Author:Currency Explorer

The U.S. released its non-farm payrolls report on Friday, showing that the country added 178,000 jobs, far exceeding expectations. Meanwhile, the February figure was revised down from an initial estimate of a decrease of 92,000 to a decrease of 133,000. The unemployment rate fell from 4.4% to 4.3%. This report provided short-term support for the dollar against the backdrop of a reduced probability of a Federal Reserve rate cut in 2026.

Gold prices are currently under pressure due to the Middle East conflict and market expectations that central banks will raise interest rates to combat inflation caused by soaring oil prices. Another factor unfavorable to international spot gold is declining demand for gold and some countries selling off their gold reserves to support their currencies, as seen recently by India and Turkey. Other countries may also be taking similar actions, though these have not yet been disclosed. This week, hawkish comments from Trump led to a further decline in gold prices, but did not trigger a new round of large-scale selling.

The impact of the war with Iran on oil supplies and energy prices remains a key focus for investors, particularly the situation in the Strait of Hormuz. US WTI crude oil prices broke through $110 a barrel on Thursday, rising about 90% since the beginning of the year, while the average US gasoline price rose above $4 a gallon for the first time in more than three years this week.

Next week's release of the U.S. Consumer Price Index (CPI) will be a preliminary litmus test for the impact of the energy shock triggered by the war. A surprising surge in the data could trigger a negative market reaction.

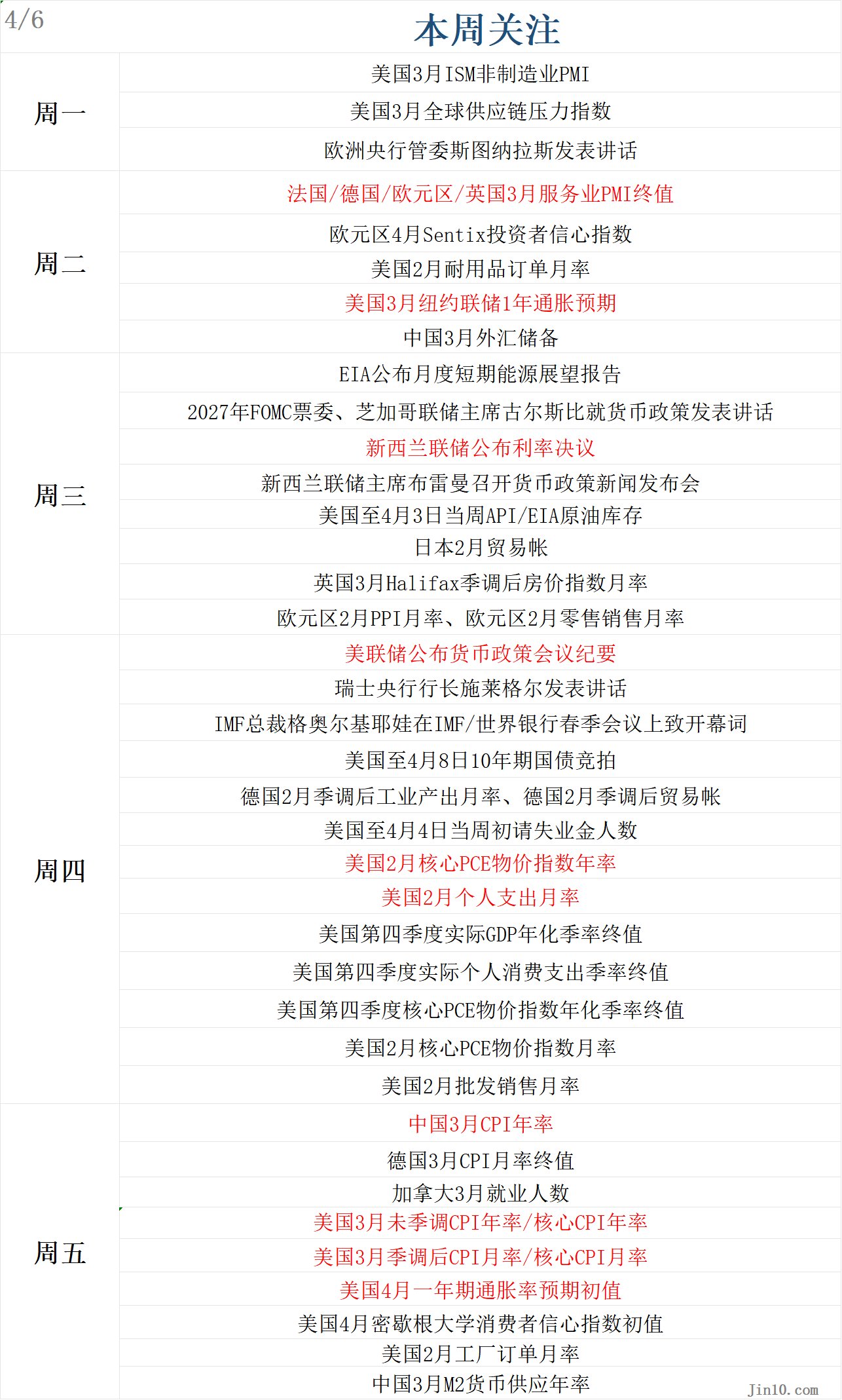

Here are the key points the market will be focusing on in the new week (all times are Beijing time):

Key Event: Sixth week of the Iran war, Trump's script has collapsed, and the bigger drama for gold prices is yet to come.

The war has entered its sixth week, and the prospects for peace negotiations are bleak.

Over the weekend, the United States continued its search for a crew member from the F-15E fighter jet shot down by Iran on Friday, while Tehran continued its attacks on Gulf Arab states and Israel. A second U.S. combat aircraft reportedly crashed in the Persian Gulf on the same day.

These incidents demonstrate that despite Trump and Hergé's claims that the U.S. military has complete control of the skies, U.S. and Israeli aircraft still face risks over Iran.

The Wall Street Journal reported on Friday thatIran has told mediators it is not prepared to meet with U.S. officials in Islamabad in the coming days, and Pakistan-led ceasefire efforts have stalled.

As hostilities continued on Saturday, Iranian state media reported that an airstrike hit a petrochemical zone in southwestern Iran. A projectile also struck an auxiliary building near Iran's Bushehr nuclear power plant. A warehouse storing bottled water in western Iran was also targeted by airstrikes.

Iran attacked a power and water plant in Kuwait on Friday after Trump threatened to strike bridges and power plants in Iran, highlighting the vulnerability of Gulf states that heavily rely on desalination plants for drinking water.

The Wall Street Journal reported thatIran's downing of two U.S. warplanes is the most compelling evidence to date that, despite suffering significant military losses, Tehran can still substantially increase the cost of continued conflict between the U.S. and Israel.These downings represent the most successful demonstration of Iran's military strategy, aimed at inflicting tactical defeats on the United States and its allies. The goal is not military victory, but rather survival and weakening their will to continue fighting.

The question is, to what extent do such blows undermine Trump’s resolve to continue or even expand the war, given that he seems determined to end it quickly?

“This undoubtedly shows that Iran can win without winning,"said Alan Eyre, a former State Department expert on Iran and a researcher at the Middle East Institute. “The US narrative is, ‘We’ve got everything in our pockets.’ This breaks that narrative.”

William Wechsler, a former Department of Defense official who heads the Middle East program at the Atlantic Council, said...Even with a significant advantage for the U.S. military, the war could quickly spiral out of control.He said, "The war will continue for some time, and whether intentional or unintentional, the possibility of further escalation is increasing. No one should be confused—"There are many ways this war could escalate rapidly.”

Trump has ordered the 82nd Airborne Division to send thousands of Marines and soldiers to the Middle East. While he has not indicated that he plans to order a ground attack on Iranian islands in the Persian Gulf, these deployments provide him with the option to carry out such an attack and have already triggered preparations from Iran and a new wave of threats.

Eyre said, "If an Iranian attack results in a large number of Americans being captured by Iranians, or a large number of Americans being put into body bags, it will change his calculations about continuing the war."

According to a Reuters report citing three sources, a recent U.S. intelligence report warned that...Iran is unlikely to open the Strait of Hormuz in the short term.

FxPro's chief market analyst, Alex Kuptsikevich, stated, "Trump's promise to return Iran to the Stone Age stands in stark contrast to his previous statements about ending the conflict within 2-3 weeks under successful negotiations. Polymarket participants estimate a 65% chance of the war between the US and Iran ending by the end of June. Closing the Strait of Hormuz before then would be a real catastrophe for the global economy."

This uncertainty will continue to put downward pressure on gold prices.Kuptsikevich stated, "The Middle East conflict is depressing gold prices as people expect central banks to raise interest rates to combat rising oil-driven inflation. This is a rather short-sighted approach, as current fuel prices are a shock to consumers, which in turn impacts the economy, demanding monetary policy easing, not tightening. However, we first need to hear central banks agree on this point; currently, they remain focused on inflation."In our medium-term price target, our target is the 4200 level.A drop in gold prices to this level would not break the upward trend. A break below this level would signal a reversal in the three-year gold price trend. A rebound from this level would give people hope that the bullish trend in gold is not yet over.

Kuptsikevich stated that spot gold is highly likely to retest the 50-day moving average near $5,000 next week and eventually escape oversold territory. This suggests an optimistic outlook for next week, but we remain cautiously pessimistic about the long-term trend, expecting a medium-term decline to $4,200, within the current downtrend.The low point could reach $3,300..

Darin Newsom, senior market analyst at Barchart.com, said: "Gold prices will consolidate between the high of 5666.60 and the low of 4128.50."A fluctuation range of $1,500Does this mean I have no clue? Absolutely.It all depends on what the US president posts on social media next..

Kitco senior analyst Jim Wyckoff noted, "Technically, the next upside price target for April gold futures bulls is a close above the solid resistance level of $5,000. The next near-term downside price target for bears is to push futures prices below the solid technical support level of $4,300. The first resistance level is $4,700, followed by $4,750. The first support level is $4,600, followed by $4,580.40."

FXTM senior market analyst Lukman Otunuga said he will be watching the initial support level of $4,600 per ounce. "Looking at the charts, a daily close holding below $4,600 could encourage a move towards $4,450. If $4,600 provides reliable support, prices could rebound to $4,800."

A research report from CICC suggests that the US-Iran conflict led to a surge in oil prices, creating a pre-existing risk of inflation. Market expectations of a shift in the Federal Reserve's interest rate cut path have put selling pressure on gold ETFs that saw significant increases in holdings last year. Simultaneously, liquidity shocks have fueled a short-term correction through the futures and options markets. The current geopolitical situation in the Middle East may be reaching a critical juncture, with oil prices facing a crucial decision point. The gold market's pricing focus may shift to assessing the impact of supply shocks on stagnation, and the already priced-in interest rate hike expectations may need to be revised.

Looking ahead, CICC believes that regardless of whether it's the oil price correction following the geopolitical de-escalation, the return of monetary policy to an easing direction, or the increased pressure of recession due to supply shocks triggering the manifestation of gold's safe-haven value,Both gold investment demand and prices may have room for upward correction..

Central Bank Updates:The Fed meeting minutes are coming! The market's biggest fear is a shift in hawkish sentiment.

Fed:

WednesdayAt 00:35, Goolsby, a 2027 FOMC voting member and president of the Chicago Federal Reserve, will speak on monetary policy.

The Federal Reserve will release the minutes of its monetary policy meeting at 02:00 on Thursday.

Other central banks:

The Reserve Bank of New Zealand will announce its interest rate decision at 10:00 AM on Wednesday.

At 11:00 AM on Wednesday, Reserve Bank of New Zealand Governor Brehman will hold a press conference on monetary policy.

Thursday 16:00,Swiss National Bank President Schlegel delivers a speech

Thursday 18:45,European Central Bank Governing Council member Sleipön delivered a speech.European Central Bank Vice President Guindos will deliver a speech at 18:00 on Friday.

Bond traders closed the week betting that the Federal Reserve would keep interest rates unchanged this year, citing signs of stabilization in the U.S. labor market and uncertainty about the economic impact of the Middle East wars.

Thomas Simons, chief U.S. economist at Jefferies, wrote that the March report, showing the largest increase in nonfarm payrolls since the end of 2024, is unlikely to have a significant impact on U.S. policymakers. “These figures are largely retrospective and may not account for any recent energy price increases or other risks related to the war with Iran. Currently, there is no indication that they need to act quickly.”

Early Thursday morning, the Federal Reserve will release the minutes of its March monetary policy meeting. The revised Summary of Economic Projections (SEP) released at that time showed that policymakers' median forecast pointed to a 25 basis point rate cut in 2026. Although its timeliness is limited,However, these meeting minutes may confirm the hawkish shift reflected in the dot plot..

If the minutes of the meeting show that Federal Reserve officials are open to tightening policy due to rising inflation caused by the protracted conflict in the Middle East, spot gold may face renewed selling pressure. Conversely, if policy discussions focus more on supporting the labor market, gold prices may rise slightly.

Huatai Securities believes that the better-than-expected rebound in March's non-farm payrolls data demonstrates the resilience of the US job market. However, amidst the Middle East conflict, the impact of high oil prices on inflation expectations is more crucial for the Federal Reserve's monetary policy. The recent escalation of the Middle East conflict and the resulting supply gap caused by the blockade of the Strait of Hormuz have pushed up oil prices and inflation expectations. Inflation is currently the core variable in the Fed's monetary policy. The Fed's dual mandate of employment and inflation provides it with some room to maneuver, avoiding interest rate hikes to combat inflation. Furthermore, with rising inflation expectations, even if the Fed does not raise interest rates, the US Treasury yield curve may shift upwards.Forming a substantial contraction.

"The latest jobs report shows that the economy is creating enough jobs to keep pace with population growth, which is why the unemployment rate remains at a historic low of 4.3%," said Sonu Varghese, chief macro strategist at Carson Group, on Friday. "This will complicate things for the Federal Reserve, as it makes no sense to consider cutting interest rates, especially given the severity of the impending inflation shock. Inflation was already a problem before the recent crisis, and it ultimately appears that last year's rate cuts were a mistake."

Important data: The first CPI report since the start of the war is about to be released!

At 22:00 on Monday, the US March ISM Non-Manufacturing PMI will be released.

Tuesday, 15:50-16:30, final March services PMI readings for France, Germany, the Eurozone, and the UK.

Tuesday23:00US March New York Fed 1-year inflation expectations

At 17:00 on Wednesday, the Eurozone's February PPI month-on-month rate and Eurozone's February retail sales month-on-month rate will be released.

On Thursday at 8:30 PM, the following data will be released: US Initial Jobless Claims, US February Core PCE Price Index (YoY), US February Personal Spending (MoM), US Q4 Real GDP Annualized QoQ (Final), US Q4 Real Personal Consumption Expenditures (Final), US Q4 Core PCE Price Index (Final), and US February Core PCE Price Index (MoM).

At 20:30 on Friday, the US March unadjusted CPI year-on-year rate/core CPI year-on-year rate and the US March seasonally adjusted CPI month-on-month rate/core CPI month-on-month rate will be released.

Friday 22:00,US April one-year inflation expectations (preliminary), US April University of Michigan consumer sentiment index (preliminary), US February factory orders (month-on-month)

With the market digesting the US jobs data, next week's focus will primarily shift to the consumer sector, particularly Friday's CPI report and the University of Michigan consumer sentiment survey. These data, along with Monday's ISM Services PMI, the February Personal Consumption Expenditures report, and Tuesday's New York Fed one-year consumer inflation expectations, will reveal the initial impact of high energy prices and could trigger adjustments to Fed rate expectations, which are expected to largely remain at current levels.HawksSpeeches by Federal Reserve officials.

On Monday, the US will release its March ISM Services PMI report. Unless the index unexpectedly falls below 50, indicating contraction, it is unlikely to have a significant impact on gold valuations.

The U.S. Bureau of Labor Statistics will release March CPI data on Friday.This will be the first inflation data to reflect the impact of war..According to FactSet's consensus forecast, the year-on-year CPI increase is expected to jump from 2.4% to 3.1% based on overall data.

Wells Fargo believes the March CPI report will abruptly end the steady slowdown in inflation over the past two years, estimating a 1.0% month-over-month increase and pushing the year-over-year increase to 3.4%. The recent oil shock may dominate market sentiment regarding March inflation, "but we expect the detailed data to show that the moderate decline in core CPI was unsustainable." "We expect core CPI year-over-year growth to remain in the 2.7%–3.1% range for the remainder of the year."

According to the CME FedWatch tool, the market currently expects an approximately 83% probability that the Federal Reserve's policy rate will remain unchanged at 3.5%-3.75% until the end of 2026.Strong inflation data could lead market participants to reassess the likelihood of a Federal Reserve rate hike. Therefore, if monthly CPI data significantly exceeds expectations, it could boost the dollar and put downward pressure on spot gold.

The gold market was closed on Friday for the Easter long weekend, so the market did not react to the better-than-expected non-farm payrolls data.Some market analysts say gold prices are expected to come under pressure when Asian markets open on Monday.However, some analysts say that healthy labor market data will give the Federal Reserve some room to maintain a neutral monetary policy stance in response to growing inflation concerns.

Analysts say that for gold to regain its safe-haven appeal, investors need to see weak economic data, as this would trigger stagflation concerns and force central banks to cut interest rates to support the domestic economy, even if inflation remains high.

Chris Zaccarelli, chief investment officer at Northlight Asset Management, pointed out that most of the employment data was collected before the joint US-Israeli military strike against Iran. However, he added that this demonstrates a degree of economic resilience. "To some extent, this will make the Fed less likely to rush into cutting rates; however, it also reinforces the view that the labor market remains strong, which should allow consumer spending to continue to grow—a key factor for the economy."

Company Earnings Reports: US Stocks Rebound or a Trap? Now Might Not Be the Time to Trade

While the market may face further volatility in the short term, stock market investors appear hopeful that the sell-off is nearing its end. U.S. stocks staged a strong rebound this week, with the S&P 500 posting its best single-day performance since May on Tuesday, the final day of the quarter, followed by continued gains on Wednesday, the start of the new month. Ultimately, despite mixed trading on Thursday, the broader index still gained 3.4% over the week, which included holidays and shorter trading hours. Markets were closed on Friday, but the unexpectedly strong non-farm payrolls data released that day suggests that investors' recent optimism is justified.

The start of earnings season will also begin to attract Wall Street's attention, with investors generally expecting strong corporate earnings prospects, which will support the performance of the U.S. stock market this year.Companies such as Delta Air Lines (DAL.N) and beverage maker Constellation Brands (STZ.N) will release their earnings reports next week. These reports will provide an initial glimpse into the first quarter earnings season, which officially kicks off the following week. According to data from the London Stock Exchange Group (LSEG) IBES,The overall earnings of S&P 500 companies are expected to increase by 14.4% in the first quarter compared to the same period last year.

Deutsche Bank noted: "The first quarter earnings season, which began in mid-April, should indicate that corporate earnings growth is continuing to strengthen and expand further."

This two-day rebound was substantial, enough to convince bulls that the stock market is one step closer to shaking off the shadow of the Iran war, after investors have had time to digest the potential economic impact of rising oil prices. However, a significant number still warn that now is not the time to trade, believing that the market needs further consolidation before this chapter concludes.

“I just feel that this round of volatility is not over yet,” said Mark Malek, chief investment officer at Siebert Financial.

The duration of the war remains a major risk, which is why news headlines continue to dictate market direction. Investors are aware that inflation is rising—U.S. gasoline prices have surpassed $4 a gallon as ships are still unable to transit the Strait of Hormuz. But they also hold onto the hope that the end of the war will mean any price spikes will be temporary.

In a national address Wednesday night, Trump said the war was "very close" to ending. However, he also stated that the U.S. would first strike Tehran "extremely hard." Investors are assessing what Trump's plan means for restoring trade through the Strait of Hormuz.

Amidst numerous uncertainties, Marko Kolanovic, former chief market strategist at JPMorgan Chase, warned investors on Wednesday against going long ahead of the long holiday weekend, as the conflict could escalate during this period and the US might send ground troops to the Middle East. "I think some form of ground action is very likely to begin during this long weekend."All that noise and deception, I think, is just a ploy to prop up the market (stocks), suppress oil prices, and keep everyone complacent. It might be safer to downplay this rally.”

Over the past month, many on Wall Street have observed that although the Dow Jones Industrial Average and the Nasdaq Composite Index both fell into correction territory this week, and the S&P 500 is also nearing correction territory, this round of stock market sell-offs resembles an orderly adjustment rather than a violent collapse. Fundstrat technical strategist Mark Newton stated,He will wait until the market consolidates further between April 5th and 9th before buying, rather than trying to chase a short-term rebound.—Although he also predicted that the stock market had begun to bottom out.

Furthermore, Warren Buffett himself stated on Tuesday that the current share price is not cheap enough for him and he will not make a move. Malek of Siebert Financial bluntly stated:"Now is not the time to make a deal."

Max Gokhman, deputy chief information officer of Franklin Templeton Investment Solutions, said: “While assets fluctuate with every new headline, economic growth will face downward pressure and overall inflation will face upward pressure until a clear agreement is reached on a plan to reopen the Straits. This means indigestion for both equity and bond investors.”

Rushabh Amin of Allspring Global Investments believes the shock is transmitted through interest rates and the dollar, rather than directly impacting the stock market—and that repricing is what drives everything else. His strongest trade is going long on the dollar, which he sees as a contrarian trade.

David Lebovitz of JPMorgan Asset Management believes that an average oil price of $125 per barrel for the year will drag down economic growth by a full percentage point. His firm belief is that U.S. tech stocks are more immune to geopolitical interference than anything else. He is also shorting Europe.

Market Closure Arrangements:

1. Monday (April 6th), Easter Monday/Qingming Festival, the following markets will be closed:

- Deutsche Börse

- Australia-Sydney Stock Exchange

- France-Paris Stock Exchange

- Madrid Stock Exchange, Spain

- New Zealand - New Zealand Stock Exchange

- Milan Stock Exchange, Italy

- London Stock Exchange

- China-Taiwan Stock Exchange

- China-Hong Kong Stock Exchange

- China's Shanghai and Shenzhen Stock Exchanges, Beijing Stock Exchanges, and domestic futures exchanges

2. Tuesday (April 7) is a make-up holiday for Easter Monday. The Hong Kong Stock Exchange will be closed for one day, and northbound and southbound trading will be closed.

No Comments