作者:BlockBeats

"We went from eggs to yen," a financial memoir by CME legend Leo Melamed, testifies to the fact that eggs were once one of the most actively traded futures products in the world.

In the first half of the 20th century, egg futures were one of the most popular trading instruments in Chicago. In some years, trading volume was second only to grains, and there were even times when futures trading volume far exceeded spot trading volume.

The Chicago Mercantile Exchange (CME) was originally called the "Chicago Butter and Egg Board," which was the precursor to the entire derivatives empire. As its name suggests, the exchange initially only traded two things: butter and eggs.

After the 1970s, egg farming in the United States rapidly industrialized, and the cold chain matured, gradually smoothing out price fluctuations. As uncertainty began to disappear, the noise in the trading pit also subsided. In 1982, egg futures officially disappeared from the Chicago Mercantile Exchange. It didn't collapse dramatically; rather, it was quietly shut down by the times.

In 2013, the Dalian Commodity Exchange in mainland China reignited interest in this commodity. At that time, China's egg-laying hen industry was still highly fragmented, with prices fluctuating wildly, and the demand for hedging was real and urgent. Trading moved from the outcry floor in Chicago to the screens of electronic matching, and participants changed from floor traders in colorful vests to industrial clients and quantitative accounts staring at candlestick charts.

Egg futures trading hasn't disappeared, it's just migrated. And today, that migration has taken another step forward. The venue for trading egg prices has moved to Polymarket.

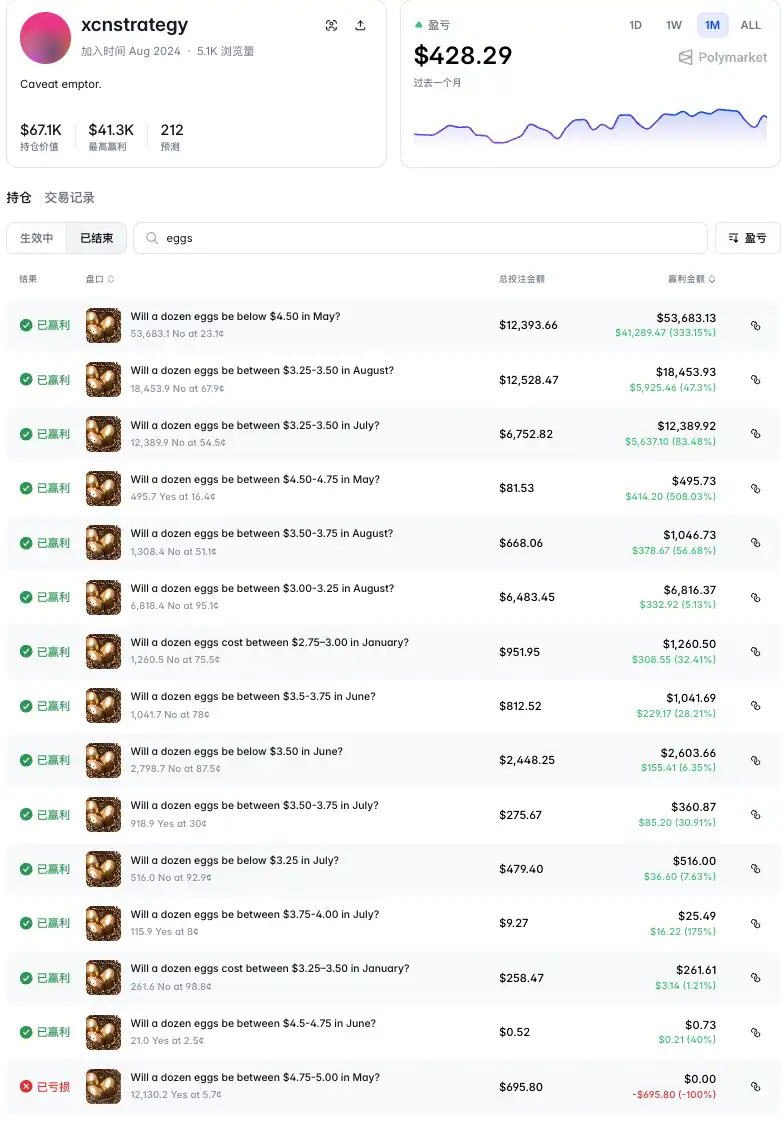

A trader with the ID "xcnstrategy" established positions based on egg price predictions across multiple expiration months in January, May, June, July, and August. The vast majority of these trades were short positions on a specific price range ("Yes"), essentially betting that eggs wouldn't reach a certain price level. The total bet was $44,800, resulting in a profit of nearly $100,000. All but the first of the 15 trades were profitable.

The most recent and most profitable trade was a $12,393 bet on "No. 5 for a dozen eggs in May below $4.50", which yielded a profit of $41,289 (+333%).

Regarding the speculation about xcnstrategy's true identity, many people believe that he is likely someone with a background in commodity markets or agricultural data research capabilities, who analyzed that the surge in egg prices caused by the avian flu in the United States in 2025 was a short-term phenomenon and that the market overestimated the probability of high prices continuing. Others believe that he is someone working in the upstream and downstream of the egg industry, hedging against fluctuations caused by the industry itself.

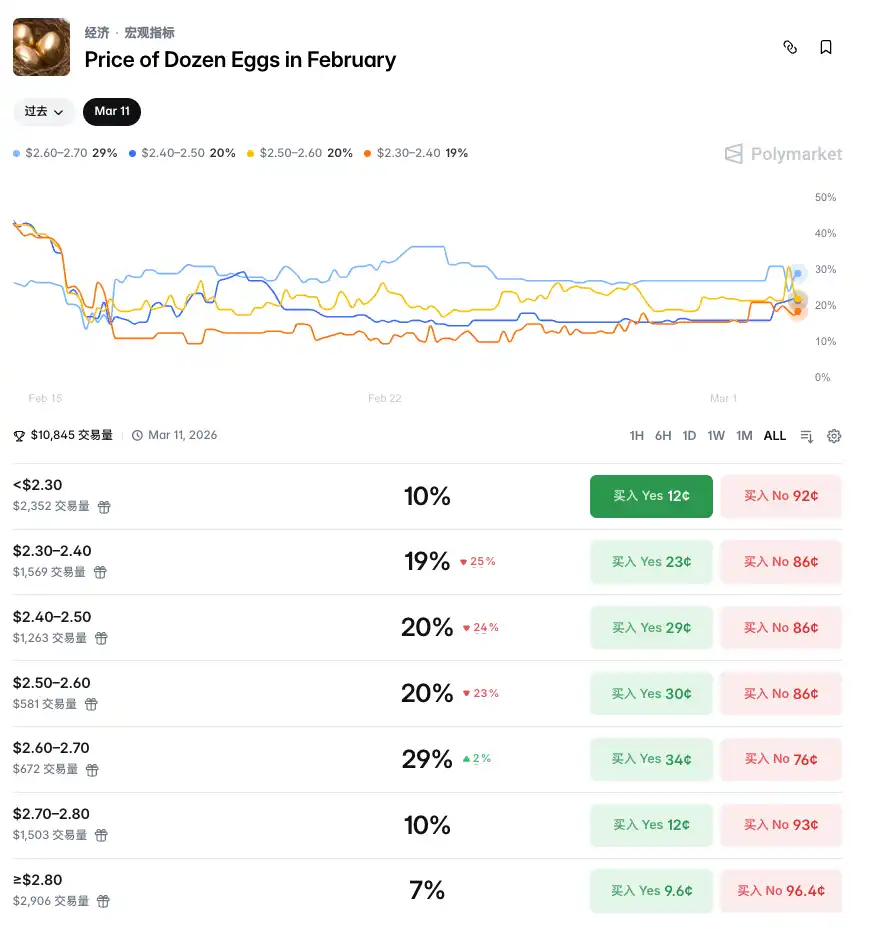

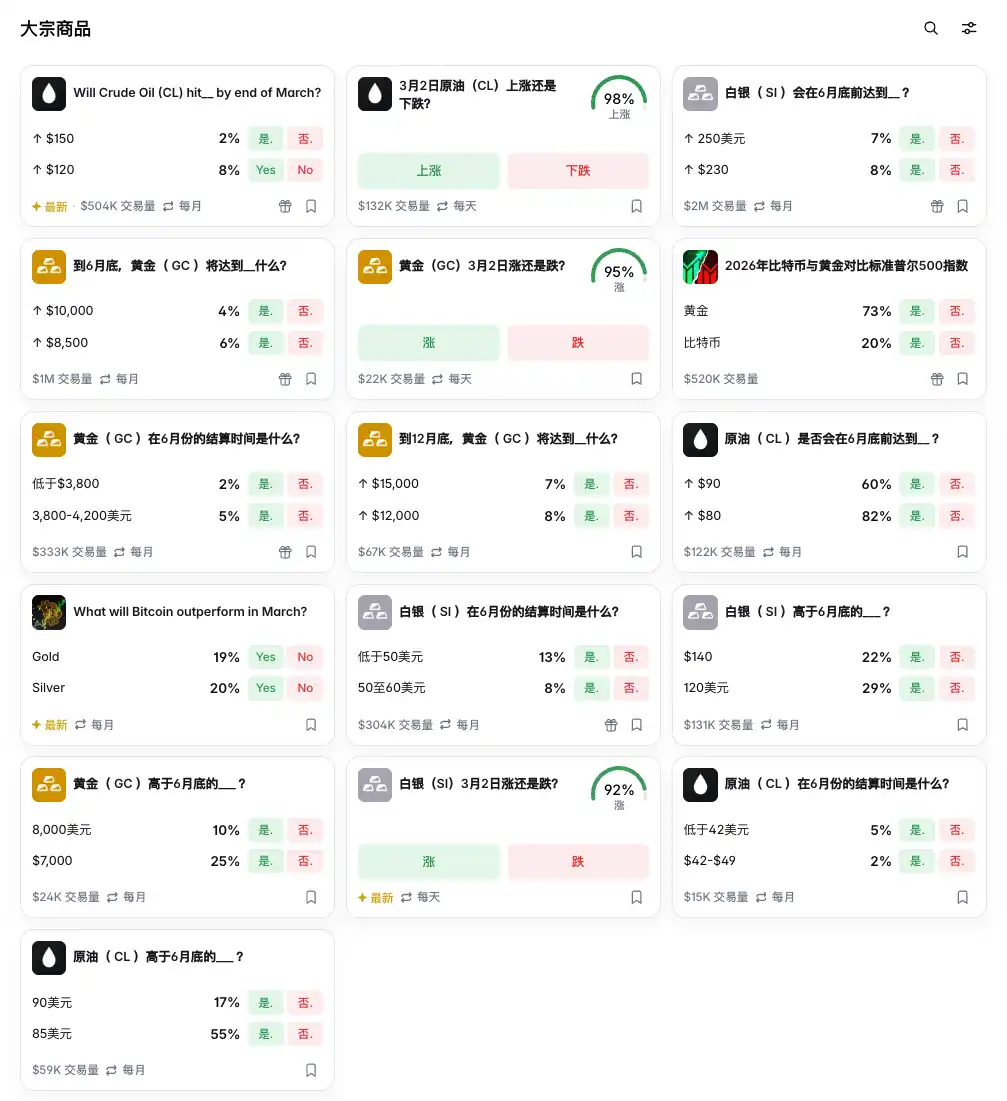

Eggs are just one example; the traditional assets traded on Polymarket are far more numerous than we imagine: from commodities like crude oil (CL), gold (GC), and silver (SI), to various foreign exchange prices, and even housing data, all can be found on Polymarket.

The fact that trading is available 24/7 is one of the biggest advantages of trading such orders on Polymarket. This advantage is very obvious when traditional financial markets are closed, as evidenced by the escalation of the US-Iran conflict last weekend.

Hyperliquid offers the same advantage in this regard. Hyperliquid's perpetual contracts linked to crude oil and gold have no expiration date and operate 24/7.

This leads to an increasingly undeniable phenomenon: the crypto market is quietly taking over the pricing function of traditional financial markets, especially when the latter are shut down.

Traditional futures markets have fixed trading hours, CME crude oil and gold contracts are closed on weekends, and the foreign exchange market experiences a liquidity crunch late at night. This means that when a geopolitical shock suddenly erupts after Friday's close, participants in traditional markets can only wait in the dark, unable to hedge, express their opinions, or price their positions.

The escalation of the US-Iran conflict last weekend is the latest example. According to Bloomberg, before and after the conflict, a large number of traders flocked to Hyperliquid to trade perpetual contracts linked to crude oil and gold to cope with the geopolitical shock—at a time when traditional markets were closed, the crypto derivatives market became the only place with its lights on. Investment executive Avi Felman had previously predicted that "Hyperliquid will become indispensable for fund managers because of its 24/7 operation." This prediction has been concretely validated in this round of conflict.

Meanwhile, the tokenization of gold is also accelerating another logical trend: when gold exists as on-chain tokens and is continuously priced in decentralized markets, it no longer needs to wait for the London Metal Exchange or CME to open. To some extent, the tokenized gold market is acting as a "shadow pre-market" for the traditional gold market, pricing gold in advance over the weekend, allowing price discovery to occur before the traditional market opens.

In 2020, FTX, then the world's second-largest stock exchange, launched a stock token that allowed users to trade Tesla and Nvidia stocks with stablecoins. The idea was to gain pricing power. When the US stock market was closed, Tesla tokens on FTX could fill the market gap, allowing users to trade Tesla stock when Tesla announced its latest model on Saturday, thereby influencing the Nasdaq opening on Monday.

Unfortunately, due to liquidity issues, the pricing effect was ultimately not achieved. Six years later, tokenization has come full circle back to this vision. Today, Polymarket and Hyperliquid are seen by many as more than just cryptocurrency trading platforms. Polymarket is now an officially recognized polling agency and information exchange center, while Hyperliquid is widely regarded as a new type of wholly-owned product trading platform.

Price discovery has always been one of the most core powers in financial infrastructure. Chicago butterflies established the CME because they needed a venue to discover prices and transfer risk.

More than a hundred years later, the same logic is being repeated on the blockchain, only the medium has changed.