作者:区块律动

Bitdeer is the largest Bitcoin miner in the US by hashrate. This week, it emptied its entire BTC treasury—from 2017 to zero. Simultaneously, the company completed a $325 million convertible bond financing and equity issuance. This is not an isolated event: hashrate is approaching the break-even point for many miners, and a structural shift is quietly underway, transforming miners from "coin-hoarding machines" into "BTC-fueled operating machines."

The full text is as follows:

Bitdeer, the largest Bitcoin miner in the United States by computing power, completely emptied its BTC ledger this week.

The company's BTC Treasury balance currently shows 0 – it sold 189.8 newly mined BTC and withdrew 943.1 BTC from its reserves to sell as well.

Mining companies holding Bitcoin are like pressure in a pipeline: part of it flows out as revenue, and part remains in the national treasury as a store of value and a buffer. The state of the buffer reflects the management's judgment on the road ahead.

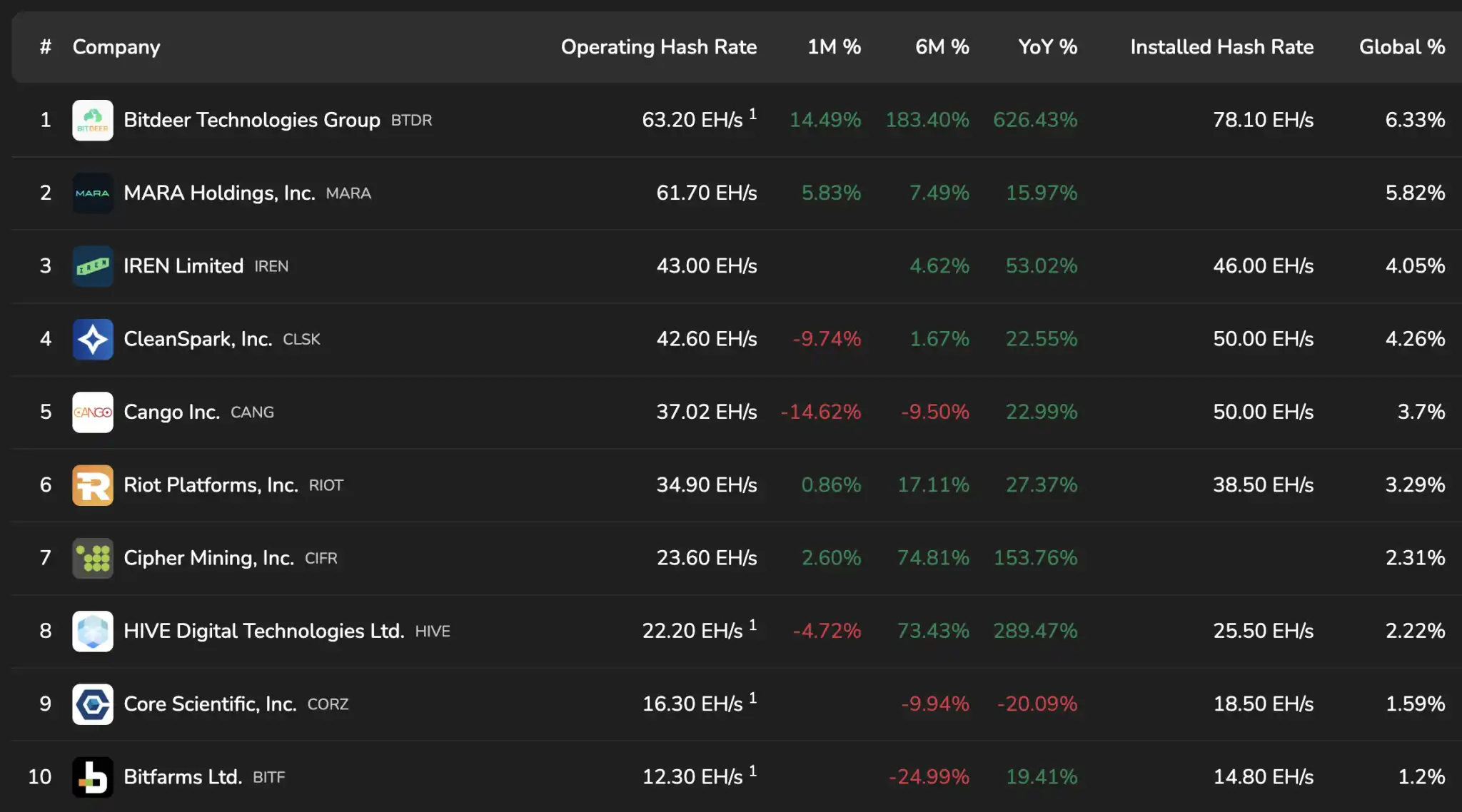

Bitcoin hashrate ranking

Source: bitcoinminingstock.io

Bitdeer's cash buffer went to zero in one go, which raises the question: why is this miner so desperate for cash? And how does it view the next quarter?

In the mining industry, bills come in fiat currency—electricity, hosting fees, wages, spare parts—while revenue comes in Bitcoin. Therefore, every treasury policy is essentially a statement about timing, risk, and access to capital.

This weekly report also has a second layer of meaning. Bitdeer's balance sheet still shows a considerable BTC holding at the end of the year—in the announcement on December 31, 2025, the company disclosed holding "2,017 Bitcoins".

From four-figure holdings to a weekly update showing zero, this tells the whole story of rhythm, cash conversion, governance models, and the ever-reinventing business of mining.

In summary, this weekly report presents a company that has proactively chosen certainty—transforming a shrinking (dollar-denominated) reserve into operational liquidity and adjusting its risk exposure to resemble that of a utility company rather than a hoarding account. This is where the term "capitulation" comes in: it describes what happens when the profit margin meter approaches the red line—the treasury transforms from a strategic reserve into fuel.

Based on weekly data, Bitdeer sold approximately 1,132.9 BTC (943.1 BTC in reserves plus 189.8 BTC newly mined). Estimated from the $60,000 to $70,000 range shown on Bitdeer's Mining Insights page, this represents approximately $68 million to $79 million in liquidity—enough to have a substantial impact on miners' cash cycles and signal a shift in stance.

A treasury bill coincides with a financing calendar.

This BTC sale occurred concurrently with what appears to be a deliberate restructuring move in the capital markets. Bitdeer announced the completion of pricing for its $325 million, 5.00% interest rate, convertible senior notes maturing in 2032, and simultaneously completed a registered direct offering priced at $7.94 per share.

The intended uses of the funds include: capped call transactions, repurchasing $135 million of convertible bonds due in 2029, and funding for data center expansion, HPC and AI businesses, ASIC R&D and operations.

This series of actions tells you where the money wants to go and what risks the company is willing to take along the way.

Convertible bonds and hedging options are financial conduits—they encapsulate volatility, trading upside potential for survival, aiming to keep the gears running even when revenue is struggling. A miner completing financing and debt restructuring within the same timeframe as emptying its BTC account signals a preference for controllable financing channels and for building infrastructure that can continuously generate orders, computing power, and contracts.

This logic aligns with the larger narrative of 2026—miners are increasingly positioning themselves as “energy-to-computing” businesses, with Bitcoin as one revenue stream and AI and HPC as another capital-intensive destination.

VanEck's 2026 outlook suggests that this transformation in the mining industry presents both opportunities and pressures, and anticipates industry consolidation as balance sheets absorb the costs of growth.

The price of computing power determines the pace, while the forward curve determines expectations.

Mining failures rarely end with a bang; they are a series of drifts, tightening, and forced small decisions that eventually converge into one big one. The industry's profit meter is hashprice—the revenue per unit of computing power—and recent readings explain why the Treasury must liquidate its holdings.

Luxor's latest hashrate index report places the USD hashprice at $34.05 per PH per day, down about 4% week-over-week, and notes that for many miners, the current hashprice is close to break-even, depending on their respective cost structures and mining rig types.

Forward market pricing indicates an average of approximately $28.73 per PH per day over the next six months—a lower expectation that acts like gravity on every Treasury policy.

The difficulty setting is the second knob, which adjusts the denominator. It can be quickly adjusted when weather, shutdowns, or power outages cause the miner to go offline.

Bitcoin experienced a record 11.16% difficulty drop to 125.86T, followed by a record rebound to 144.40T. The next correction is expected to occur in early March. This pattern resembles a whiplash reaction for miners who plan their capital expenditures and liquidity on a weekly and monthly basis.

Bitdeer's own dashboard reflects the same situation—Bitdeer lists its network hashrate at approximately 1,022 EH/s, difficulty at approximately 144.4T, and daily earnings per terahash at $0.0289. Miners must survive in the space created by these numbers and choose where to absorb volatility: the national treasury, the debt heap, or growth plans.

Surrender first comes in the form of accounting, then in the form of integration.

When traders talk about “capitulation,” they imagine a waterfall—a sudden cleansing that wipes the books to zero. Capitulation in the mining industry often takes the form of book entries and financing terms: selling coins, cutting reserves, pricing convertible bonds, issuing new equity, and weaker operators being forced to merge or shut down.

Bitdeer's actions this week align with a narrative of using government treasury liquidation as a financing bridge—converting BTC into cash to support larger-scale construction and debt restructuring. This includes channeling the proceeds into hedging options trades, repurchasing existing convertible bonds, and funding research and operations in data centers, HPC, AI, and ASICs. Companies operating under this script are treating Bitcoin as an inventory that can be converted into concrete, chips, and contracts.

The forward market price for Luxor hashrate is approximately $28.73 per PH per day, implying continued pressure on profit margins. This pressure often pushes miners to one of three options: sell BTC, sell equity, or sell the company itself.

VanEck's outlook characterizes 2026 as a consolidation phase, pointing directly to financing options—dilutive convertible bonds, treasury sales during periods of weak prices, and the divergence between operators capable of running both Bitcoin mining and AI computing power on two tracks, and those that can only maintain one.

This is why Bitdeer's liquidation of its reserves may be a case of the canary in the coal mine. This event serves as both a case study and a cautionary tale. Miners can maintain exposure to Bitcoin through continuous operation while holding fewer actual tokens; they can also reposition themselves as infrastructure companies, shifting Bitcoin price risk to other areas for management.

If the entire industry replicates this transaction, the number of miners accumulating BTC on their balance sheets will decrease, and miners' cash flow will become more sensitive to short-term profitability.

What to focus on next?

First, the continuity of the policy. A week-long liquidation could be a matter of timing, but a pattern that continues for several months signifies a new treasury doctrine. The most useful signal will be the updates in the coming weeks—the same "BTC Holdings" row will again list company holdings and customer deposits separately.

Second, the cost of capital. Convertible bonds and equity financing terms indicate that the company is building its survival space, but when hashprices tighten, this survival space becomes a competitive weapon. Under pressure, miners with lower financing costs buy time, while miners with higher financing costs sell coins, shares, and assets.

Third, the profit margin context. The Luxor hashrate index places hashprice near the break-even point for many miners, and the dramatic fluctuations in difficulty show how quickly the denominator can swing while the network is still adjusting. Miners build on these constantly shifting foundations, and their treasury acts as a shock absorber.

The cleanest interpretation of this week is procedural: miners follow incentives, which flow through hashprice, difficulty, and funding terms.

Bitdeer converted its reserves into cash, and in the same week it did so, it was also adjusting its capital structure and clarifying its future spending priorities—data centers, HPC, AI, and ASIC.

The industry as a whole can absorb a single company emptying the national treasury, but it must also face the reality of this model: a mining ecosystem that treats Bitcoin as a throughput rather than a hoarding asset and treats balance sheet exposure as an adjustable knob based on operating costs is gradually taking shape.