作者:Wall Street CN

Since January 2023, driven by the demand for AI computing, memory chip stocks have continued to surge, with the average stock price of the top three memory manufacturers rising by 699%. However, as stock prices continue to climb, the market's biggest concern is no longer "how much higher can they go," but rather "what signals should we watch for to determine the turning point."

On March 16, UBS Global Research released a research report titled "Global I/O Memory Semiconductors," reviewing the cyclical patterns of the memory industry over the past 20 years and reassessing current leading indicators. UBS points out that driven by AI computing, the underlying logic of the memory industry has fundamentally changed, and traditional valuation and forecasting models may no longer be applicable.Operating profit, on the other hand, becomes a better leading indicator.

The industry's underlying logic has changed: AI is pushing supply and demand towards a new equilibrium.

UBS attributes the current market rally to "the shift in storage value in the AI computing power era." The report points out that two supply-side constraints are accumulating behind this value reassessment:

HBMs are taking up more and more DRAM wafer capacity, leading to a "severe DRAM shortage";

This tension is amplified by the "trade ratio": as the size of HBM DRAM die continues to increase relative to DDR, the "consumption" of production capacity per unit of HBM is higher.

Building on this, UBS draws a conclusion that is more relevant to investors—the central level of returns has shifted upward. The report states bluntly, "We believe ROE has undergone a structural reset," and projects that Samsung/SK Hynix/Micron will achieve an average ROE of 36% between 2026 and 2030E, significantly higher than the 15% of the past decade. This implies that using old cyclical templates to find the top may fail more frequently.

Traditional indicators fail: the "second derivative" is no longer reliable.

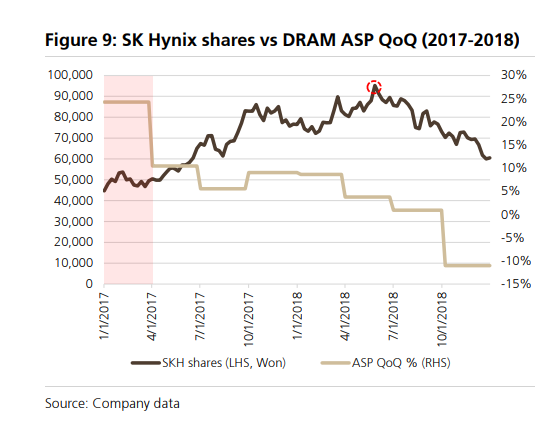

In the past, investors often used the "second derivative"—the quarter with the fastest quarter-on-quarter or year-on-year acceleration in storage contract prices (ASP)—to predict stock price peaks. However, UBS's review shows that the reliability of this indicator is declining.

In the past 20 years, in 10 instances of "stock price peaks", only in 50% of cases did the stock price and the DRAM ASP change peak in the same or similar quarter.

For example, in the fourth quarter of 2009 (the recovery period after the global financial crisis), the second quarter of 2013 (the cycle after industry consolidation), and the first quarter of 2017 (the traditional cycle), the peak of the sequential change in ASP occurred 3, 5, and 5 quarters earlier than the peak of stock prices, respectively.

UBS points out that although the actual ASP is slightly more synchronized with the stock price (peaking in the same quarter in 60% of cases), overall, the "second derivative" is no longer a reliable "top-selling" signal in the current complex market environment.

Finding a new anchor: Operating profit is a better leading indicator

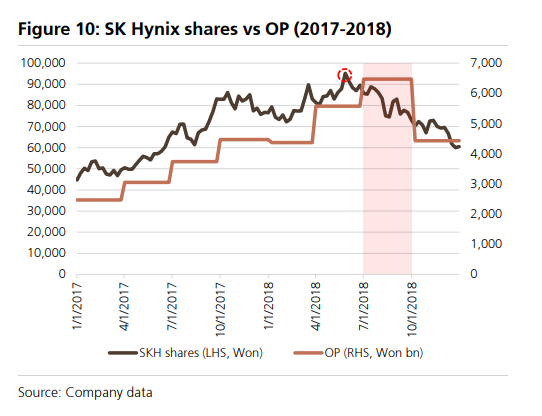

Since traditional indicators are failing, what should investors look at? UBS's answer is: operating profit (OP).

Operating profit not only reflects price changes but also incorporates factors such as bit growth and cost reduction per bit. Therefore, it is closer to the "final value" of the industry's true prosperity.

The report analysis shows that in the past 20 years, stock prices have peaked at the same time as or even earlier than operating profits in 90% of cases.

Especially before 2012, stock prices and operating profits peaked almost simultaneously. After that, the stock market became more predictive, and stock prices typically peaked one to two quarters earlier than operating profits (most often one quarter earlier).

However, UBS also cautioned investors that predicting when operating profits will peak is not easy. This is because the supply and demand changes brought about by AI may make the profit cycle more difficult to predict, especially as HBM continues to squeeze DRAM capacity. The relationship between price, supply, and profit will become more complex, and the "estimated time" for profit peaks may shift rapidly.

therefore,Operating profit can be an important indicator, but it is by no means a "panacea".

AI is reshaping industries: ROE is undergoing a structural reset, and the upward trend is expected to continue until 2027.

UBS emphasizes that the current storage cycle is fundamentally different from the past. The advent of the AI computing era has led to a fundamental shift in value towards the storage field.

As HBM (High Bandwidth Memory) occupies an increasing share of DRAM wafer capacity, the DRAM shortage is becoming increasingly severe. Furthermore, the ever-increasing size of HBM DRAM chips further exacerbates the capacity constraints.

Based on these factors, UBS believes that the return on equity (ROE) of the storage industry has undergone a structural reset. (Report)It is predicted that from 2026 to 2030, the average ROE of Samsung, SK Hynix and Micron will reach 36%, far higher than the 15% of the past decade.

Therefore, the report remains optimistic about the future of storage stocks.The report projects that operating profits in the storage industry will peak in the third quarter of 2027. All else being equal, this means the upward trend in storage stocks could continue into the second quarter of 2027.

UBS continues to favor SK Hynix as its top pick, while also maintaining a "buy" rating on Samsung, Micron (MU), and Nanya Technology.

~~~~~~~~~~~~~~~~~~~~~~~~

The above exciting content comes from

For more detailed analysis, including real-time updates and firsthand research, please join [the group/group].

No Comments