Author:BlockBeats

Text | Kaori

The NASDAQ system went live on February 8, 1971.

There was no trading floor, no bell-ringing ceremony; it was simply an electronic quotation terminal connecting over-the-counter traders scattered across the United States. A broker at the NYSE glanced at it and dismissed it. For two hundred years, the rule of stock trading had been to walk into that building, stand on that floor, and bid face-to-face. What could a screen change?

Twenty years later, Intel, Microsoft, and Apple successively listed on NASDAQ, and the era of tech stocks reshaped the Wall Street landscape. The NYSE began to catch up, acquiring the electronic trading platform Archipelago in 2006.

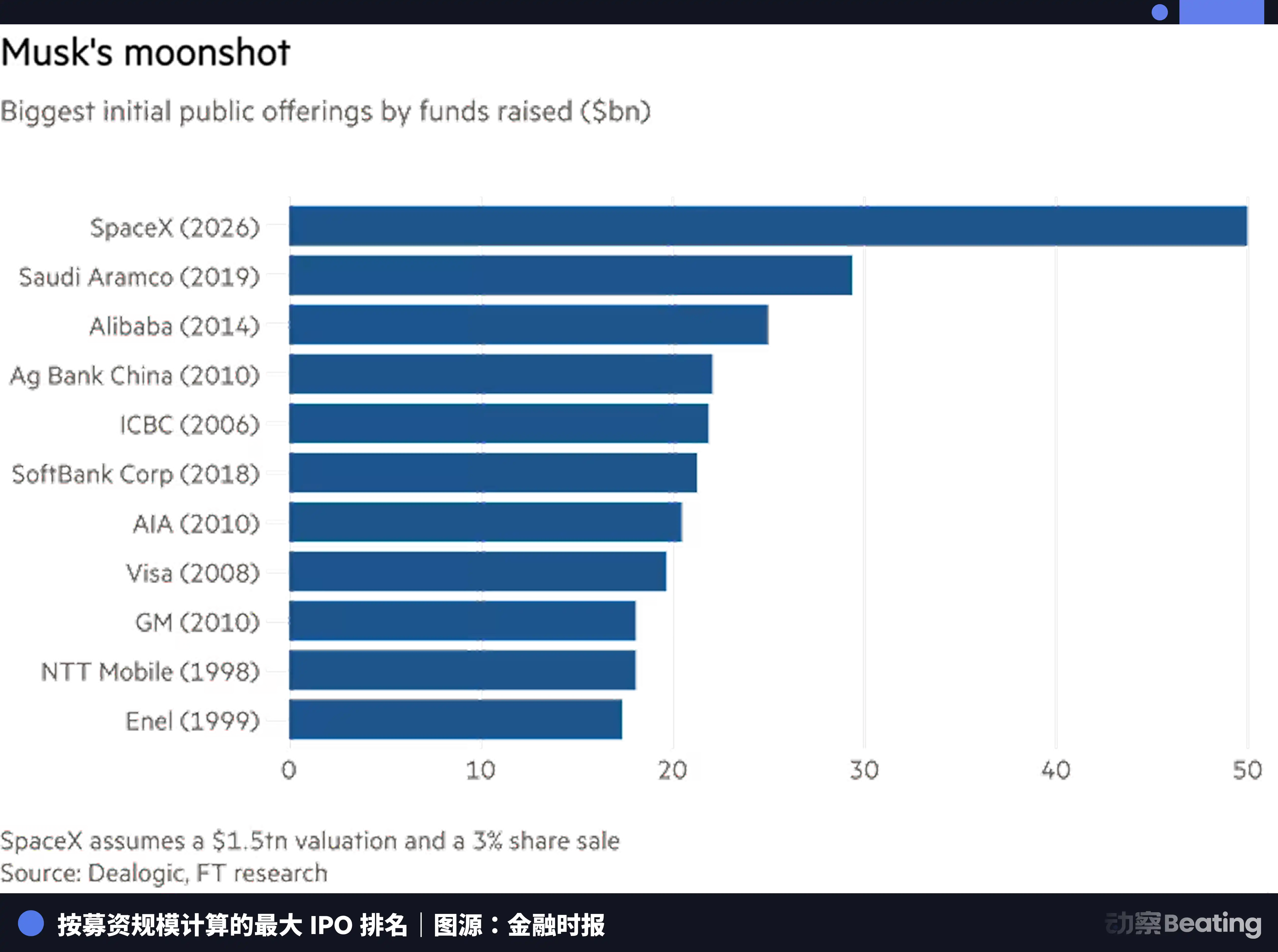

Twenty years from now, in 2026, SpaceX is in talks with Nasdaq, demanding inclusion in the Nasdaq 100 index within 15 trading days of its listing. If that's not possible, it can go to the NYSE.

Each time, the rules yield to enough power, but this time is different.

The rise of Nasdaq in 1971 was a new type of exchange using technology to disrupt old rules. The transformation of the NYSE in 2006 was an old exchange surrendering to new technology. And the scenario in 2026 is a company that hasn't even gone public yet demanding that a two-hundred-year-old market system change its processes for it.

This is not just a story about SpaceX going public, but also a snapshot of a shift in the direction of gravity in the capital markets.

Financing opportunities are no longer exclusive to IPOs.

What is the purpose of going public? The textbook answer is to raise funds.

This answer was accurate in the 1990s. Back then, the public market was practically the only place to provide companies with large-scale, long-term capital. SoftBank hadn't yet established its Vision Fund, sovereign wealth funds avoided tech stocks, and the private secondary market was virtually nonexistent. To get truly substantial funding, there was only one path: knock on the door of the stock exchange, undergo auditing, scrutiny, and pricing, and then pray for a successful roadshow.

Microsoft went public on NASDAQ on March 13, 1986, raising $61 million and valuing the company at approximately $777 million. At the time, the company's annual revenue was less than $200 million. It needed that money to expand its product line, recruit engineers, and seize the standard position in the PC operating system market.

Forty years later, this logic is no longer the only answer.

SoftBank Vision Fund, Tiger Global, Coatue, a16z… an entire ecosystem of institutional capital has pushed the amount of ammunition in the private equity market to an unprecedented scale. A company can grow all the way to a valuation of 50 billion or even higher in the private equity market without ever touching the public market.

Revolut is the most direct proof. On November 24, 2025, the London-based digital bank completed a secondary equity transfer, valuing the company at $75 billion. Lead investors included Coatue, Greenoaks, Dragoneer, and Fidelity, with participants including a16z, Franklin Templeton, and even Nvidia's venture capital arm, NVentures.

The company reported full-year revenue of $4 billion in 2024, a 72% year-over-year increase, and pre-tax profit of $1.4 billion. When asked about the IPO timeline, CEO Nik Storonsky stated: "We are building the world's first truly global bank; an IPO is not a priority."

What does $75 billion mean? This figure exceeds the market capitalization of Barclays, Deutsche Bank, and Lloyds Bank in the public market. A private company has received a higher price tag than publicly traded banks in a private transaction.

Recently, there have been reports that Revolut plans to conduct another round of secondary share sales in the second half of 2026, with a valuation of $100 billion.

SpaceX completed a similar strategic move earlier, with its private funding rounds covering the full capital needs of its three product lines: rocket development, Starlink deployment, and deep space exploration. According to Reuters, SpaceX plans an IPO with a valuation of approximately $1.75 trillion. If successful, it would be the largest IPO in history and would immediately rank sixth in market capitalization in the US, behind only Nvidia, Apple, Microsoft, Amazon, and Alphabet.

Then there's Stripe, the payments company that processed $1.9 trillion in transactions in 2025, a 34% year-over-year increase. In February 2026, through an employee stock buyback, its valuation reached $159 billion. Co-founder John Collison put it bluntly in an interview: "For us, the IPO was just 'finding a solution to a problem.'"

These companies are not going public not because of a poor market environment, but because they no longer have such an urgent need for funds from the public market. The private market provides the same amount of capital, but with fewer regulatory constraints and disclosure requirements.

But not needing money doesn't mean you don't need to go public.

Entering the index, the real spoils of war

Financing is only the first motivation for going public; the second is the liquidity of people.

SpaceX has thousands of employees holding stock options and RSUs. In the past few years, the company has allowed some employees to cash out their stock options early through tender offers. However, this method has limits on the amount and frequency of such offers, and the pricing is determined by the company, not by the market.

For a company with tens of thousands of employees, this channel is too narrow. Only the open market can provide a true, continuous, market-priced outlet for liquidity.

The same pressure exists on the VC side. Revolut's shareholder list includes a16z, Fidelity, and Coatue. These funds' LPs don't need growth in paper valuations; they need tangible cash returns. The private secondary market can address some exit needs, but its scale and efficiency are far inferior to the public market. When a fund matures, LPs want to take their money and leave; paper wealth doesn't count.

So these companies still want to go public, but the combination of variables driving them has changed. Fundraising needs have decreased significantly, while employee liquidity and VC exits remain essential. Beyond these traditional motivations, a structural force that has been underestimated by most over the past decade is rapidly gaining weight.

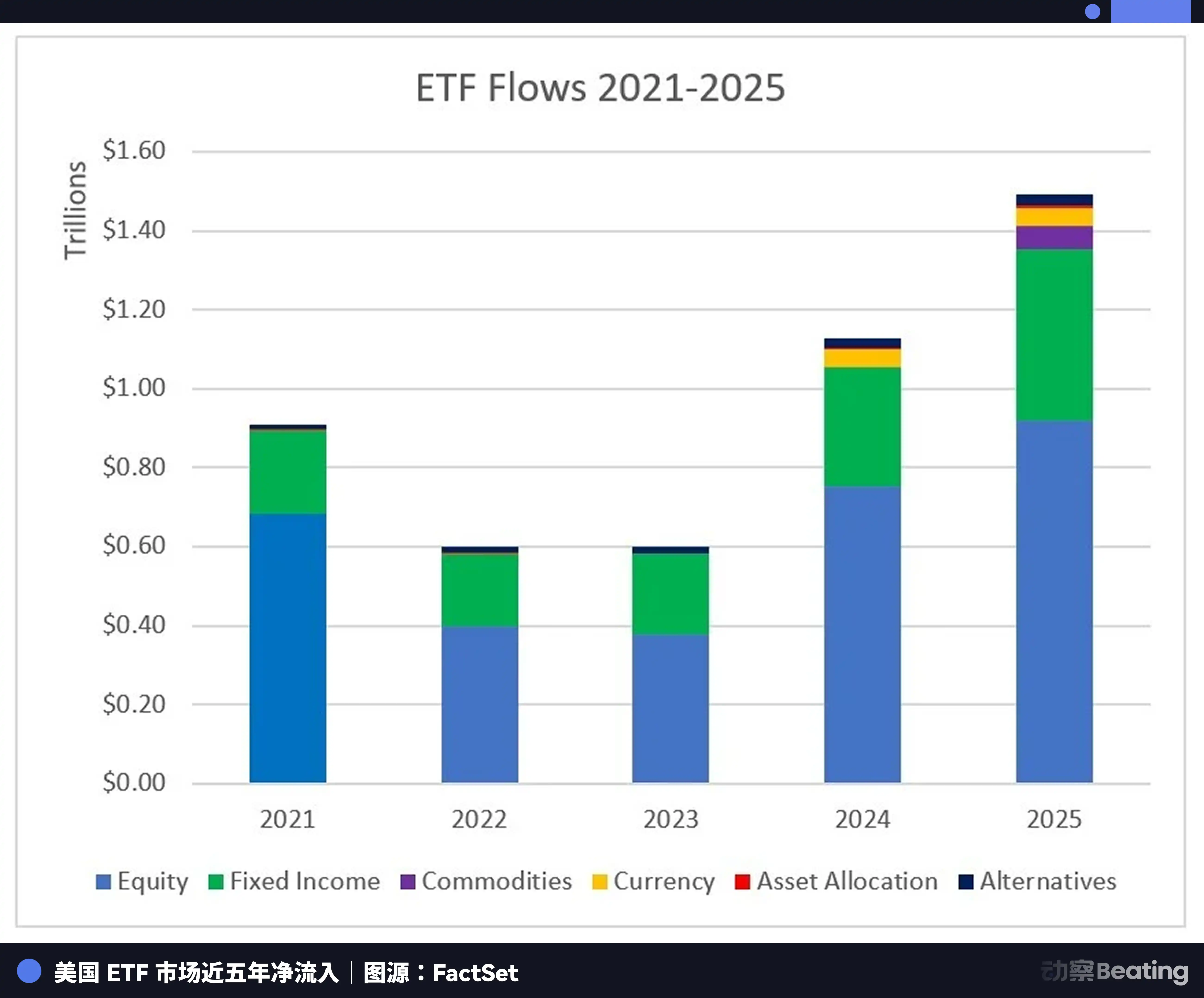

In 1975, John Bogle created the first index fund for ordinary investors at Vanguard, tracking the S&P 500. Wall Street's reaction was ridicule; active stock picking was professional, passive following was a lazy strategy, and no one wanted to buy a mediocre product.

Half a century later, the lazy ones won.

As of March 2025, the assets under management of passive funds (including mutual funds and ETFs) in the United States reached $15.96 trillion, accounting for 51% of the total assets of the mutual fund industry, surpassing actively managed funds for the first time. In 2025, the US ETF market saw a record net inflow of $1.49 trillion, with equity ETFs attracting $923 billion.

There's a mechanical logic behind these numbers. Once a stock is included in an index, all funds tracking that index must allocate to it according to their weighting. There's no subjective judgment, no waiting for the right moment; it's mandatory buying. And as long as the company remains in the index, the funds hold it in perpetuity.

It's important to clarify that passive funds are price takers, not price setters. Stock price discovery is still primarily accomplished by active funds, involving analyst research, institutional trader speculation, and hedge fund betting.

But what passive funds do is equally crucial: they provide a huge, stable, and non-discretionary holding base. This base won't panic sell-offs because quarterly earnings reports fall short of expectations, nor will it cut positions because the CEO makes a tweet; it's the ballast.

For a company of SpaceX's caliber, the value of this ballast is quantifiable.

SpaceX's expected IPO valuation is approximately $1.75 trillion, which would place it directly among the top six in the Nasdaq 100. Under current rules, newly listed companies typically need to wait up to a year before being eligible for inclusion in major indices such as the S&P 500 or Nasdaq 100. This waiting period was originally intended to assess the company's ability to withstand the liquidity pressures brought about by large-scale institutional buying.

But for SpaceX, this waiting period means that funds tracking the Nasdaq 100, including Invesco QQQ which manages over $400 billion, will be unable to allocate to one of the world's top ten companies by market capitalization for up to a year, and the tracking error will become unacceptable.

The pressure isn't on SpaceX, it's on the index funds themselves.

Nasdaq therefore proposed the Fast Entry rule, which allows newly listed companies to be included in the market capitalization of existing constituent stocks after 15 trading days. This rule is still under review, but Nasdaq itself acknowledges that it was designed to attract high-valuation private companies such as SpaceX, Anthropic, and OpenAI.

SpaceX makes rapid inclusion a prerequisite for selecting exchanges, and it has the confidence to do so because the inherent requirements of the passive index system give it bargaining power.

Some might ask, if the core objective is to be included in an index, why not do a direct listing? Direct listing saves on underwriting fees, and you can still be listed and included in an index.

The answer lies in scale.

SpaceX's IPO is expected to raise over $25 billion, and it needs to create a sufficiently large free float on its first day of trading to meet the liquidity threshold for passive fund allocation. Direct listings do not involve new share issuance; the number of shares available on the first day depends entirely on how much existing shareholders are willing to sell. For a company with a market capitalization of $1.75 trillion, if the free float is too small on the first day, passive funds simply cannot complete their position building, causing drastic price distortions.

Structured IPOs are precisely the tools that pave the way for large-scale passive investment. This logic, in turn, explains why Revolut and Stripe aren't in a hurry.

Revolut's $75 billion investment in the Nasdaq 100 has limited weighting, and the resulting passive buying is disproportionate. Furthermore, its delay has other practical reasons, such as the ongoing process of obtaining a banking license, and management's desire for several more quarters of earnings data to solidify the valuation narrative.

However, the arithmetic of index weighting is also part of the calculation. Stripe's valuation of $159 billion is already considerable, but John Collison said that an IPO is not a priority. The underlying judgment may be similar: the structural benefits of an IPO can only be maximized when the valuation grows further and the weighting in the index becomes more meaningful.

The value equation for going public is being rewritten.

Fundraising has taken a backseat; employee liquidity and VC exits are the fundamentals. Meanwhile, the perpetual holding base provided by index investing is becoming a new variable in determining the timing of an IPO. It's not the only variable, but its weight has been steadily increasing over the past decade, and in the case of SpaceX, it was brought to the negotiating table for the first time.

So, what is the role of the exchange in this game?

Surprise attack by Hyperliquid

Nasdaq has changed its index inclusion rules for a company that is not yet publicly listed.

In October 2025, ICE, the parent company of the NYSE, invested $2 billion in the prediction market platform Polymarket, valuing the company at approximately $8 billion. In March 2026, ICE further invested in the cryptocurrency exchange OKX at a valuation of $25 billion, gaining a seat on its board of directors.

These two things, on the surface, are competitive strategies, but at their core, they reflect the same anxiety: the scarcity of gatekeepers is disappearing.

There used to be an unwritten boundary between the NYSE and Nasdaq. Traditional industries went to the NYSE, while technology and emerging industries went to Nasdaq. This boundary lasted for decades, with both sides maintaining a monopoly in their respective fields.

That tacit understanding has now broken down.

The structure of ICE's investment in OKX warrants close examination. OKX's 120 million users will gain access to ICE's US futures market and tokenized trading of NYSE-listed stocks. In return, ICE will receive OKX's real-time cryptocurrency pricing data for developing regulated crypto futures products.

ICE Vice President Michael Blaugrund put it bluntly: ICE's future competitors may not necessarily be traditional institutions like CME or Nasdaq, but rather DeFi protocols or super apps. He specifically named Robinhood and Uniswap.

A company listed on the NYSE publicly acknowledging that its future competitor might be a decentralized protocol is itself a signal.

Polymarket's investment logic is similar. ICE isn't buying a prediction market platform, but rather an entry point into on-chain trading infrastructure. The partnership includes institutional distribution of Polymarket data and future tokenization projects.

In the 1990s, Nasdaq broke the NYSE's floor trading monopoly with electronic trading. The power shifted, but the格局 (geju, a term referring to the overall structure or pattern) didn't disappear. Today, on-chain infrastructure is replaying this scenario, eroding the market share of derivatives and alternative assets on the fringes of exchanges.

Hyperliquid provides the most specific cross-section.

This decentralized exchange achieved a total trading volume of $2.95 trillion in 2025, with an average daily trading volume of approximately $8.34 billion and annual revenue of $844 million. It also added over 600,000 new users. For comparison, Coinbase's trading volume during the same period was approximately $1.4 trillion. This on-chain protocol, without a corporate entity or publicly visible CEO, achieved twice the trading volume of Nasdaq-listed Coinbase.

What deserves even more attention is the change in its user structure.

In 2025, Hyperliquid launched on-chain perpetual contract trading for global stocks such as the S&P 500, Nasdaq, gold, crude oil, Nvidia, and Tesla through the HIP-3 protocol. On its tokenized platform, trade.xyz, crypto trading pairs accounted for only 7 of the top 30 markets by trading volume. On March 15th, the total open interest in the HIP-3 market reached a record high of $1.43 billion, a 100-fold increase in six months, with trade.xyz capturing 90% of that.

In March, escalating tensions in the Middle East triggered sharp fluctuations in oil prices. Traditional futures exchanges closed for the weekend, leading to a surge of professional traders flocking to Hyperliquid. These weren't retail investors; they were professional futures traders drawn by the 24/7 availability, on-chain transparency, and higher capital efficiency. While traditional exchanges were still opening and closing their markets according to schedule, the on-chain market had already turned "24/7 liquidity" from a concept into reality.

These figures and the exchanges' current IPO business are not on the same track, and direct competition between the two is very limited. But ICE's concern is not about today, but about the trend.

When on-chain infrastructure can support perpetual contract trading of global stocks, when professional traders begin to use on-chain tools for hedging and speculation, and when the liquidity of tokenized stocks gradually approaches that of traditional exchanges, the moat of exchanges is being bypassed little by little.

The NYSE chose to invest in blockchain players, while Nasdaq chose to modify its own rules. Both actions point to the same conclusion: the era of maintaining a dominant position through monopolies is over, and proactive expansion is the only option.

end

In 1971, no one saw Nasdaq's electronic quotation terminals as a threat. In 2006, no one thought the NYSE would voluntarily dismantle its trading floor. In 2026, no one knows how far Hyperliquid and the on-chain infrastructure it represents will go.

But after each concession to the rules, the old structure did not disappear, but was re-stratified.

The NYSE still exists and remains powerful, but it no longer holds exclusive pricing power. Nasdaq will become even stronger after SpaceX's IPO, and the foundation of its perpetual holdings will continue to grow as its market capitalization expands. ICE's investment logic in OKX and Polymarket is similar: if on-chain transactions are inevitable, then become the infrastructure provider for the on-chain world, rather than waiting to be bypassed.

The system on the blockchain will not disappear; in fact, it will become stronger and stronger, becoming a new infrastructure.

In a world where two systems coexist, where will the next large enough company with the confidence to offer competitive terms knock on doors? Or to put it another way, will it even need to knock on doors at all?

No Comments