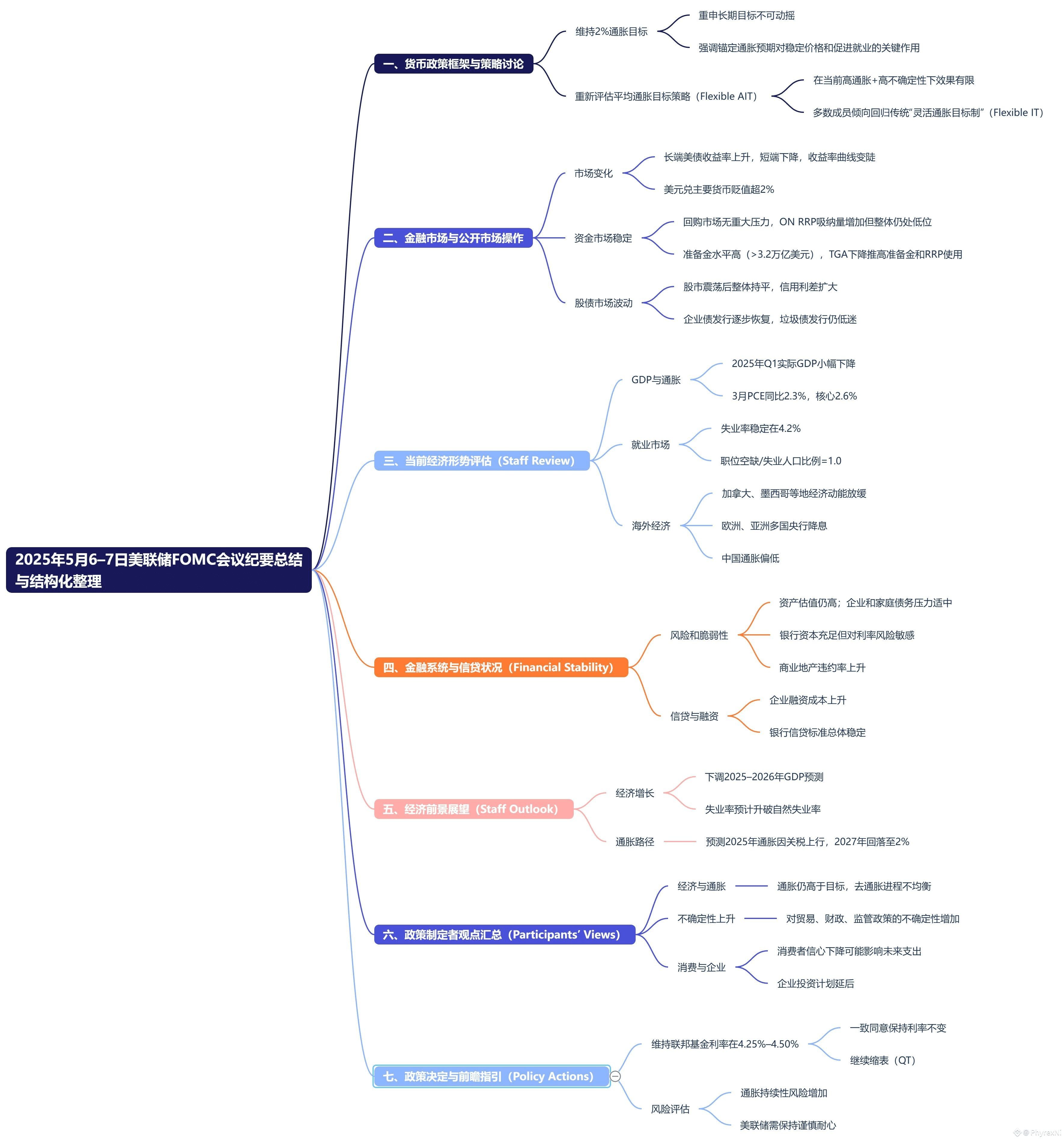

The Federal Reserve has just released the minutes of its March meeting, which focused on responding to the "policy framework adjustment" mentioned by Powell last time. The minutes show that the participants reiterated that the long-term inflation target of 2% is unshakable, and emphasized that anchored inflation expectations are critical to maintaining price stability and promoting employment.

In the past, when interest rates were close to the zero lower bound (ELB), the Federal Reserve adopted an average inflation target (AIT), that is, allowing inflation to be higher than 2% for a period of time to compensate for the long-term below target. However, in the current environment of high inflation and high uncertainty, most members believe that the effect of this strategy has been greatly weakened, and they tend to return to the traditional "flexible inflation targeting system" (FIT).

Simply put, flexible inflation targeting is the method currently used by most central banks. It means that the central bank sets a clear inflation target (such as 2%), but does not force it to hit it accurately at all times. Instead, it allows inflation to fluctuate within a certain range and flexibly adjusts monetary policy in combination with factors such as economic growth and employment.

In other words, the central bank can tolerate inflation below or above 2% in the short term, as long as it can roughly return to the target in the medium term. However, this does not mean that there is a major change in the current policy path. The real significance is how the central bank should fine-tune the policy pace after inflation approaches 2%, so the impact on the current market is very limited.

Because the other content is based on March, I personally think it is not very meaningful, so I did not list them one by one. The main content is placed in the mind map.

This tweet is sponsored by @ApeXProtocolCN|Dex With ApeX