Fidelity Sends Letter to SEC: Tokenized Asset Regulation Should Not Be "One Token, One Rule," Differentiated Rules and Regulatory Models Needed

On March 22, Fidelity Investments, a US asset management company, sent a letter to the US Securities and Exchange Commission (SEC), responding to the SEC's earlier public comment period.

In the letter, Fidelity Investments called on the SEC to further refine its regulatory framework, primarily addressing matters related to brokers offering, custodian, and trading crypto assets on alternative trading systems (ATS).

The letter emphasized that developing a comprehensive regulatory framework and clear rules for trading tokenized securities is "crucial," including rules governing the trading of tokenized securities issued by third parties.

The letter pointed out that tokenized instruments have different issuance structures, legal attributes, and valuation models. For example, tokenized real-world assets (RWAs) encompass entirely different asset classes such as stocks, real estate, bonds, or private credit.

Fidelity further explains that tokenization models differ significantly in structure and the rights granted to holders. Some models allow indirect access to underlying securities through security interests, while others restrict participation to qualified contract investors based on security swaps.

This structural difference means the tokenization market is already "layered," requiring regulatory oversight that avoids a one-size-fits-all approach. Differentiated rules must be developed for different models; otherwise, compliance is impossible.

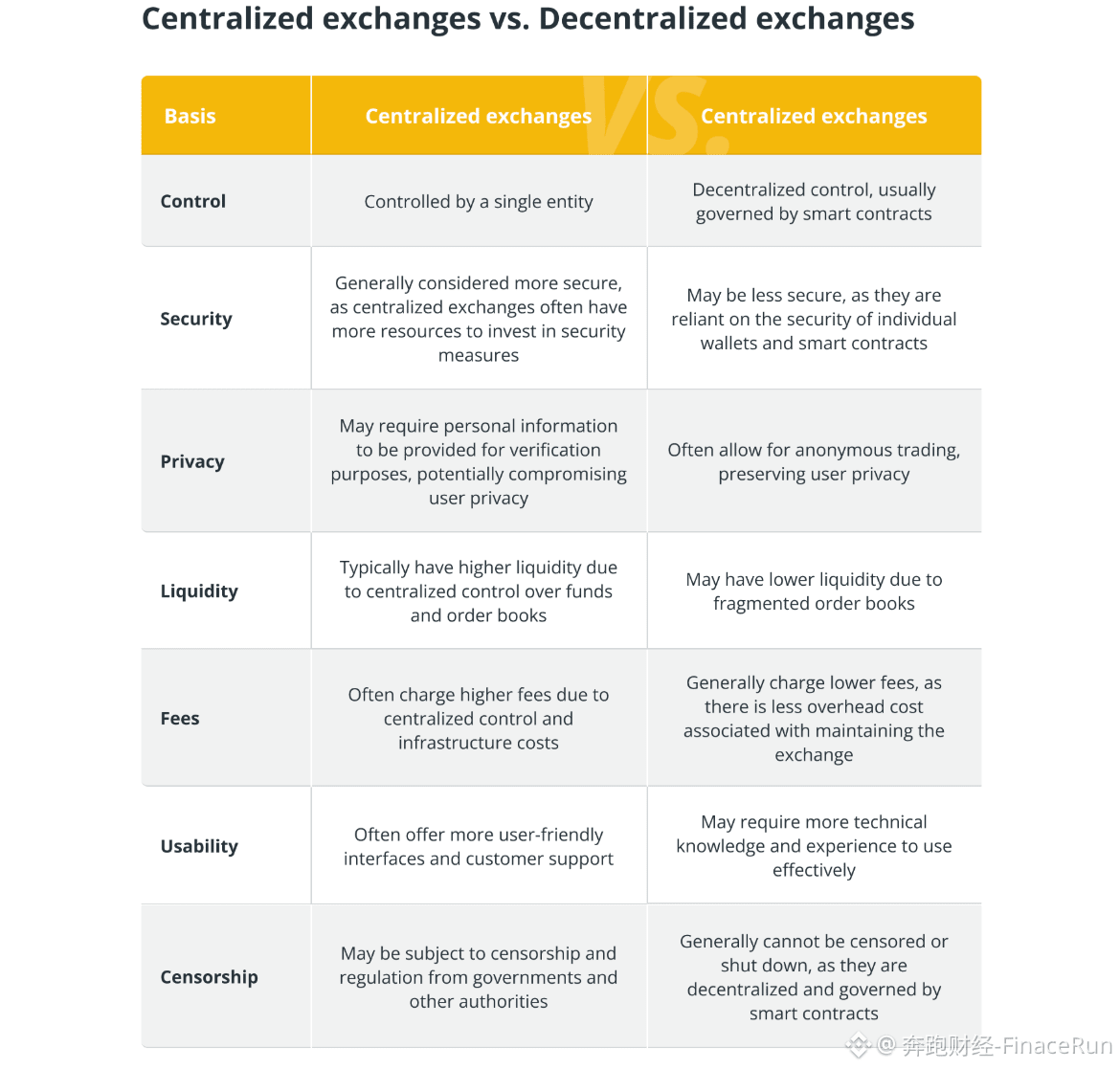

Furthermore, because DeFi financial trading platforms lack a central authority and cannot generate detailed financial reports as required by the SEC, Fidelity urges the SEC to bridge the regulatory gap between CeFi and DeFi trading systems and consider how they should evolve and coexist.

In response, Fidelity recommends that the SEC issue guidance allowing brokers to utilize distributed ledger technology for alternative trading systems and other record-keeping, aiming to alleviate unnecessary financial reporting burdens for decentralized systems by modifying reporting requirements.

In summary, Fidelity's letter reveals that some RWAs are merely digital shells of traditional securities, while others have become high-barrier contract derivatives, clearly inconsistent with a unified market regulatory logic.

Fidelity's demands are straightforward: either break down the rules into smaller, more manageable sections, or stifle innovation in the industry. The SEC's response will determine how fast CeFi can grow and how far the DeFi world can go.

#TokenizedSecurities

Price Converter

- Crypto

- Fiat

USDUnited States Dollar

CNYChinese Yuan

JPYJapanese Yen

HKDHong Kong Dollar

THBThai Baht

GBPBritish Pound

EUREuro

AUDAustralian Dollar

TWDNew Taiwan Dollar

KRWSouth Korean Won

PHPPhilippine Peso

AEDUAE Dirham

CADCanadian Dollar

MYRMalaysian Ringgit

MOPMacanese Pataca

NZDNew Zealand Dollar

CHFSwiss Franc

CZKCzech Koruna

DKKDanish Krone

IDRIndonesian Rupiah

LKRSri Lankan Rupee

NOKNorwegian Krone

QARQatari Riyal

RUBRussian Ruble

SGDSingapore Dollar

SEKSwedish Krona

VNDVietnamese Dong

ZARSouth African Rand

No more data