypto and US stocks, so I don't need to trade gold.

37

318

34

FinanceRun

Crypto Newbie

3h ago

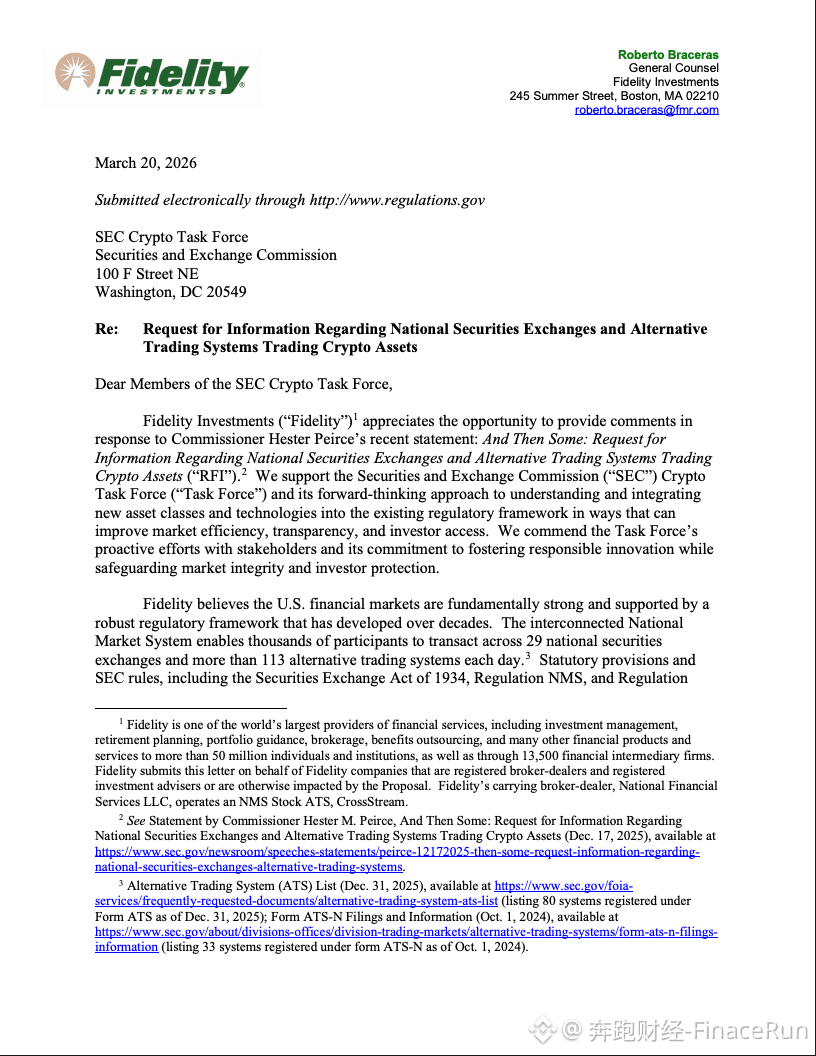

Fidelity Sends Letter to SEC: Tokenized Asset Regulation Should Not Be "One Token, One Rule," Differentiated Rules and Regulatory Models Needed

On March 22, Fidelity Investments, a US asset management company, sent a letter to the US Securities and Exchange Commission (SEC), responding to the SEC's earlier public comment period.

In the letter, Fidelity Investments called on the SEC to further refine its regulatory framework, primarily addressing matters related to brokers offering, custodian, and trading crypto assets on alternative trading systems (ATS).

The letter emphasized that developing a comprehensive regulatory framework and clear rules for trading tokenized securities is "crucial," including rules governing the trading of tokenized securities issued by third parties.

The letter pointed out that tokenized instruments have different issuance structures, legal attributes, and valuation models. For example, tokenized real-world assets (RWAs) encompass entirely different asset classes such as stocks, real estate, bonds, or private credit.

Fidelity further explains that tokenization models differ significantly in structure and the rights granted to holders. Some models allow indirect access to underlying securities through security interests, while others restrict participation to qualified contract investors based on security swaps.

This structural difference means the tokenization market is already "layered," requiring regulatory oversight that avoids a one-size-fits-all approach. Differentiated rules must be developed for different models; otherwise, compliance is impossible.

Furthermore, because DeFi financial trading platforms lack a central authority and cannot generate detailed financial reports as required by the SEC, Fidelity urges the SEC to bridge the regulatory gap between CeFi and DeFi trading systems and consider how they should evolve and coexist.

In response, Fidelity recommends that the SEC issue guidance allowing brokers to utilize distributed ledger technology for alternative trading systems and other record-keeping, aiming to alleviate unnecessary financial reporting burdens for decentralized systems by modifying reporting requirements.

In summary, Fidelity's letter reveals that some RWAs are merely digital shells of traditional securities, while others have become high-barrier contract derivatives, clearly inconsistent with a unified market regulatory logic.

Fidelity's demands are straightforward: either break down the rules into smaller, more manageable sections, or stifle innovation in the industry. The SEC's response will determine how fast CeFi can grow and how far the DeFi world can go.

#TokenizedSecurities

46

336

30

Stephen | DeFi Dojo

Crypto Newbie

5h ago

Last night's Resolv vulnerability incident was a very unique experience for me because I was in an informal meeting with @mezzanine_fi's core team, so we were monitoring the situation in real-time from the minutes it occurred (being notified via @HypernativeLabs).

First, thanks to @SaulCapital and @yieldsandmore, who were among the first teams to discover the vulnerability and notify the community.

As a result, within minutes, Discord and Telegram groups began working to mitigate the risk.

Impressively, @infiniFi was able to quickly analyze and eliminate all exposure with zero loss. They also mentioned that @pagerduty played a crucial role in waking up/notifying all relevant team members and taking action almost immediately.

@SteakhouseFi also quickly mitigated all exposure, and to my knowledge, they were the first curators to announce the risk reduction progress.

@reservoir_xyz also quickly analyzed their exposure at Steakhouse and updated everyone on the progress.

In YAM and DeFi Dojo, various arbitrage opportunities were analyzed in real time. I'm proud and encouraged that no one on Dojo promoted malicious lending strategies on Fluid. Instead, they focused on more ethically pegged arbitrage strategies on DOLA and GHO, actively analyzing all second-order risks so the community could act quickly.

Services like Hypernative and PagerDuty are clearly crucial for real-time detection of de-pegged and questionable minting, and I strongly recommend all protocols and risk analysis enthusiasts include tools like Hypernative in their core toolkits.

It's heartbreaking to see @0xfluid affected; it's a protocol I really like, and I love my team, even though they occasionally make some strong statements on Twitter. Even so, they seem to have found a way forward, and I'll certainly be there to support them.

I also hope @ResolvLabs can find a solution, because technically, the underlying assets of Resolv are not affected. The most affected are primarily liquidity providers (LPs) and the lending market.

Key takeaways:

- Lending markets no longer hardcode stablecoins as 1.

- Minting and redemption (of all sizes) requiring only KYC verification can generally mitigate minting vulnerabilities.

- Governance needs to be 24/7, therefore infrastructure must be built to allow liquidity withdrawals/risk mitigation when necessary.

- Monitoring services should be available to everyone.

- Liquidity providers remain the most vulnerable targets in minting vulnerability attacks.

- Operational security (OpSec) is not a secondary issue; it needs to be given equal importance to smart contract risks (note).

48

486

31

I am not a ghost lamp.

Binance

7h ago

Lately, I haven't had enough money to close deals, so my life has become more structured. I go out for dinner after work and go to bed at 11 pm. My work efficiency has also improved; the workshop foreman and line leader even praised me for being quick. Before, when I had contracts, I would constantly check to see if I was making money. If I was stuck with losses, I wouldn't sleep a wink all night; I was constantly anxious. When I lost money, I felt like cursing, smashing things, and throwing my phone.

38

373

28

Bitcoin Commander

Crypto Newbie

8h ago

3.23 Bitcoin Price Analysis: The smaller timeframe structure of Bitcoin indicates that the third downward move is nearing its end. Shorting should be approached with caution. Uncertainty remains in the larger timeframe, and there is a risk of major players reversing course and manipulating the price to absorb short-selling liquidity. (Bitcoin Futures Trading) Commander

25

369

40