作者:BitPush

One stroke is enough to rewrite the worldPaymentA deal that will reshape the industry landscape is quietly brewing.

On February 24, Bloomberg reported that a private payments giant led by the Collison brothers...StripeThey are considering acquiring the long-established payment pioneer.PayPalAll or part of the businessOn the day the news broke, PayPal's stock price surged nearly 7%.

One is a privately held unicorn valued at $159 billion, the other a former kingpin with a market capitalization of only $43 billion but a massive user network. Behind this deal lies not only the ebb and flow of market share, but also a discussion about the future of payments – especially crypto/StablecoinsThe deep game of payment.

PayPal's Dilemma and Underhanded Tactics

To understand why this potential deal has caused such a stir, let’s first look at two sets of figures.

Over the past 12 months, PayPal's stock price has fallen by nearly 46%, and its market capitalization has hovered around $40 billion. Meanwhile, Stripe, which is not yet publicly listed, has recently boosted its valuation to $159 billion through employee stock buybacks—less than a third of the former's valuation.

Behind this inversion lies the multi-dimensional pressure that PayPal's business is under.

The competitive landscape has been completely transformed. Apple Pay and Google Pay have secured their consumer (C-end) entry points by leveraging mobile operating systems, while emerging players like Adyen and Stripe are constantly encroaching on their territory with their technological flexibility in the business (B-end) sector. PayPal, which once started as a "third-party guarantor," is gradually losing its scarce connector status in today's increasingly diversified payment landscape.

User habits are also subtly evolving. With the explosion of social payments and embedded finance, people prefer to complete transactions instantly rather than being redirected to cumbersome third-party pages. Whether it's Stripe's one-click payment or Apple Pay's biometric authentication, both seem more convenient than that blue icon interface that requires remembering a password. While PayPal possesses the social trump card of Venmo, it has consistently struggled to transform it into a commercial engine.

The most fundamental pain point is the loss of market confidence in its growth potential. In the old world of fiat currency payments, PayPal's imagination has reached its limit; in its foray into crypto, although it launched the stablecoin PYUSD, it was criticized for "compliance in place but lacking intrinsic transaction demand," failing to penetrate the DeFi ecosystem or create unique value in its own B2B cross-border scenarios.

However, despite its fundamentals being heavily questioned, PayPal still holds several "chips" that are coveted by tech giants.

First, there's Braintree, which processes approximately $700 billion in payments annually, and Bernstein values it at $10 billion to $15 billion. Acquiring it would boost Stripe's total payment volume to $2.1 trillion, giving it a significant edge over competitors like Adyen.

Second is Venmo, a P2P application with over 100 million monthly active users and a valuation of approximately $5 billion. For Stripe, which has long remained "behind the scenes," this is a valuable consumer touchpoint: a kind of "last-mile visibility."

Thirdly, there's its nearly 30-year-old global network: a clearing infrastructure spanning over 200 countries, deeply embedded in cross-border trade, and 438 million active accounts with verified credit histories. While seemingly outdated, it serves as the most robust bridge to the global commercial frontier. PayPal recently launched the PayPal World program, partnering with Tenpay, UPI, and others, potentially reaching over 2 billion users. This interoperability connecting Eastern and Western payment systems is precisely the strategic entry ticket that no competitor can replicate.

Nearly thirty years of accumulation have not been in vain. It's just a pity that the person who best understands how to use this coupon may no longer be PayPal itself.

Stablecoins become the hidden main theme

However, one word repeatedly mentioned by Wall Street analysts reveals the deeper ambition behind this deal: stablecoins.

“The merger of Stripe and PayPal could make them significant players in the stablecoin space, as stablecoins are increasingly becoming a more crucial part of global commerce,” said Mizuho analyst Dan Dolev..

Looking back at the actions of the two companies over the past two years, it's easy to see that cryptocurrencies—especially stablecoins—have become their shared bet on the future. However, their strategic paths are drastically different.

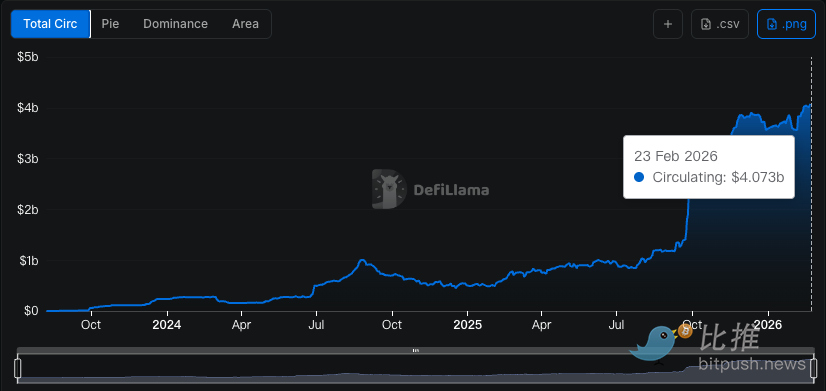

PayPal has chosen a "crypto-based network" approach, its underlying logic inheriting and continuing the centralized thinking of the SWIFT era. It aims to extend the advantages of its payment network to the on-chain world, thereby building a closed-loop ecosystem centered on PYUSD. In April of this year, it even launched the "PYUSD Holding Rewards Program," offering users a 3.7% annualized return, hoping to drive growth in cross-border payment business through stablecoin trading volume..

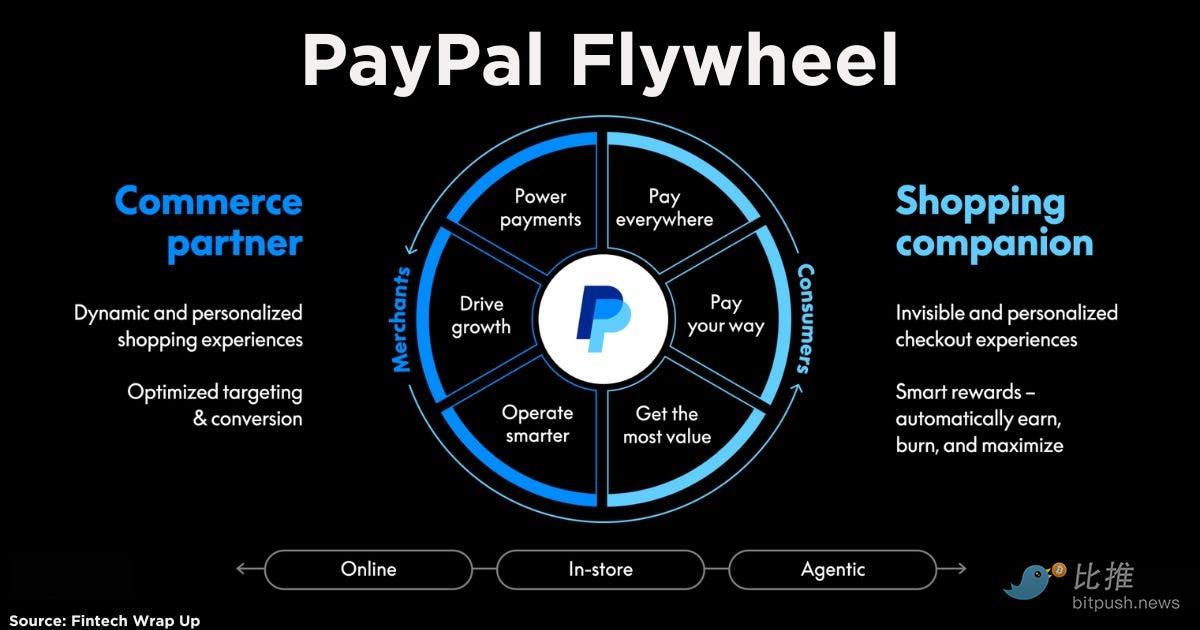

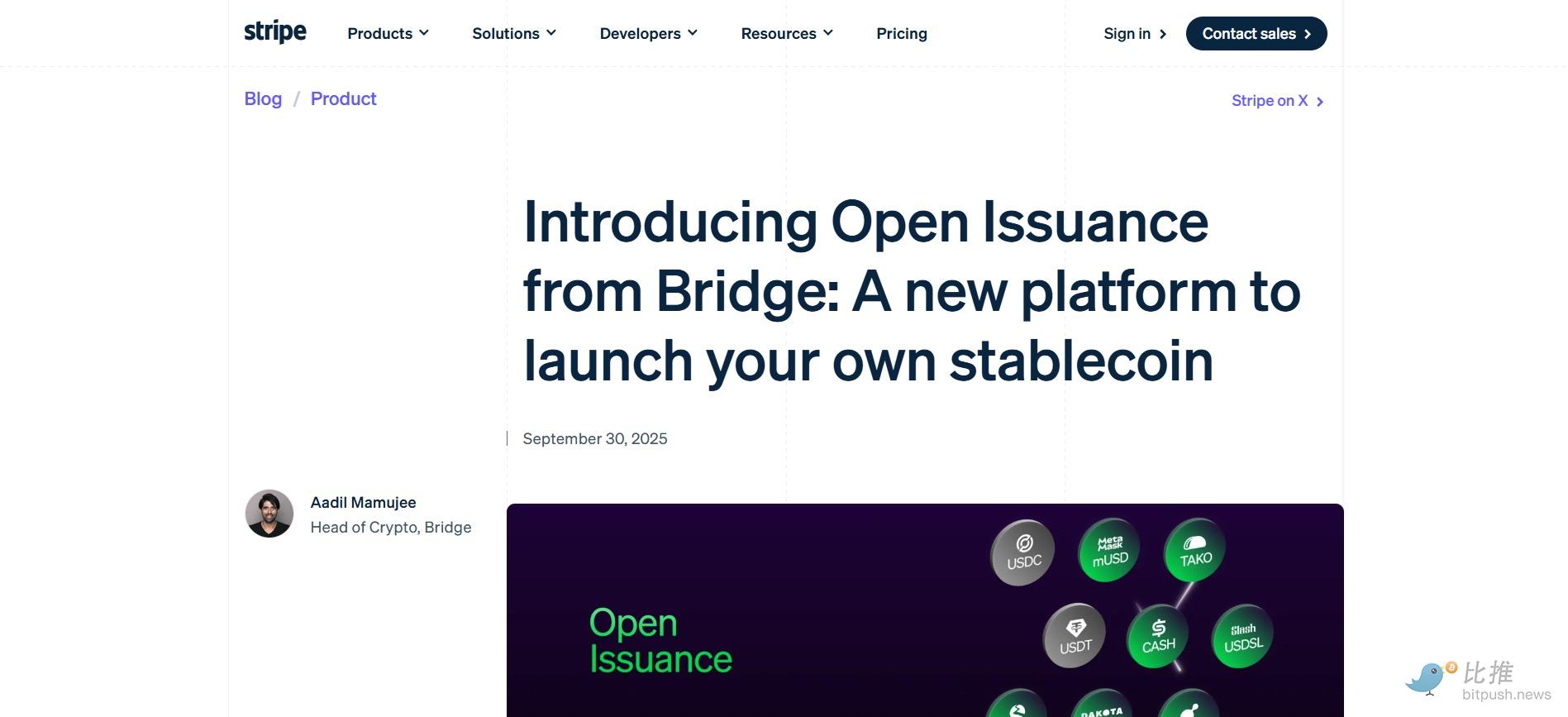

Stripe's strategy is more systematic. In 2024, it acquired stablecoin infrastructure company Bridge for $1.1 billion, its largest acquisition to date. But its true ambitions were only fully revealed with the launch of its "Open Issuance" platform—it doesn't bet everything on issuing its own stablecoin, but rather aims to become an "arsenal" for stablecoin payments, empowering other companies to issue, manage, and use stablecoins by building robust infrastructure and developer tools..

At the heart of "Open Issuance" is the ability for every enterprise to issue its own stablecoin through Stripe and earn reserve interest income. This "issuance-as-a-service" model cleverly shifts the focus of value capture: while other traditional stablecoin issuers are still calculating interest spreads of a few basis points, Stripe abandons its reliance on reserve interest and instead builds a new profit model based on service fees.It shifted the focus of value from "issuance" to "distribution".

The most crucial piece is Tempo. Stripe is partnering with Paradigm to build this Layer 1 public chain focused on payments, directly targeting traditional clearing networks like SWIFT. Overlaying these two strategic plans makes Stripe's logic for acquiring PayPal increasingly clear: Stripe possesses future-proof on-chain payment infrastructure (Tempo, Open Issuance), while PayPal has an existing user network (400 million accounts) and a market-proven stablecoin product (PYUSD).

If PYUSD is integrated into the Tempo chain, leveraging its sub-second confirmation and low-cost characteristics, and then reaching hundreds of millions of consumers through Venmo, a "Web3 payment closed loop" outside the traditional banking clearing system will become a reality for the first time. This is not only complementary at the product level, but also a disruptive force against the existing global financial infrastructure.

An even more imaginative scenario is AI Agent payments. Unlike the traditional banking system, AI Agents can have their own encrypted wallet address, through which they can receive, store, and send funds. This makes automated clearing between AIs extremely convenient and efficient, especially suitable for micro-payment scenarios with small amounts and transaction backgrounds.Stripe's x402 payment protocol, launched this year, paves the way for this future—allowing developers to conduct automated machine-to-machine settlements via the Basechain using USDC, expanding payment scenarios from "human-to-human" to "machine-to-machine." PayPal's 400 million accounts are precisely the ideal "cash-out outlet" for these AI agents.

Challenges of Regulation and Integration

Of course, the finalization of this deal still faces significant uncertainty. Sources familiar with the matter emphasized that discussions are still in their early stages, and whether an agreement will be reached is far from certain..

Private companies acquiring publicly traded companies and taking them private is not uncommon in business history. Elon Musk's acquisition of Twitter for $44 billion in 2022, followed by its swift delisting from Nasdaq, is a prime example in recent years. Acquirers typically use cash tender offers or mergers, paying a premium (potentially between 30% and 50%) to the target company's shareholders to buy out the shares and then delist the company, either as a subsidiary or through full integration. Stripe has ample cash reserves.With the backing of top-tier VCs like a16z and Thrive Capital, and financing channels including debt leverage, new rounds of private equity, or existing reserves, it could easily acquire PayPal..

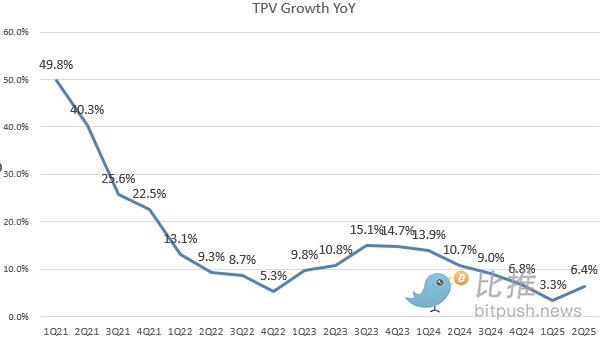

However, regulation hangs like a Damocles' sword. The merger of the two payment giants (with a combined TPV of nearly $3.7 trillion) is bound to attract the attention of antitrust authorities. Raymond James analysts believe that potential acquirers could include large tech companies such as Alphabet, Meta, Microsoft, Amazon, and Apple, but the limited financial information available about the privately held Stripe casts doubt on the feasibility of the deal..

Furthermore, the challenge of cultural integration should not be underestimated. Stripe is known for its geek culture and developer-friendly approach, and its co-founder...John CollisonThe company recently stated that it is "not in a hurry to go public."PayPal, on the other hand, is a publicly traded company with 400 million end-users. How to reconcile these two drastically different genes will be a challenge the Collison brothers must face.

Even so, the rumor itself is symbolic enough. It signifies a profound revaluation of the global payments industry: scale is no longer a moat, and future-oriented infrastructure capabilities are becoming the key factor in determining one's voice.

For Stripe, a successful acquisition of PayPal would be a cross-generational "David and Goliath" scenario; if it fails, at least the market has seen its ambition: it not only wants to become the payment foundation of the internet, but also wants to become the rule-maker of the next generation of the financial world.

Author: Coconut Shell

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG discussion group:https://t.me/BitPushCommunity

Bitpush TG Subscription:https://t.me/bitpush

Note: All articles on Bitpush represent the author's views only and do not constitute investment advice.

John CollisonPaypalStripePaymentStablecoins

Related News