Author:Cold Wind Meta

source:BitMEX ResearchCompiled by: Jinse Finance

Key points of this article

We analyzed Stretch ($STRC), a novel MSTR (Strategy) debt instrument designed to maintain price stability by adjusting its dividend yield monthly based on bond market prices. Therefore, it is marketed as a low-risk product and compared to short-term U.S. Treasury bonds. This is yet another attempt by Mr. Michael Saylor to infiltrate the financial system, again with the aim of accumulating more Bitcoin. We reviewed the SEC filings, and as we understand them, MSTRs can abandon their price stability objective, reducing the dividend by up to 25 basis points per month, meaning the dividend yield could potentially drop to zero within a little over three years. Therefore, we believe this product is favorable for MSTRs, and from an investment perspective, its risk is significantly higher than that of short-term Treasury bonds.

Overview

In November 2024, we published an article about MSTR, titled "We calculated the mathematical principles of a Ponzi scheme.".

This approach is relatively simple, focusing solely on the stock itself. In addition to stocks, MSTR offers a range of other financial products for investors to choose from. Of particular note is the company's relatively new line of senior perpetual bonds:

This article will focus on what we consider the most interesting of the four products—STRC. In particular, following our article published in November 2024,STRC is the product for which we receive the most questions..For example:What happens when the music stops and the influx of new funds into MSTR runs out? How will MSTR pay STRC's dividends then? Will MSTR be forced to sell Bitcoin? Is STRC a Ponzi scheme?In light of these issues, we decided to write this short article to outline our basic views on SRC.

What is STRC?

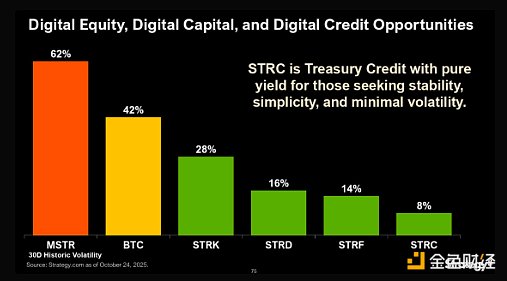

STRC is touted as the lowest-risk offering in the MSTR investment portfolio. In fact, its risk is comparable to US Treasury bonds or stablecoins. However, its returns are significantly higher than these low-risk alternatives. The chart below, from a recent MSTR investor presentation, compares STRC to "Treasury credit."

source:Strategy file

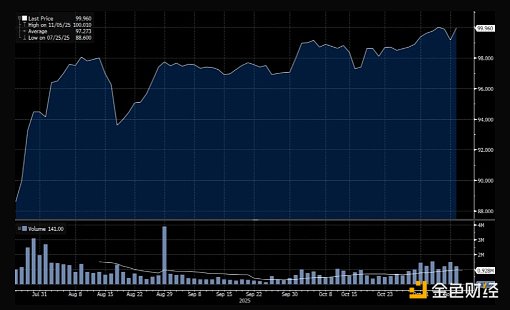

The price of STRC has recently risen to its face value of $100. This indicates that it has achieved some success and its price has remained relatively stable.

How are interest rates determined?

STRC's target appears to be maintaining a trading price around $100. Dividends are typically paid monthly, with the company able to adjust the amount at its discretion. The idea is that if STRC's trading price is below $100, dividend payments can be increased, thereby pushing up MSTR's price. Conversely, if STRC's trading price is above $100, dividends can be reduced, which theoretically should bring the price back down to around $100.Therefore, this instrument should be very stable, consistently trading around $100. This makes STRC a cash-like instrument and an alternative investment to short-term Treasury bonds. A key difference from Treasury bonds is that the funds raised from issuing STRC are used to purchase Bitcoin. This is yet another attempt to infiltrate the financial system with the aim of buying more Bitcoin.

As far as we know,STRC is a completely new product. There are currently no other similar debt instruments on the market.Debt instruments typically offer fixed or floating coupons, and their interest rates fluctuate based on other interest rates in the economy, such as the federal funds rate. We have not yet observed any other debt instrument that maintains market price stability by adjusting interest rates. MSTR, seemingly emboldened by its previous success in exploiting a loophole in the financial system—selling its own stock at a premium to buy Bitcoin—has devised an even more audacious scheme: issuing bonds to purchase Bitcoin. Due to this novel approach, these bonds appear to carry the same risks as short-term Treasury bonds.

At first glance, this new debt issuance model seems unsustainable for companies. If a company uses a fixed-coupon bond, its liabilities remain unchanged even if it faces difficulties. However, if a company uses a floating-coupon bond, the floating rate is designed to maintain debt price stability. Therefore, if the company faces difficulties and credit risk increases, it will need to increase coupon payments to maintain debt price stability. This means that as the company encounters difficulties, its liabilities will also increase. Thus, the company may fall into a vicious cycle, with its credit rating continuously declining until bankruptcy. Therefore, these new instruments may exacerbate corporate instability. For example, a drop in the price of Bitcoin could lead to a decrease in the value of STRC, which in turn increases the monthly payment liabilities of MSTR, ultimately leading to a vicious cycle.

What are the interest rate rules?

Given the above mechanism, it is worth noting the rules for setting monthly dividend payments, rather than simply the goal of stabilizing the STRC share price. Particular attention should be paid to the rules regarding coupon rate reductions. These rules are detailed below, but due to their somewhat obscure wording, they may be difficult to understand.

However, we may not reduce the annual monthly regular dividend rate applicable to any regular dividend period by: (i) (1) 25 basis points; and (2) (x) the sum of the lowest values of the annual monthly SOFR (as defined in the supplement to this prospectus) for the first business day of the preceding regular dividend period and (y) the annual monthly SOFR rates for each business day from the first to the last business day of the preceding regular dividend period (if any); or (ii) to a level lower than the annual monthly SOFR rate effective on the business day preceding the date on which we issue the next regular dividend rate notice.

source:SEC

Note: SOFR is the US market-based overnight interest rate benchmark. It was established to replace LIBOR because LIBOR was more easily manipulated by certain banks.

Our understanding of the above is that, regardless of other circumstances, the MSTR has the right to reduce its dividend yield by up to 25 basis points per month at its own discretion. The dividend yield can be reduced by 25 basis points per month, depending on the STRC's share price or overall market conditions. This equates to 300 basis points or 3 percentage points per year. Therefore, based on the current 10% dividend yield, it would take three years and four months to reduce the dividend yield to zero at the maximum allowed reduction. In some cases, if market interest rates in the overall economy are also declining, the company can reduce the dividend yield more quickly each month. For example, if the overnight market interest rate falls by 100 basis points in a month (from the beginning to the end), then the STRC's dividend yield could potentially decrease by 100 basis points + 25 basis points = 125 basis points in any given month. This seems reasonable; if the benchmark interest rate falls, then the STRC should be able to adjust accordingly.

If MSTR fails to pay its declared dividends, the consequences are complex. In this case, unpaid dividends will continue to accumulate. Our understanding is that MSTR cannot pay dividends on "any class or series of dividend par stocks" until all unpaid accrued dividends have been paid, unless it also pays STRC dividends, and the STRC dividends constitute at least a proportion of the accrued unpaid dividends that is not less than the same proportion of other dividend-paying stock classes. In other words, the higher the accrued unpaid dividends, the more difficult it becomes to pay significant dividends on other stock classes. Therefore, if MSTR begins to accumulate unpaid STRC dividends, it becomes more difficult to pay dividends on any other stock classes. However,There is currently no risk of any form of guarantee or bankruptcy, and the company is not obligated to pay dividends to STRC holders if it does not wish to do so.

Is STRC a Ponzi scheme?

Now that we understand how STRC works, we can explore whether it shares similarities with a Ponzi scheme. Of course, it's not a Ponzi scheme in the strictest sense, as it's not based on lies or fraud. However, if a model shares many similarities with a Ponzi scheme—for example, it can provide investors with seemingly generous and stable returns, but the maintenance of these returns depends on a continuous inflow of new funds, and once the inflow stops, the entire system collapses—then comparing it to a Ponzi scheme becomes reasonable.

From a cash flow perspective, STRC's costs are quite high. With an issuance size of approximately $3 billion, and a 10% yield, its annual dividend payout would reach $300 million. MSTR cannot afford such high dividends without raising new capital or selling Bitcoin, making STRC, in a sense, somewhat resemble a Ponzi scheme. However, considering that the company can completely and autonomously reduce its dividend payouts gradually to keep them within an affordable range, it doesn't actually resemble a Ponzi scheme. Therefore,In summary, we do not believe that STRC is a Ponzi scheme. However, we believe that investing in STRC at $100 does not demonstrate exceptional investment insight. In our view, STRC carries significantly higher risk than short-term U.S. Treasury bonds.

in conclusion

If the music stops abruptly, MSTR faces challenges. Instead of dumping Bitcoin, MSTR could completely abandon its strategy of aiming for stability with STRC. The company can choose any easier option. MSTR could reduce the dividend yield of STRC by 25 basis points per month. At the current dividend yield of 10.5%, it would take three and a half years to reach zero. As the dividend yield decreases, the cost of paying dividends will also decrease. We believe this is very beneficial for MSTR, and therefore the current dividend payments are sustainable and affordable. Of course,This means that the price of STRC could plummet, potentially by as much as 87%.Until the present value of cash flows over the next three and a half years.

The story of MSTR may not be what some skeptics expect. We believe that...MSTR's debts may not necessarily lead to a forced sell-off of Bitcoin, triggering a price spiral that ultimately results in MSTR's bankruptcy.We need to understand that Strategy's debt instruments are highly innovative; they are not ordinary debt instruments, but rather specially designed to meet its own needs.Saylor is no ordinary person! He is a prodigy of our time.They often use unusual mechanisms (whether debt or equity) to raise billions of dollars for their companies.MSTR will not be affected regardless of Bitcoin prices or fund flows.Conversely, investors may feel dissatisfied when everything comes to an abrupt halt. We believe that STRC is a perfect example of this phenomenon.

No Comments