作者:中金点睛

summary

The Warsh path can be broadly summarized as "interest rate cuts and balance sheet reduction," which will likely be accompanied by fiscal expansion and the need to stabilize long-term bond yields. The core of this article is not to judge whether the Warsh path will be implemented, but rather to attempt to analyze the Warsh path from the perspective of China's experience and its implications for monetary policy operations in both China and the United States.

China's situation over the past few years can be described as "the central bank not expanding its balance sheet, banks expanding their assets, and explicit fiscal expansion."At times, it also faces the challenge of a slowdown in the pace of bank balance sheet expansion. However, during this process, government bond yields did not rise significantly. This example can help us understand the "Wash path" to some extent.

The lesson from the Chinese experience is that...The impact of liquidity on government bond yields will exist in the short term, but the central bank has the ability to mitigate this issue through monetary operations and regulatory optimization.If Warsh wants to achieve "interest rate cuts and balance sheet reduction" without triggering a significant rise in Treasury yields, optimizing the regulatory and monetary policy framework is imperative. Of course, the Chinese and American financial systems are different. China's system is bank-centric, while non-bank financial institutions play a crucial role in the US, and the two countries have their own characteristics in terms of liquidity arrangements.

Another challenge to the Warsh path lies in the fundamentals, particularly the stability of inflation expectations.If inflation expectations rise disorderly, long-term bond yields will be difficult to stabilize, and the market will worry about the sustainability of loose monetary policy: has the debt actually translated into more inflation and trade deficits, or has it truly driven improvements in economic efficiency? The Walsh path itself is a response to stabilizing inflation expectations. Future challenges still exist, and there are two solutions to prevent disorderly rises in inflation expectations under a state of both fiscal and monetary easing: one is that aggregate demand is negatively impacted, and the other is that aggregate supply continues to expand and total factor productivity of the economy improves. China's experience is a combination of these two aspects.

For the United States, how can it simultaneously reduce its balance sheet, cut interest rates, expand fiscal policy, and prevent Treasury bond yields from rising?First, we need to optimize monetary policy operations and financial supervision. Second, we need to stabilize inflation expectations by either tightening aggregate demand or expanding aggregate supply. The former may lead to larger and more decisive interest rate cuts, which could lower real interest rates. The latter is a desirable option but is more difficult and may lead to higher real interest rates.

What lessons can China learn from the United States' experience?First, regulatory design and the central bank's balance sheet can assist in the transmission of monetary policy, while the design of the exit path is also very important. Second, exogenous monetary injection is very effective in expanding demand and inflation expectations, while supply-side reforms cannot be ignored. Third, both aggregate monetary policy and structural monetary policy are important for economic development.

China's experience offers valuable insights for understanding the Walsh path.

Recently, Trump nominated Kevin Warsh to be the next Federal Reserve Chairman. There is considerable controversy in the market regarding Warsh's policy path of lowering long-term interest rates through a combination of "interest rate cuts and balance sheet reduction".

Warsh argues that the root cause of US inflation lies in the Federal Reserve's expansion of its balance sheet through QE and other means, which, in conjunction with fiscal policy, leads to excessive money supply. Therefore, the size of the Federal Reserve's balance sheet should be controlled, and the independence of the Federal Reserve from the Treasury should be rebuilt to guide fiscal control of deficits and debt, thereby enhancing the effectiveness of the Federal Reserve's interest rate cuts.

The core of the market's controversy lies in the fact that the impact of "interest rate cuts and balance sheet reduction" on liquidity is both positive and negative, making it difficult to draw a directional conclusion, especially against the backdrop of US fiscal expansion.

In fact, the situation in China can provide a reference for understanding Walsh's policy path.China's fiscal deficit has generally expanded over the past few years, and the monetary policy mix can be broadly summarized as "banks expanding their balance sheets + the central bank not expanding its balance sheets," a process accompanied by a decline in long-term interest rates.

As of December 2025, the total assets of my country's central bank reached 48.2 trillion yuan, accounting for approximately 34.4% of GDP, 2.5 percentage points lower than at the end of 2019 (36.9%). During the same period, the ratio of commercial banks' total assets to GDP increased from 287.6% to 337.9% (Chart 1), the ratio of government bonds to commercial banks' total assets rose from 10.6% to 15.8%, and the 10-year treasury bond yield fell from 3.14% to 1.85%.

Chart 1: my country's central bank has not expanded its balance sheet in the past few years, while total bank assets have expanded.

Source: Wind, CICC Research Department

There are two reasons why long-term interest rates in China have not risen despite fiscal expansion and a lack of balance sheet expansion by the central bank:First, in terms of liquidity, the central bank provided strong support to banks in terms of liquidity and financial supervision for taking over treasury bonds. Second, in terms of fundamentals, China's inflation expectations have not risen.

Liquidity: Optimizing monetary operations and financial regulation

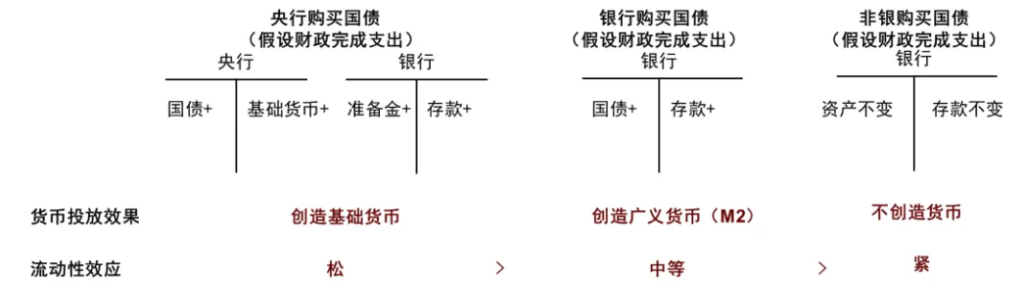

Theoretically, there are fundamental differences in the supply and demand of money when the central bank buys bonds, banks buy bonds, and non-banks buy bonds.

From the perspective of the financing party, the issuance of government bonds and the subsequent spending will drive up the demand for money. However, different buyers have different effects on the money supply (Chart 2): the process of the central bank buying bonds will automatically create a base money supply.

When banks buy bonds, they do not create base money, but they do create M2, and a portion of excess reserves are converted into required reserves. Non-bank institutions buying bonds do not create any money; they only lead to adjustments between different deposits within the bank's liabilities. Therefore, ranked from tightest to loosest liquidity, non-bank institutions buying government bonds is the tightest, central bank buying government bonds is the loosest, and bank buying government bonds falls in between.

Chart 2: The impact of central bank, banks, and non-bank financial institutions purchasing government bonds on liquidity is fundamentally different.

Source: CICC Research Department

So, if the central bank doesn't expand its balance sheet but instead allows banks and non-bank financial institutions to purchase government bonds, how can liquidity stability be ensured? China's experience in this regard may offer some lessons for the United States:

First,Reducing the "liquidity constraint" on banks by purchasing government bonds.As shown in Chart 2, when banks purchase government bonds from residents, they create a deposit on the liability side. As a result, a portion of the excess reserves need to be converted into required reserves. If the scale of bond purchases is large, it may trigger a tightening of bank liquidity.

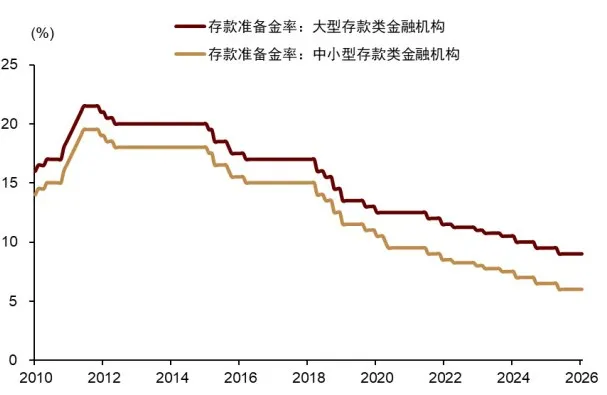

Therefore, the central bank needs to appropriately reduce the statutory reserve requirement ratio and release more excess reserves. From the end of 2019 to the end of 2025, the statutory reserve requirement ratio of large deposit-taking financial institutions in my country was reduced from 13% to 9%, and the statutory reserve requirement ratio of small and medium-sized institutions was reduced from 11% to 6% (Chart 3). During the "14th Five-Year Plan" period (2021-2025) alone, the central bank released 7 trillion yuan of liquidity through the reduction of the reserve requirement ratio[1].

Chart 3: The central bank has lowered the required reserve ratio multiple times.

Source: Wind, CICC Research Department

Chart 4: The scale of interbank pledged repo transactions in my country is growing rapidly.

Source: Wind, CICC Research Department

second,Reduce the "capital constraint" of government bonds on banks.Government bonds have a risk weight of 0, so from the perspective of traditional capital adequacy ratio (RWA) regulation, banks purchasing government bonds consume almost no risk capital. However, when asset size expands during the bond purchase process without a corresponding increase in Tier 1 capital, it lowers the leverage ratio (net Tier 1 capital/adjusted total assets). Compared to the United States, China is more pragmatic on this issue: China's regulatory focus remains on risk-weighted capital constraints and liquidity management, and it does not impose strict, rigid total exposure constraints on government bond allocations similar to the SLR/eSLR led by the Federal Reserve. When Chinese commercial banks purchase government bonds, they are generally not constrained by leverage ratios, while large US banks, measured by "total exposure" under the SLR framework, do not offer preferential treatment to low-risk assets and are more likely to be constrained when purchasing government bonds.

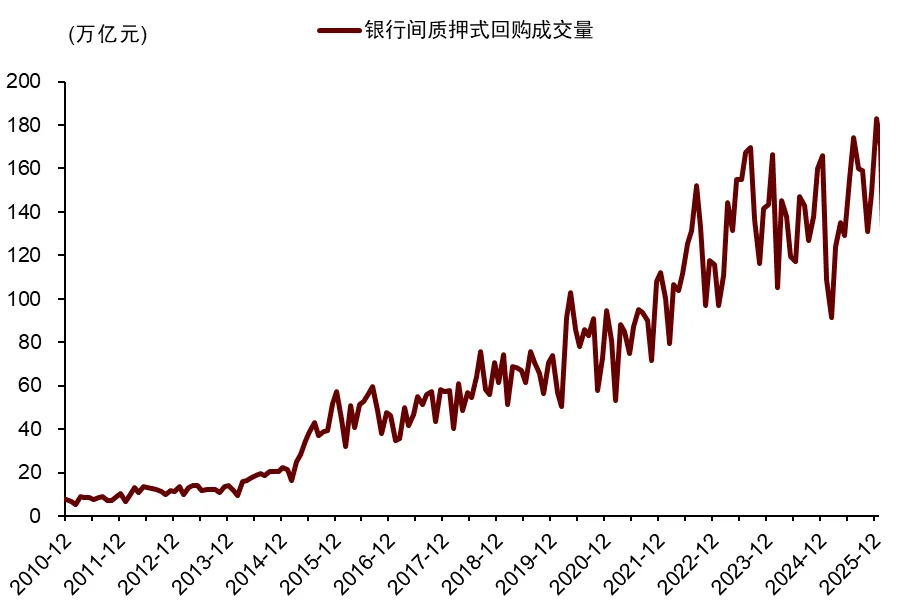

third,Increasing the central bank's support for the entire money market means not only supporting banks, but also assisting banks in supporting non-bank financial institutions.The central bank injects liquidity into banks, which then lend funds to non-bank financial institutions through pledged repurchase agreements. These non-bank institutions can then use the funds to increase their holdings of government bonds. From the end of 2019 to the end of 2025, the monthly transaction volume of pledged repurchase agreements in my country is expected to increase from 74 trillion yuan to 183 trillion yuan (Chart 4).

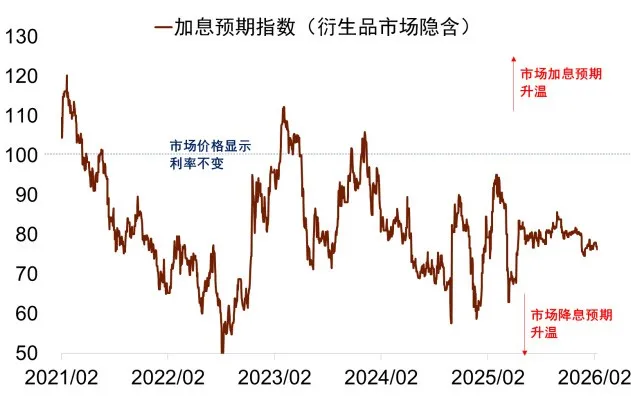

fourth,This guides the market's expectations for short-term interest rates downward, reducing banks' expectations for funding costs.For most of 2021, the interest rate swap market has anticipated future interest rate declines (Chart 5). This is partly due to fundamental factors.

Chart 5: Over the past few years, the market has expected interest rates to fall most of the time.

Source: Wind, CICC Research Department

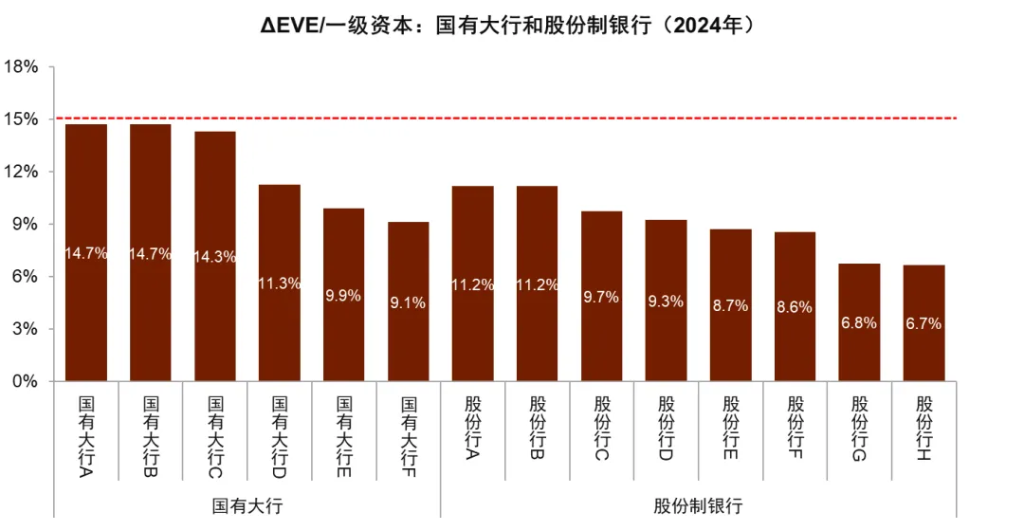

Since the end of last year, China has also faced a liquidity challenge: if the pace of bank balance sheet expansion slows down, how can long-term bond yields be stabilized, given that the central bank is not expanding its balance sheet?In the past few years, Chinese commercial banks have taken on a large amount of long-term treasury bonds, while deposits on the liability side have shown a trend towards becoming more demand deposits, resulting in an increase in the mismatch between asset and liability duration. This mismatch is reflected in the specific regulatory indicator of the ratio of economic value change to Tier 1 capital, namely ΔEVE/Tier 1 capital (hereinafter referred to as ΔEVE). Currently, some banks' levels of this indicator are very close to the regulatory threshold of 15% (Chart 6).

Chart 6: In 2024, the ΔEVE and Tier 1 capital ratio of some major state-owned banks approached the 15% limit.

Data source: Reports on the third pillar of the national economic growth model of listed banks, Wind, CICC Research Department

We believe that, from an annual perspective, this constraint may not pose a significant problem.In our report, "Will 'Risk Prevention' Become a Limit to Interest Rate Declines?", we analyzed the following:

First and foremost, the most important risk prevention approach is to take a holistic view and ensure the effectiveness of macroeconomic policy transmission, rather than adhering to a fixed regulatory indicator.Globally, major developed countries, in response to insufficient demand and the subsequent reduction of monetary policy interest rates to zero, did not strictly adhere to the regulatory requirements for ΔEVE. Instead, they adjusted the implementation based on the realities of their financial systems. While this approach may seem controversial in retrospect, we believe it essentially reflects a holistic view of risk prevention: when aggregate demand is insufficient, the greatest risk prevention measure is ensuring the smooth implementation of counter-cyclical policies; the potential shock risk from rising interest rates can be considered a relatively secondary concern.

Even if relevant regulations are implemented, some technical requirements for ΔEVE can be adjusted, such as appropriately lowering the assumption of interest rate shocks.The value of ΔEVE is positively correlated with the magnitude of the interest rate shock assumption. Basel III assumes that my country’s parallel interest rate shock is 225bp, which is higher than that of Japan (100bp) and the United States (200bp). The magnitude of the interest rate shock assumption for each country depends on the fluctuation of government bond yields. The Basel Committee also allows countries to adjust their assumptions as appropriate [2]. Using the same data [3] and methods as Basel III, we calculated that my country’s parallel interest rate shock should be around 200bp. If we remove the rapid decline in government bond yields during the 2008 financial crisis, my country’s parallel interest rate shock should be around 150bp.

In addition, the 15% regulatory threshold for ΔEVE can be appropriately increased with reference to the Japanese experience.Japan's interest rate risk regulation for small and medium-sized banks takes into account their operational realities. Since 2018, Japanese multinational banks have been subject to the book interest rate risk regulation requirements of the Financial Services Agency of Japan, with a ΔEVE threshold of 15%; Japanese domestic banks (most of which are small and medium-sized banks) have been subject to the regulation since 2019, with the denominator of ΔEVE relaxed from Tier 1 capital to total capital, and the threshold also raised to 20%[4]. Even so, every year from 2019 to 2024, some Japanese domestic banks exceeded the ΔEVE threshold, with a maximum of 16 banks. This is because, compared with large banks, Japanese small and medium-sized banks are highly dependent on the Japanese domestic market, cannot expand into overseas markets, have a high proportion of interest income, and it is reasonable for them to choose to purchase long-term bonds in their operations.

The lesson from China's experience is that while the impact of liquidity on government bond yields may exist in the short term, the central bank has the ability to mitigate this issue through monetary operations and regulatory optimization.If Warsh wants to achieve "interest rate cuts and balance sheet reduction" without triggering a significant rise in Treasury bond yields, optimizing the regulatory and monetary policy operation framework is imperative.

From a liquidity perspective, the United States has many policy options to ensure that the Federal Reserve's balance sheet reduction and long-term interest rates remain largely stable. Some changes are not easy to implement in the short term, but they are not entirely impossible.At the risk of oversimplification, if the Federal Reserve shrinks its balance sheet, then other financial institutions will need to expand their assets to accommodate Treasury bonds.

For example, the Federal Reserve could increase reverse repurchase support for financial institutions to use Treasury bonds as collateral for financing, alleviate the liquidity pressure on financial institutions, especially hedge funds, and allow non-bank financial institutions to purchase Treasury bonds; it could consider setting up a liquidity tool specifically for TGA; in addition, it could adjust the regulatory requirements related to SLR (Governor Milan proposed that US Treasury bonds should be completely removed from the denominator of SLR[5]) to allow commercial banks to expand their balance sheets and accept Treasury bonds.

It is important to note that the financial systems of China and the United States are not entirely identical, and how to hedge against the challenges faced by non-bank liquidity may be a more important issue for the United States.China's financial system is centered on banks. Commercial banks are the main holders of Chinese government bonds. Although non-bank institutions participate, their overall leverage ratio is low, and the size of hedge funds is far smaller than that of the United States.

China's pledged repo market primarily circulates within the banking system, giving the central bank more direct control over liquidity. Therefore, China's liquidity risk is more reflected in structural changes on bank balance sheets than in the disruption of financing chains for highly leveraged non-bank institutions.

In stark contrast, the United States is a typical example.Market-based financial systemWhile banks remain important intermediaries, the marginal price setters in the Treasury market are often not traditional commercial banks, but rather hedge funds, money market funds, pension funds, and other asset management institutions. Particularly in the Treasury basis trade between spot and futures bonds, hedge funds leverage repurchase agreements to finance, assuming significant inventory and arbitrage functions. This means that liquidity in the US Treasury market largely depends on the ability of non-bank institutions to obtain short-term financing through the repurchase market.

Fundamentals: How to stabilize inflation expectations?

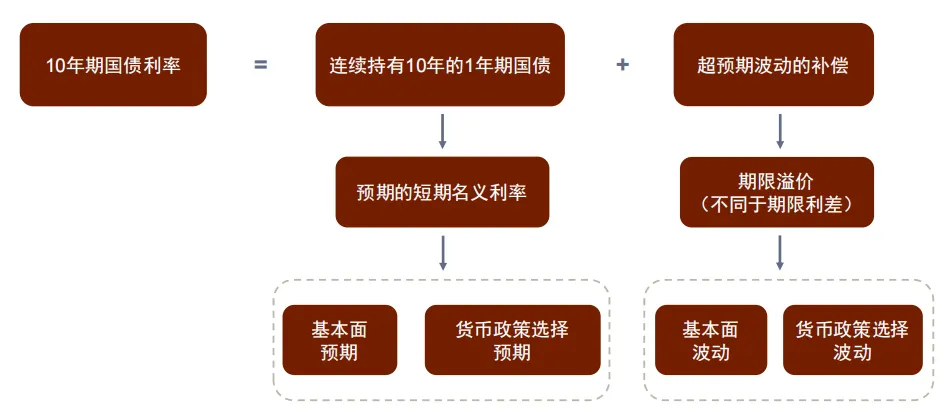

Chart 7: Breakdown of 10-Year Treasury Bond Yields

Source: CICC Research Department

The challenges of the Warsh path, besides liquidity, lie in macroeconomic fundamentals, particularly the stability of inflation expectations. This is because inflation expectations simultaneously affect short-term interest rate expectations and term premiums.This analytical framework is shown in Figure 7. For details, please refer to our previously published report, "Where is the Bottom of Interest Rates | The Long Cycle Series (Part Two)". Specifically:

First, inflation expectations will influence the expected path of short-term interest rates.If inflation expectations continue to rise, investors will expect short-term interest rates to also continue to rise.

Secondly, inflation expectations also affect term premiums.If the average nominal interest rate is expected to be 1.0% over the next 10 years, will the Treasury bond yield be 1.0%? Of course not. Investors also need to consider the probability of fluctuations along the entire path, including tail risks. If inflation expectations are at risk of rising uncontrollably, investors will firstly question the monetary authorities' response to inflation; secondly, they will question whether fiscal expansion has translated more into inflation, leading to larger trade deficits and external debt, rather than into real growth and improved economic efficiency, which will affect investors' confidence in the sustainability of fiscal authorities.

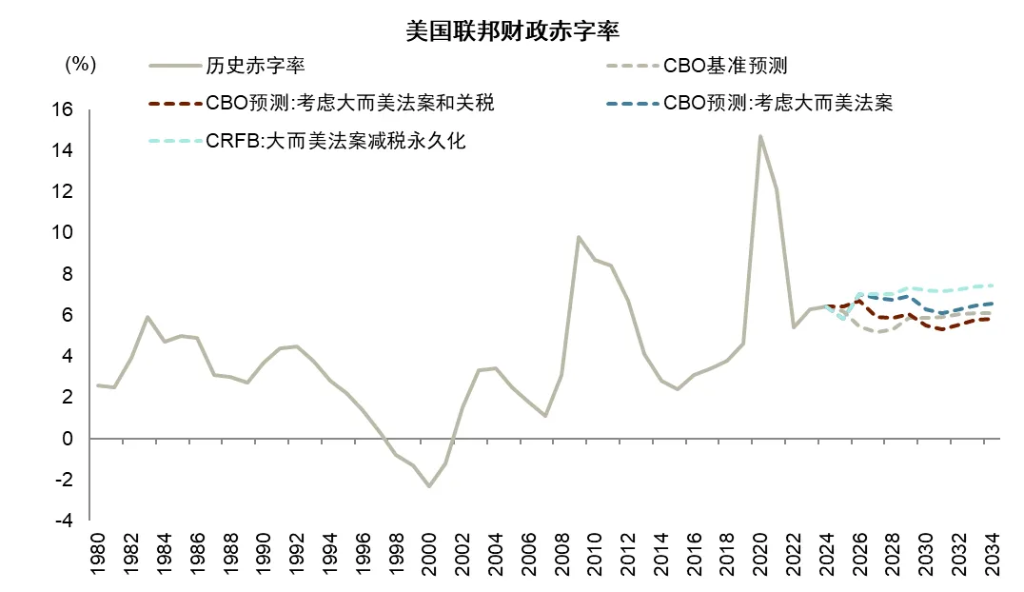

The US fiscal easing seems difficult to reverse, and the proposal of the Warsh path itself is an inherent requirement for stabilizing inflation expectations.The US fiscal expansion exhibits structural, institutional, and political entrenching trends, making its "loose monetary policy" extremely difficult to reverse in reality.

On the one hand, the proportion of mandatory expenditures such as social security, medical insurance, defense and debt interest continues to rise, and the deficit is no longer mainly driven by cyclical stimulus, but is embedded in the aging and debt rolling mechanism;

On the other hand, the widening partisan divide and electoral politics have increased the political costs of cutting welfare or raising taxes, and fiscal austerity lacks a consensus basis for implementation. It is worth noting that while the current US unemployment rate is only 4.3%, the federal fiscal deficit rate for fiscal year 2024 will reach 6.4%, the highest level since World War II except for the subprime mortgage crisis and the pandemic. The CBO predicts that the US fiscal deficit rate will remain at 6-7% for a long time (Chart 8).

If the central bank directly coordinates fiscal expansion with balance sheet expansion, the resulting money supply is exogenous money, which has a strong stimulating effect on inflation. Exogenous money is money whose issuance is not directly constrained by economic costs; it's similar to newly discovered gold, directly creating new demand and driving the economy. The opposite of exogenous money is endogenous money, such as money created through lending, which is itself constrained by economic costs and reflects demand and is a result of economic activity. The Warsh path itself was proposed to stabilize inflation expectations.

Chart 8: The CBO expects the U.S. federal fiscal deficit rate to remain high.

Data source: CBO, Haver Analytics, CICC Research Department

How can we prevent inflation expectations from rising disorderly under the background of fiscal and monetary easing? There are two solutions: one is credit tightening, which means the economy will naturally weaken, supply will remain unchanged, demand will decrease, and inflation expectations will come down; the other is that total factor productivity of the economy will increase, demand will remain unchanged, but supply will increase, and inflation expectations will also be effectively controlled.

China has combined these two solutions over the past few years.Therefore, while the central bank has not expanded its balance sheet and fiscal policy is still expanding, government bond yields have not risen. Specifically:

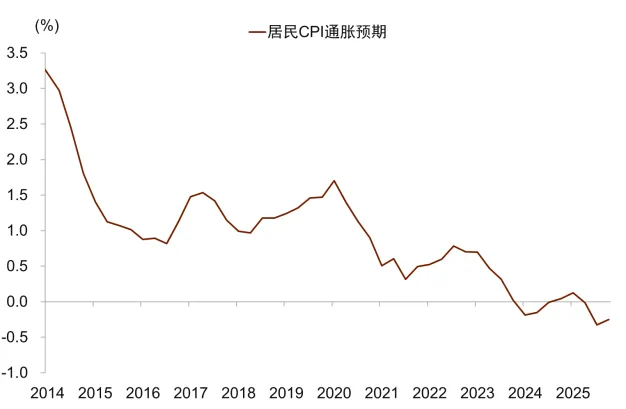

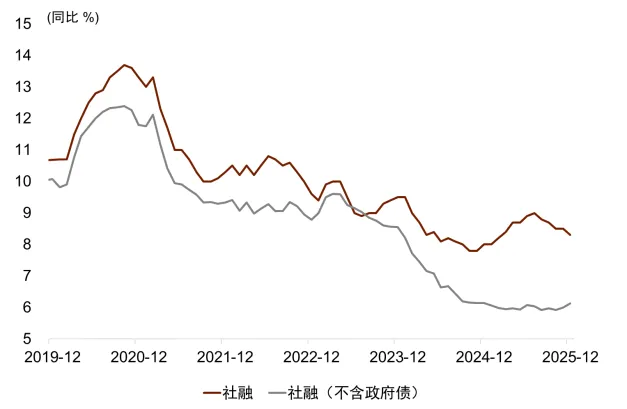

In the process of China's central bank not expanding its balance sheet and fiscal expansion, credit tightening is accompanying the situation, so there is no need to worry about inflation expectations derailing and rising.From the end of 2019 to the end of 2025, the year-on-year growth rate of social financing in China's private sector will decrease from 10.1% to 6.1%, and the year-on-year growth rate of outstanding RMB loans will decrease from 12.3% to 6.4%. During the same period, based on the central bank's urban depositors survey, residents' expectations for the year-on-year CPI in the next quarter will decrease from 1.5% to around -0.3%. Since 2025, residents' inflation expectations have not improved along with the actual rise in inflation (Chart 9, Chart 10).

Chart 9: Household inflation expectations have declined somewhat.

Source: Wind, CICC Research Department

Chart 10: Private sector social financing growth is at a historical low.

Source: Wind, CICC Research Department

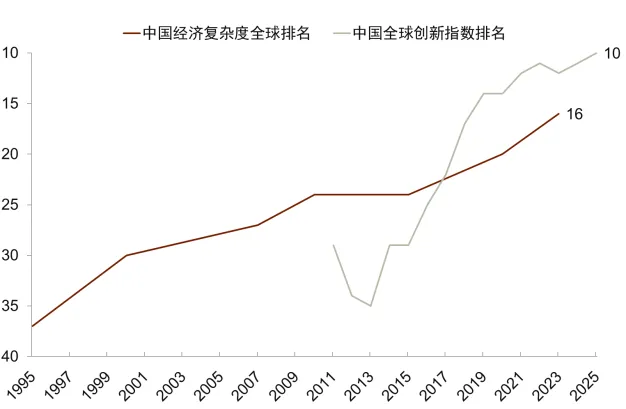

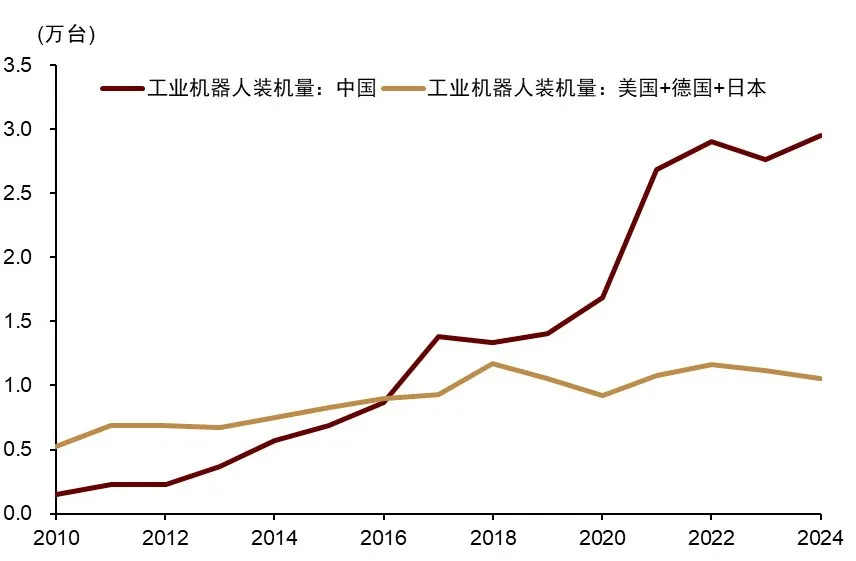

Another path is to improve total factor productivity. During the period of the central bank not expanding its balance sheet while engaging in fiscal expansion, China has made significant progress in both technological innovation and large-scale supply capacity.In recent years, China's industrial scale and automation have steadily improved. In 2023, China's economic complexity ranked 16th in the world, only one place behind the United States (Chart 11). The number of industrial robots installed doubled from 2019 to 2024, and is now nearly three times the total number of the United States, Japan and Germany (Chart 12).

Chart 11: China's economic complexity and innovation index are steadily improving.

Source: Wind, CICC Research Department

Chart 12: China's installed industrial robot capacity exceeds the combined total of the US, Japan, and Germany.

Source: Wind, CICC Research Department

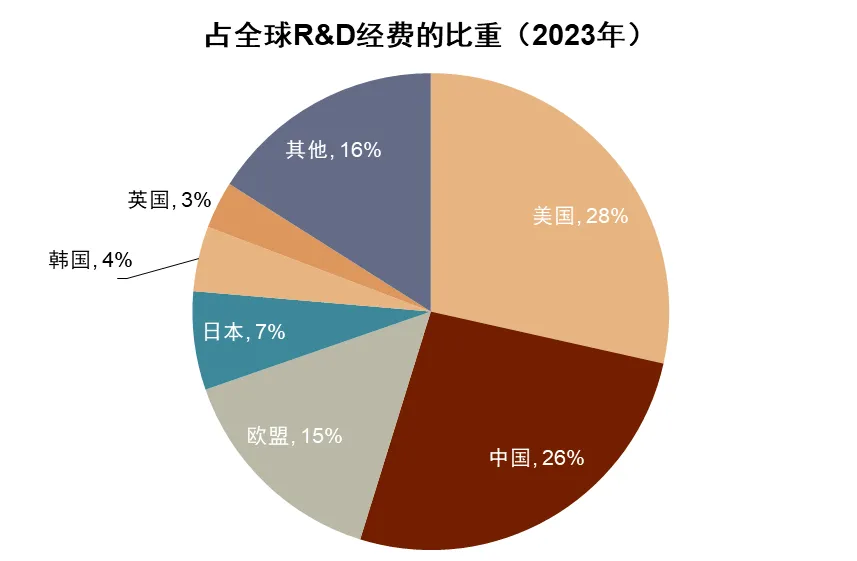

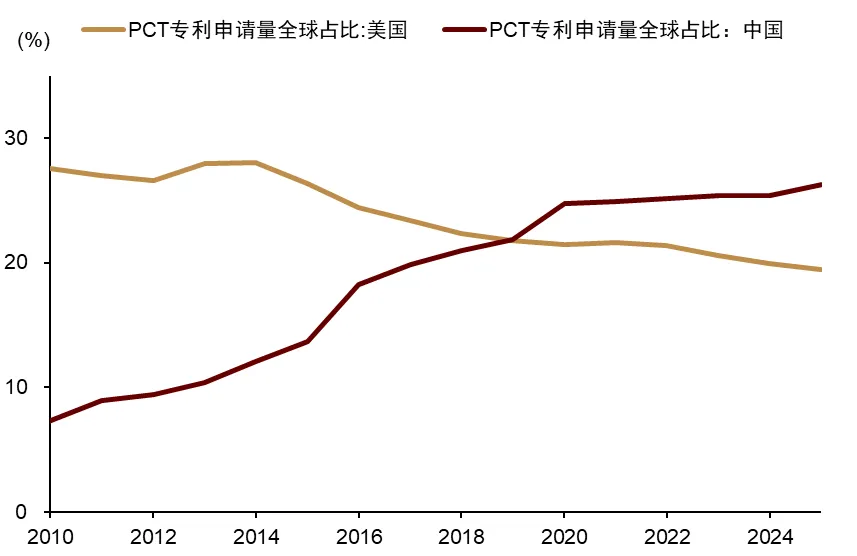

China's progress in science and technology innovation is also remarkable: from 2013 to 2025, China's ranking in the Global Innovation Index rose from 35th to 10th (Chart 11). China's total R&D expenditure is second only to the United States in the world, while its number of PCT patent applications has surpassed that of the United States (Chart 13, Chart 14).

Chart 13: China's R&D expenditure ranks second in the world, only after the United States.

Source: World Intellectual Property Organization, CICC Research Department

Chart 14: China's PCT patent applications have surpassed those of the United States.

Source: Wind, CICC Research Department

Lessons from China and the United States

For the United States, how can it simultaneously reduce its balance sheet, cut interest rates, expand fiscal policy, and prevent Treasury yields from rising? Drawing on China's experience, the US might need to take the following actions:

First, we need to optimize monetary policy operations and financial regulatory indicators, and make proper arrangements regarding liquidity.If the Federal Reserve really wants to reduce its balance sheet, it can increase reverse repurchase to support financial institutions to use Treasury bonds as collateral for financing and alleviate liquidity pressure; establish a liquidity tool specifically for TGA; adjust the regulatory requirements related to SLR (Governor Milan proposed that US Treasury bonds should be completely removed from the denominator of SLR[6]); and urge the Treasury to reduce the duration of US Treasury bond issuance, etc.

Second, to stabilize inflation expectations, there are two paths: the first is to tighten credit.The economy will naturally weaken, and the market has always been concerned about this, not so much because of policy arrangements, but because of assessments of the US economy. However, this may not be the situation the US government wants to see, nor is it the original intention of Warsh's approach. If this path is indeed taken, the private sector's preference for risky assets will decrease, Treasury yields will naturally decline, and Warsh's rate cuts may become more decisive and larger. Under this path, real interest rates will most likely still decline.

The second path is to improve total factor productivity.With the US maintaining loose monetary policy amid fiscal easing, will this translate more into inflation, trade deficits, and increased production capacity in other countries, or will it lead to improved supply capacity within the US? This question reveals the core concept of the Warsh approach, which essentially returns to market-driven endogenous money supply, favoring a "small government, big market" philosophy that believes the power of the free market will bring sustained technological progress and economic growth. If this approach succeeds, US total factor productivity will increase, supply capacity will improve, inflation expectations will stabilize, and the risk of rising nominal interest rates will decrease, although real interest rates may rise somewhat.

As we pointed out in our recent special report, “Not a Choice, But an Inevitability: US Policy from the Perspective of Political Economy,” the problems brought about by the free market are also significant, and are even the root cause of many of the current social problems in the United States. The appropriate policy direction for the United States should be post-Keynesian distribution reform, rather than simply returning to the free market.In other words, we believe that Warsh's ideas are inconsistent with the requirements of US economic reform, ultimately leading to a passive wait for technological progress to open up space for economic development. From China's experience, we can also see that truly transforming the path of economic and social development, bidding farewell to the past development model and building a new development pattern, requires the joint efforts of all parties.

From another perspective, we can understand China's monetary policy objectives as maintaining reasonably ample liquidity, promoting a reasonable recovery in prices, and sustaining economic growth. So, what can we learn from the US experience?

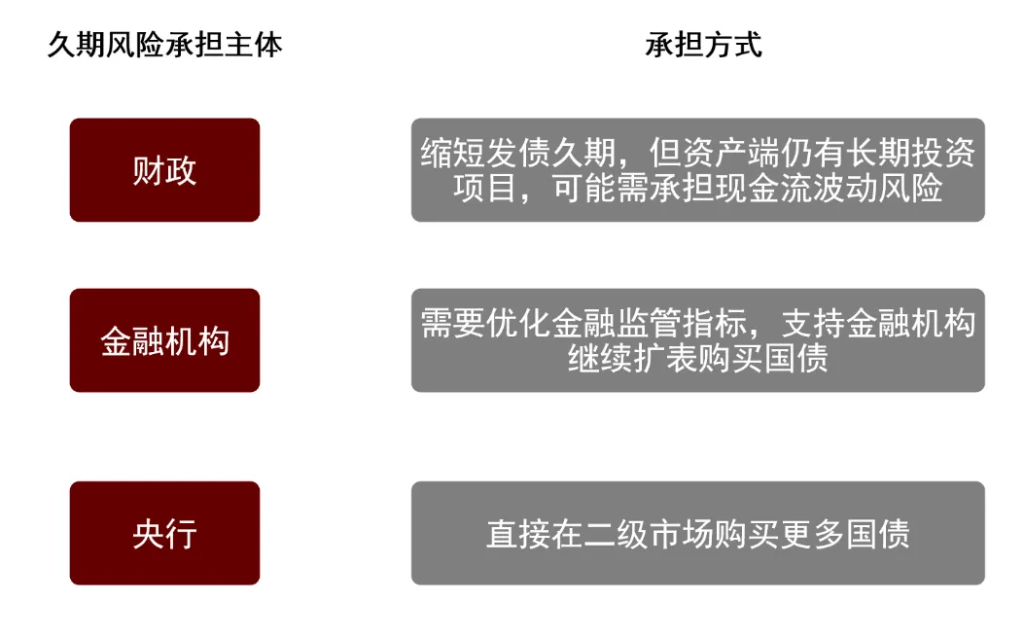

First, regulatory design and the central bank's balance sheet can assist in the transmission of monetary policy, while the design of the exit path is also very important.One of the problems China is currently facing is the banks' ability to absorb long-term government bonds. This problem stems from the duration mismatch and the corresponding interest rate risk regulation of the banking book. We have already discussed this extensively. Essentially, during an economic downturn, who should bear the duration risk of fiscal expansion? Should it be the Ministry of Finance, the central bank, or commercial banks?

There are several models for sharing duration risk: First, the government shortens its own bond issuance duration. In this process, the government still invests in many long-term investment projects and has to bear the risk of cash flow fluctuations itself. Second, financial regulatory indicators are adjusted so that commercial banks or other financial institutions can bear duration risk. Third, the central bank expands its balance sheet and directly assumes duration risk.

Looking at the US experience, during economic downturns, it both relaxed financial regulations (the Federal Reserve temporarily adjusted leverage ratios during the pandemic) and adopted a central bank balance sheet expansion strategy to absorb the duration risk of fiscal expansion. However, when it came to exiting the fiscal expansion, Warsh's mere announcement of "balance sheet reduction" caused significant market volatility. The lesson for China is that fiscal arrangements, regulatory arrangements, and central bank balance sheet operations can help smooth the transmission mechanism of monetary policy, while also considering exit costs and prioritizing arrangements with lower exit costs.

Second, exogenous monetary injections are very effective in expanding demand and inflation expectations, but supply-side reforms cannot be ignored.The Federal Reserve's quantitative easing, which involves purchasing long-term Treasury bonds in the secondary market, leads to exogenous monetary expansion. Exogenous money is not a result of the economic system's autonomous operation; rather, it is a driving force behind economic expansion. As the central bank purchases Treasury bonds, it injects base money, increasing private sector deposits. The money injected by the government is exogenous because no one would refuse government tax cuts or transfer payments; its quantity depends entirely on the intentions of fiscal policy. Therefore, exogenous money is a cause of economic changes and is highly effective in expanding demand and boosting inflation expectations.

Even so, the "Wash path" still receives market attention as an important option, primarily because of the question of whether demand growth driven by exogenous money can translate into improved economic efficiency. If demand growth ultimately relies mainly on imports, the accumulated trade and fiscal deficits will eventually raise concerns about the sustainability of economic growth.

Therefore, China may consider increasing the injection of exogenous money while simultaneously undertaking structural reforms. On the one hand, during periods of weak economic demand and pressure on nominal growth, it can moderately increase the injection of exogenous money, using liquidity tools, policy-based financial support, or fiscal coordination to improve the credit environment, stabilize inflation expectations and asset prices, and prevent a self-reinforcing downward trend in demand. On the other hand, it should simultaneously promote structural reforms by optimizing factor allocation, improving total factor productivity, deepening market-oriented reforms, and expanding high-level opening-up to enhance the supply elasticity and efficiency of the economic system.

Chart 15: How to Bear Duration Risk

Source: CICC Research Department

Third, both aggregate monetary policy and structural monetary policy are important for economic development.In terms of specific monetary policy operations, aggregate monetary policy and structural monetary policy are not substitutes for each other in the modern macroeconomic control system, but rather complement each other and have their own focus.

Aggregate monetary policy mainly adjusts the overall liquidity level of society through tools such as interest rates, reserve requirement ratios, and open market operations, affecting financing costs and the pace of credit expansion. Its role is to stabilize the economic cycle, manage inflation expectations, and maintain overall liquidity in the financial market.

Structural monetary policy, on the other hand, emphasizes targeted support, guiding funds to specific areas such as technological innovation, small and micro enterprises, green transformation, or strategic emerging industries through relending, rediscounting, policy tools, or special quotas. Its function is to optimize resource allocation and alleviate structural financing constraints; it is a tool for "precise adjustment." Therefore, in the stage of high-quality development, aggregate tools are responsible for stabilizing the macroeconomic environment, while structural tools are responsible for improving allocation efficiency. Only through their coordinated efforts can a balance be achieved between stabilizing growth, controlling risks, and promoting transformation.