Author:BitPush

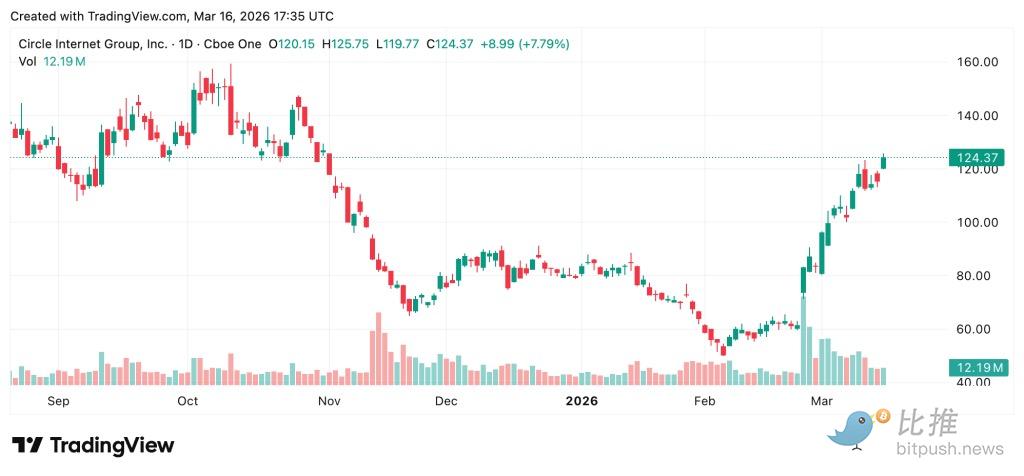

Since February,CircleInternet Groupshare priceCircle's price surged from around $50 to $125, more than doubling in a month. During the same period, Bitcoin retreated from its highs, and crypto stocks like Coinbase followed suit, with Wall Street's cautious sentiment towards tech stocks remaining strong. Circle's performance, however, was remarkably unique.

With a monthly increase of over 100%, Circle has not only far surpassed the S&P 500 and Nasdaq 100, but has also become the most watched name in the fintech field.

Even Ed Engel, an analyst at Compass Point who was previously the most ardent bear, upgraded his rating from "sell" to "neutral" in January of this year. Seaport Global, on the other hand, has given a target price as high as $280, making it the most optimistic voice in the market.

Financial Report: A Remarkable Turnaround

It all started with a financial report released at the end of February.

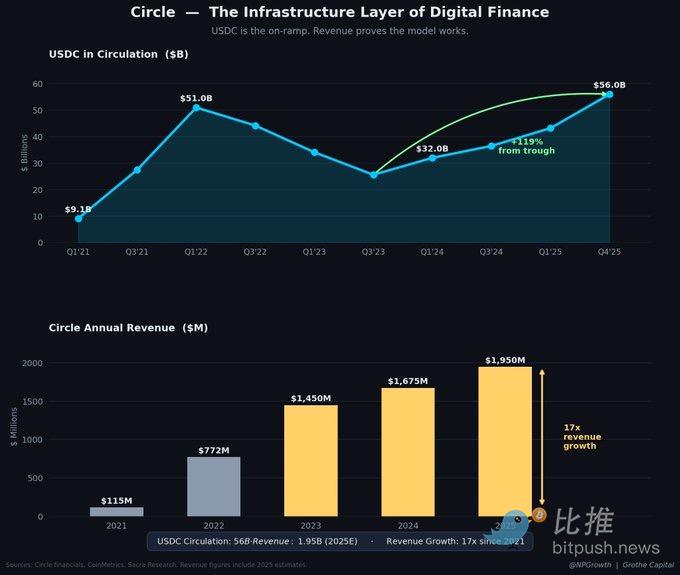

Circle's total revenue and reserves reached $2.75 billion in 2025, a year-over-year increase of 64%. What truly surprised the market was the fourth quarter: single-quarter revenue of $770 million, a year-over-year increase of 77%, and adjusted EBITDA of $167 million, a staggering increase of 412%.

The "net loss of $70 million" that Wall Street had previously worried about was actually an accounting issue. This loss primarily stemmed from a one-time stock compensation expense of $424 million following the IPO. Excluding these non-cash items, Circle's cash flow is actually quite robust. Mizuho Bank stated in a research report that Circle is demonstrating strong operating leverage—revenue growth is far outpacing cost expansion.

This prompted Ed Engel, an analyst at Compass Point and Circle's most staunch short seller, to "surrender" in January of this year, upgrading his rating directly from "sell" to "neutral".

Core Logic Restructuring: Not a Crypto Company

Circle CEO Jeremy Allaire has recently emphasized on multiple occasions that they are not a “crypto company.”

That makes sense. Unlike exchanges that rely on transaction commissions for profit, Circle's model is more like a combination of a "light-asset bank" and a "payment network." It issues...USDCStablecoinsIt is backed by 100% US dollar and US Treasury bond reserves. In other words, Circle earns a large portion of its profits from US Treasury bond interest.

Circle has actually benefited from concerns about "sticky inflation" in the macroeconomic environment. The escalating situation in Iran and rising oil prices have repeatedly delayed expectations of a Federal Reserve interest rate cut.

Interest rate spread advantage: In its Q4 financial report, interest income from US Treasury bonds contributed 95% of its total revenue (approximately $733 million). As long as high interest rates persist, Circle enjoys a huge interest rate spread that is almost "risk-free".

Safe-haven effect: Even as the overall crypto market declines, USDC's market capitalization has shown remarkable resilience. Clear Street data shows that since October 2025, the crypto market capitalization has fallen by 44%, but USDC's market capitalization has remained rock-solid, reflecting its nature as a payment infrastructure rather than a speculative asset.

Bernstein analysts point out that this model gives Circle a certain "counter-cyclical" property. Even during crypto market downturns, as long as the circulating supply of USDC doesn't decrease, the company's revenue won't be significantly impacted. And data from the past few months shows that USDC's market capitalization has indeed demonstrated strong resilience.

Three growth engines: tokenization, prediction markets, and AI payments

Seaport Global analysts gave a high target price of $280 because the market underestimated USDC's "dominance" in three explosive growth areas.

The first is tokenized assets. From $1.5 billion in 2023 to $26.5 billion now, this market has increased 17-fold. BlackRock's tokenized government bond fund, BUIDL, with over $2 billion in assets, has seen significant growth in subscriptions and redemptions.depthIt relies on USDC. In this space, USDC is becoming the interface connecting physical assets and the on-chain world.

Robert Mitchnick, Head of Digital Assets at BlackRock, mentioned at an industry conference that institutional clients' demand for on-chain government bonds has exceeded expectations, with USDC playing a crucial settlement role. Traditional cross-border fund flows take 2-3 business days; with USDC, this process is compressed to minutes. For institutional transactions often involving tens of millions of dollars, this efficiency improvement represents a qualitative leap.

The second is the prediction market. Platforms like Polymarket processed over $22 billion in transactions in 2025, with USDC as the sole settlement currency. This market is characterized by event-driven fluctuations—US elections, sporting events, and the release of macroeconomic data all trigger pulses in trading volume. Each of these pulses reinforces USDC's position as "internet casino chips."

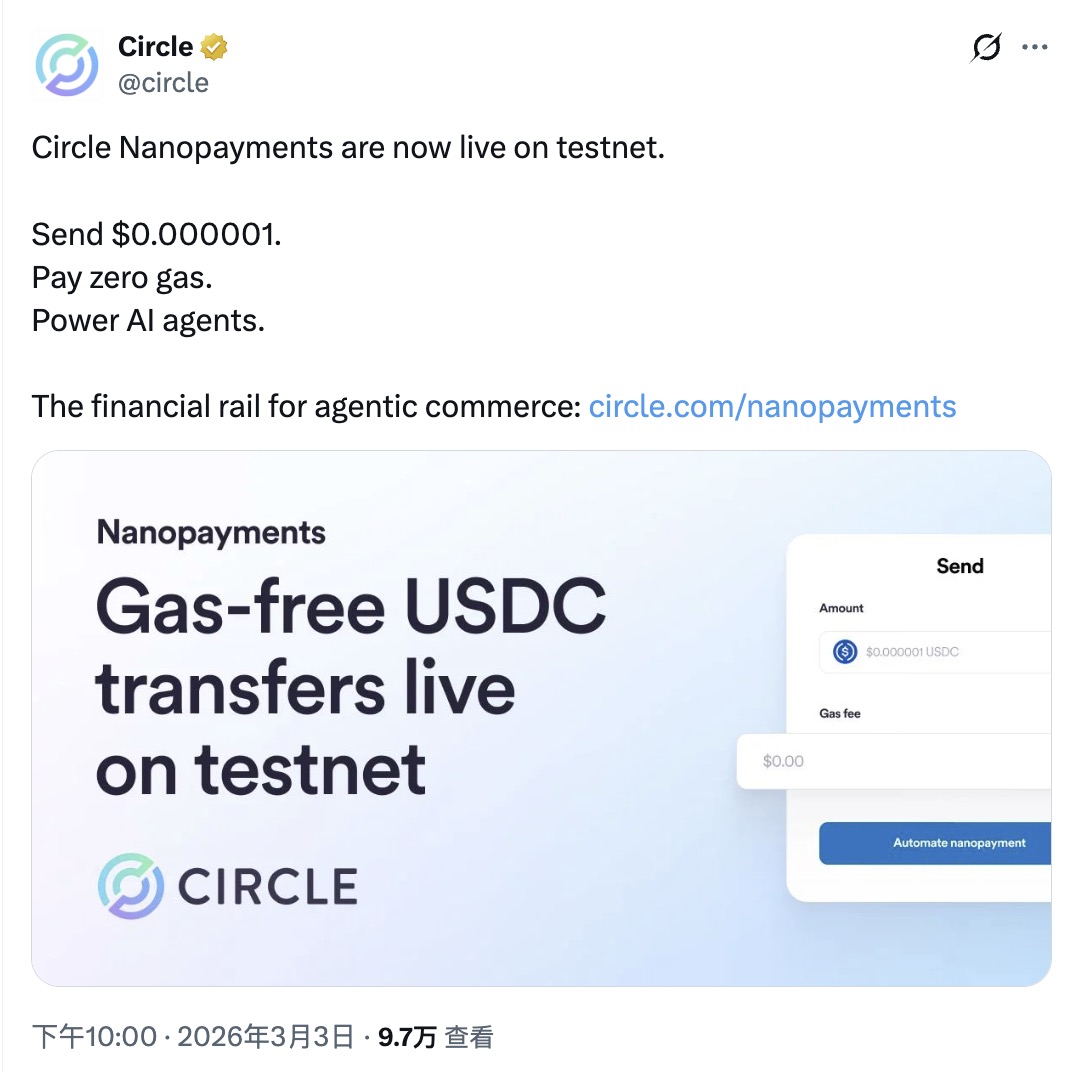

The third is AI agents. This is probably the direction with the greatest potential.

Autonomous AI software requires a programmable payment tool to facilitate machine-to-machine transactions. For example, if one AI needs to call upon the services of another AI or purchase computing resources, it must be able to automatically complete small payments. Traditional credit card networks cannot handle such microtransactions, while on-chain settlement via stablecoins perfectly meets this need.

Early data shows that approximately 98% of AI agent payments are now settled in USDC. In the past nine months, AI agents have completed over 140 million payments, totaling $43 million. While the absolute amount is still small, the growth rate of transactions is astonishing. Analysts at Clear Street say the market may be underestimating the potential impact of AI on USDC. "If billions of AI agents emerge in the future, every transaction between them will require a common currency. USDC is currently the closest player to that role."

Circle clearly saw this opportunity. In mid-March, the company launched the Nanopayments testnet, supporting gas-free transfers as low as $0.000001. This product is designed entirely for micro-transactions between machines, aiming to capitalize on the upcoming AI agent economy.

Regulatory benefits and compliance premium

The regulatory environment is also changing.

The Trump administration showed some support for digital assets, and the advancement of the Clarity Act has gradually clarified the regulatory framework for stablecoins. The core of this act is to address two key questions: what licenses stablecoin issuers need, and what standards reserve assets must meet. Once the act is passed, the last barrier for traditional financial institutions to enter this market will be removed.

As the most compliant issuer, Circle is enjoying its "compliance premium." Its audits are far more stringent than its competitors', its reserve reports are published monthly, and its reserve assets consist entirely of short-term U.S. Treasury bonds and cash. This transparency is a cost when regulations are lax, but it becomes a moat when regulations tighten.

This shift in mindset is driving USDC's penetration rate among institutional funds. Over the past six months, USDC's circulating supply has increased by approximately 30%, while Tether's has remained largely unchanged. Behind this shift lies the continuous inflow of institutional funds.

summary

Of course, risks still exist.

Circle is highly sensitive to interest rates. It has calculated that for every 100 basis point cut in interest rates by the Federal Reserve, its annualized interest income decreases by approximately $618 million. If interest rates decline rapidly over the next two years, the company's profitability will be significantly impacted.

The valuation isn't cheap either. Its current price-to-book ratio is 9.2, far exceeding the levels of traditional financial companies. The price-to-book ratios of US bank stocks are generally between 1 and 2, and even for payment companies with better growth potential, Visa and Mastercard's price-to-book ratios are only 6 to 7. Circle's current valuation has already factored in much of the optimistic expectations.

There's also competition. Tether is pushing forward with new regulated products, PayPal has launched its own stablecoin, and JPMorgan Chase has its own on-chain deposit token. These giants each have their own advantages, and whether USDC can maintain its market share remains to be seen.

But one thing is becoming clear: the stock price surge over the past month is essentially a reassessment of Circle by Wall Street.

This proves one thing: when blockchain technology sheds its speculative nature and becomes a payment infrastructure tied to US Treasury reserves, compliance systems, and the AI ecosystem, it will no longer belong solely to the "crypto circle" but may become part of global finance. This question is more important than the rise and fall of the crypto market: can USDC replace the outdated and slow SWIFT system in the next decade?

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG discussion group:https://t.me/BitPushCommunity

Bitpush TG Subscription:https://t.me/bitpush

Note: All articles on Bitpush represent the author's views only and do not constitute investment advice.

CircleUSDCdepthStablecoinsshare priceOpinion

Related News

A 10,000-word analysis of Canton Network: Wall Street's blockchain ambitions

$50 million gone in a single "confirm"! The most expensive accidental loss in DeFi history is born.

Don't rush to predict the demise of cryptocurrencies; AI is revitalizing them.

The downfall of crypto had little to do with exploiting investors.

No Comments