作者:Wall Street CN

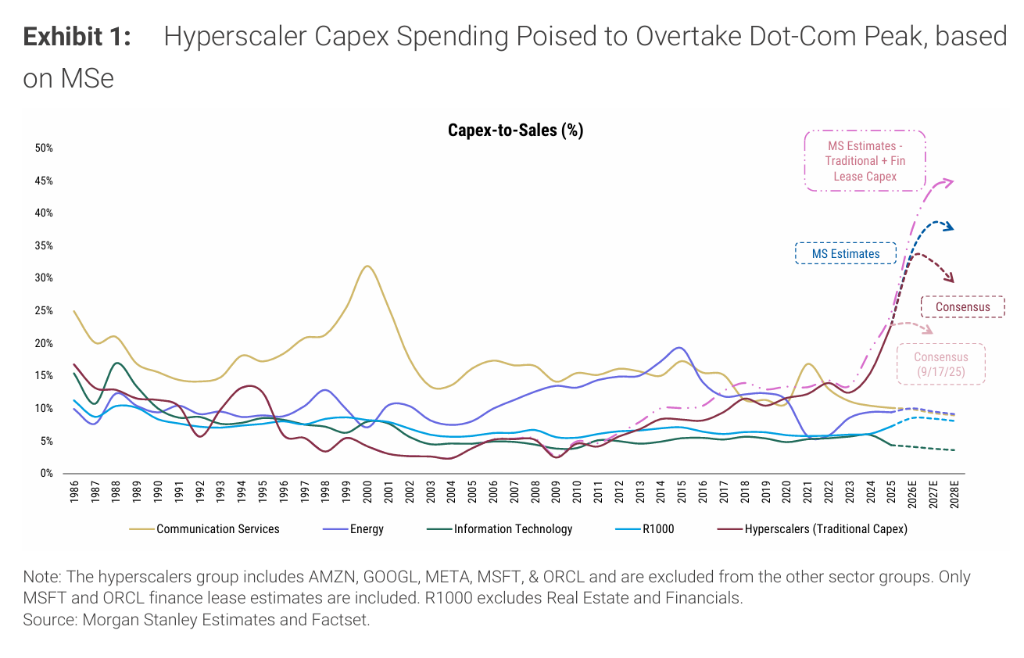

The wave of investment in AI infrastructure is propelling tech giants into an unprecedented asset-heavy cycle. A recent study by Morgan Stanley shows that hyperscale cloud providers, including Amazon, Google, Meta, Microsoft, and Oracle, are expected to surpass their historical peak capital expenditures during the dot-com bubble era, indicating a structural shift in the business models of the tech industry.

According to a report released by Morgan Stanley on February 26, 2026, the bank expects the capital expenditure-to-sales ratio of the aforementioned five hyperscale cloud service providers to be higher.It is projected to reach 34%, 39%, and 37% in 2026, 2027, and 2028 respectively, surpassing the peak of approximately 32% during the dot-com bubble era.

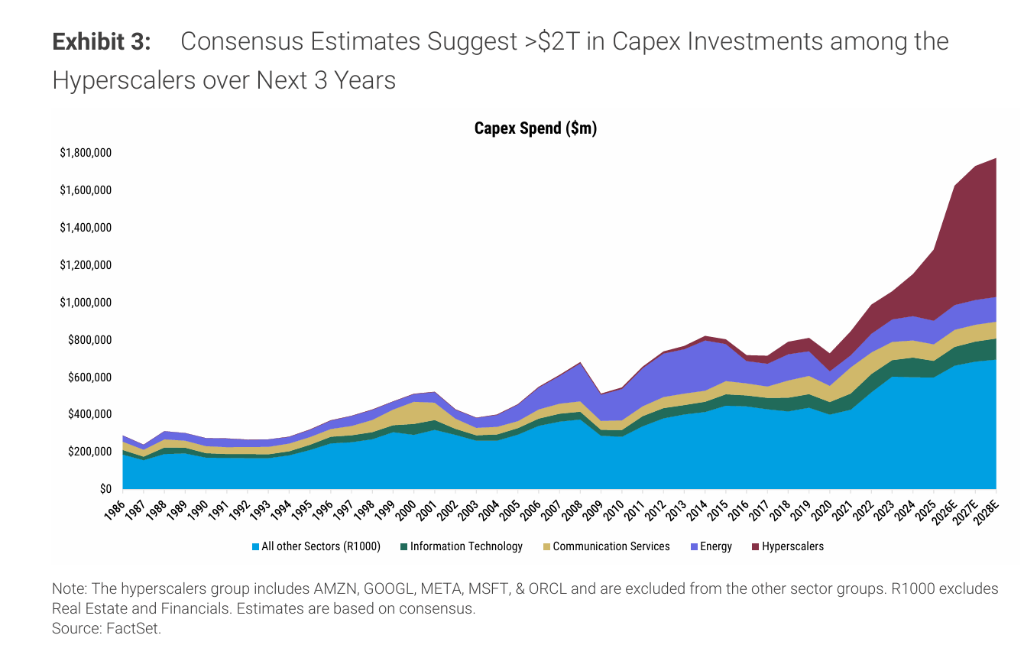

If finance leases are included in the calculation, this proportion will further climb to 38%, 44%, and 45%. Meanwhile, the total capital expenditures of these companies over the next three years will exceed $2 trillion, representing approximately 40% of the total capital expenditures of the Russell 1000 index constituents.

However, the explosive expansion of capital expenditures did not translate into a corresponding upward revision of revenue. Morgan Stanley points out that...Over the past six months, the market consensus forecast for capital expenditures in 2026 and 2027 has been revised upward by more than $630 billion, but the revisions to revenue forecasts have been far less significant, resulting in a continued decline in the expected free cash flow (FCF) of hyperscale cloud service providers.In contrast, semiconductor AI-enabled companies have seen their 2026 sales revenue consensus forecasts revised upward by about 60% over the past two years, far exceeding the approximately 8% increase for hyperscale cloud service providers, making them the most direct financial beneficiaries in this round of AI investment cycle.

Capital intensity surpasses historical highs of the dot-com bubble.

In its report, Morgan Stanley noted that six months ago it characterized the AI construction boom as "approaching but not yet surpassing" the capital intensity of the fiber optic construction peak during the dot-com bubble.The latest forecasts indicate that capital intensity will "far exceed" the peak of the dot-com bubble, which was about 32%, with capex-to-sales projected to reach 34%, 39%, and 37% in 2026, 2027, and 2028, respectively.

The report also emphasizes that measuring this investment cycle solely by traditional capital expenditures underestimates its scale. Financial leasing, essentially acquiring assets through debt, should be included in the overall investment assessment. While financial leasing was virtually nonexistent during the dot-com bubble, hyperscale cloud service providers are currently signing data center leases totaling hundreds of billions of dollars. Morgan Stanley software industry analysts predict that the financial leasing capital expenditures of Microsoft and Oracle alone will be enough to push the overall hyperscalers' capex-to-sales ratio to 38%, 44%, and 45% in 2026, 2027, and 2028, respectively.

In terms of impact on the Russell 1000 index, hyperscale cloud service providers accounted for over 150% of the index's capital expenditure increase in 2025—meaning that the capital expenditure of the remaining constituent stocks was actually in a net contraction. Hyperscale cloud service provider capital expenditure increased by approximately 70% year-on-year, while the remaining constituent stocks declined by 6%. Morgan Stanley projects that by 2026, hyperscalers will account for approximately 40% of the Russell 1000's total capital expenditure, doubling from 2024, and potentially jumping further to 49% by 2028.

Capital expenditure revisions hit a record high, while revenue forecasts lagged significantly.

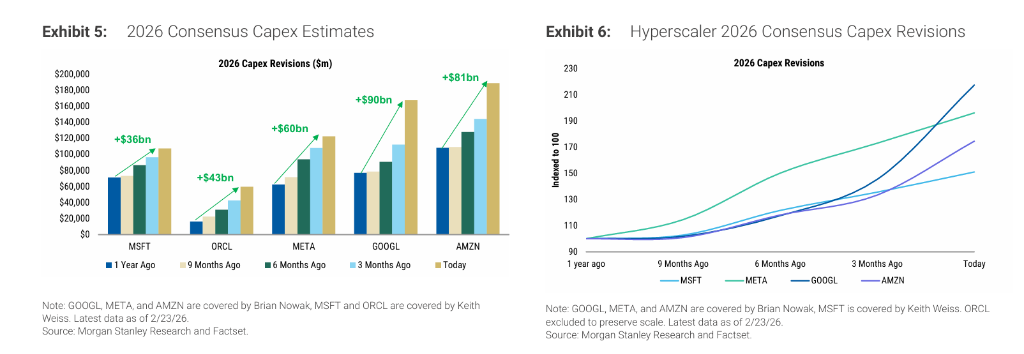

A notable feature of this investment cycle is the unprecedented speed and magnitude of upward revisions to capital expenditure forecasts. Since September 2025, the market consensus forecast for hyperscalers' capital expenditures in 2026 and 2027 has been revised upward by approximately 1.5 times each, while Morgan Stanley's own analyst forecasts have been revised upward by as much as approximately 1.8 times.

From the perspective of an individual company,Google's consensus forecast for capital expenditures in 2026 has been revised upward by 117% compared to a year ago, META by 96%, Amazon by 75%, and Oracle by a staggering 264%.Morgan Stanley analyst Todd Castagno's team pointed out that these revisions are characterized by "step-like" rather than gradual adjustments, indicating that this investment cycle is extremely difficult to predict—management's continuous updates to data center expansion plans and companies' scramble to secure key supply chains further increase the difficulty of forecasting.

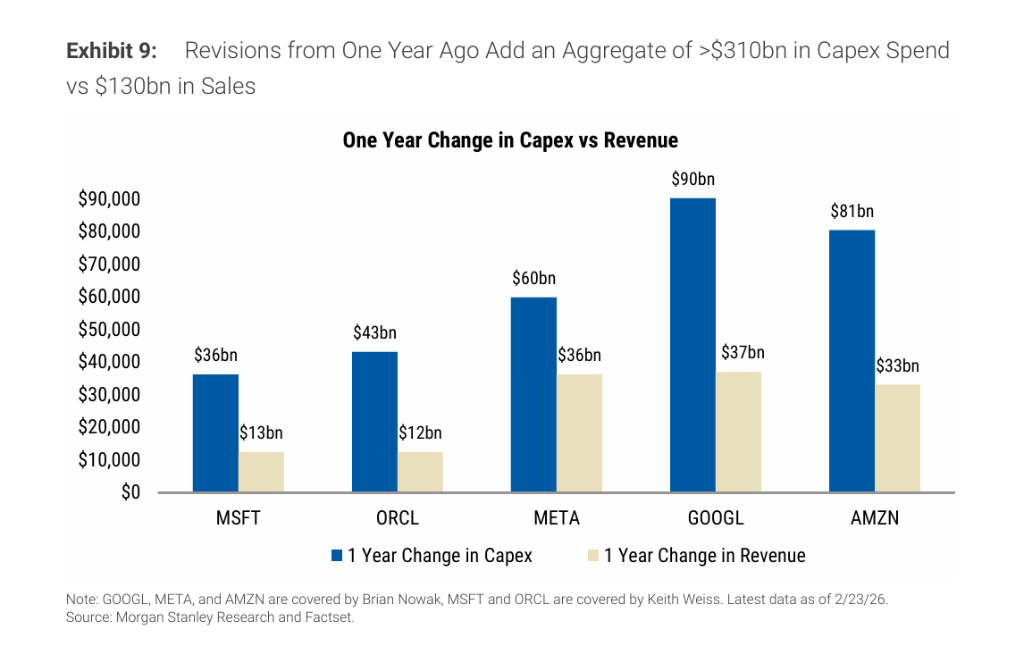

This contrasts sharply with the rapid upward revision of capital expenditure expectations.Revenue revisions remained virtually unchanged, while FCF expectations declined accordingly.The report shows that in the past year's 2026 forecasts, the five companies have increased their capital expenditures by a total of over $310 billion, while their revenue revisions total only about $130 billion. Morgan Stanley points out that as their fixed cost base continues to expand, these companies' operating leverage will rise accordingly, and their future earnings and FCF will become significantly more sensitive to changes in revenue expectations.

Financial leasing significantly amplifies the actual investment scale

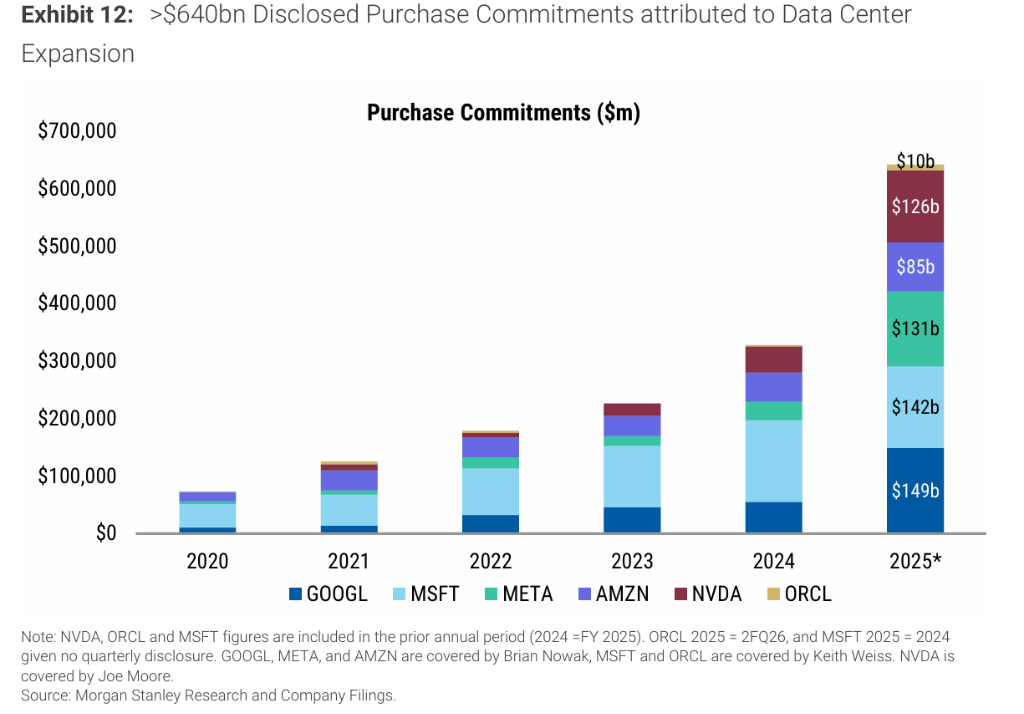

Hyperscale cloud service providers have recently significantly expanded their use of financial leasing, further increasing their actual capital intensity. As of the latest company financial reports, these five companies have committed over $660 billion in future leases, with Oracle at approximately $248 billion, Microsoft at approximately $155 billion, Meta at approximately $104 billion, Amazon at approximately $96 billion, and Google at approximately $59 billion. Notably, Google's lease commitments have increased approximately sevenfold since 2024, while Meta's have increased by over 200% during the same period.

Financial leasing has a particularly significant impact on the capital strength of individual companies.Taking Microsoft as an example, if only traditional capital expenditures are considered, its capex-to-sales ratio was approximately 29% in FY26 and FY27. After including finance leases, this ratio will jump to approximately 43% and 42%, respectively. Oracle's situation is even more extreme—the company is acquiring all its data center enclosures through leasing. Under traditional accounting methods, Oracle's capex-to-sales ratio is projected to be 75% and 119% in FY26 and FY27, respectively. After including finance leases, it will climb to 107% and 201%, respectively, meaning that the total reinvestment in both fiscal years will exceed the total revenue of that year.

Semiconductor manufacturers are the biggest winners, while hyperscale cloud service providers still need to prove their worth.

Although capital expenditures are highly concentrated in hyperscale cloud service providers, the group that has benefited most clearly in the recent investment cycle is semiconductor AI-enabled companies.

The fundamental reason for this divergence lies in the difference in income certainty:Hyperscale cloud service providers have made large-scale purchases of GPUs and other chip components in advance, providing chip suppliers with a clear and immediate source of revenue. Hyperscalers, on the other hand, will need to gradually monetize these computing assets over the next few years, relying on the monetization of large language models, continuous computing power demand, and product differentiation. This process carries greater uncertainty.

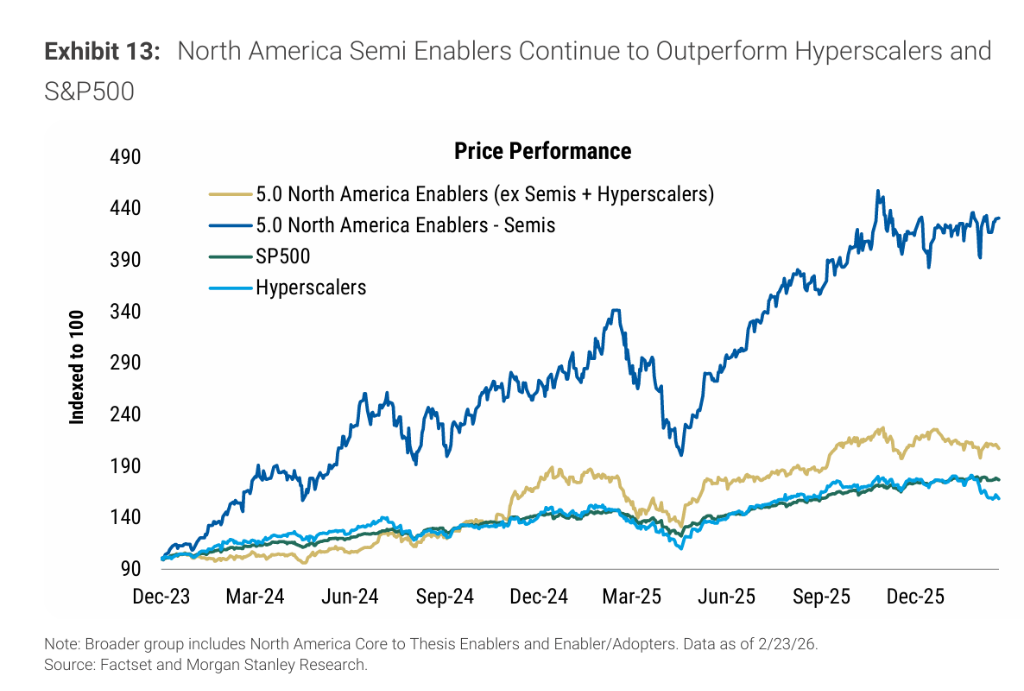

The performance of the capital market also confirms this divergence of logic. Since December 2023, the stock price increases of North American semiconductor AI-enabled companies have exceeded those of hyperscale cloud service providers and the broader AI-enabled sector by 272% and 224%, respectively. The market is currently more willing to pay a premium for the near-term earnings already confirmed by semiconductor companies, while choosing to continue to wait and see regarding the revenue realization paths of hyperscalers and the broader AI-enabled group.

Morgan Stanley analyst Brian Nowak believes that Meta, Google, and Amazon are leveraging AI investments, data accumulation, and economies of scale to accelerate user engagement and monetization. Keith Weiss characterizes Oracle's data center expansion as a potential revenue opportunity, but emphasizes that it requires substantial financial support. The current trend of upward revisions to capex will also lead to a continued rise in depreciation expenses, which, given that sales revenue has not been revised upwards accordingly, will put significant pressure on profit margins.

~~~~~~~~~~~~~~~~~~~~~~~~

The above exciting content comes from

For more detailed analysis, including real-time updates and firsthand research, please join [the group/group].